In recent years I’ve spent a lot of time speaking to and consulting with builders and remodelers, big and small, and I’ve noted that there’s often confusion about what types of costs go where on a financial statement. On a typical P&L (profit and loss statement), the costs are segregated into two types: cost of goods sold (COGS) and overhead. COGS consists of the costs directly related to producing jobs. Accountants call these “above the line” costs. Overhead items, or indirect costs, go “below the line.” The “line” that differentiates these costs is the gross profit. To arrive at the gross profit, above-the-line job costs are subtracted from job income or selling price. To get net profit, overhead costs — below-the-line costs — are subtracted from the gross profit.

Direct vs. Indirect and Fixed vs. Variable Costs

Above-the-line costs are the “sticks and bricks” that go directly into your project (labor, materials, and subcontracts) and are always directly proportional to the amount of work you do. In other words, direct job costs vary depending on how much work you do — so we call them “variable direct costs.”

“Fixed costs,” on the other hand, are costs you can count on staying the same. The rent on your office building is fixed, as are your bookkeeper’s salary, your monthly Internet service fee, and pretty much any other costs that come in month after month. (Other utilities, like gas and electric bills, are fixed, because even though they may vary by month, they’re very similar year after year.) Your rent and your bookkeeper’s work are not things that get permanently installed on a job, and so they do not contribute directly to the value of any project; thus they are considered indirect costs and should show up below the line. We call these “fixed indirect costs.”

This is where it gets confusing. While all direct costs are variable (connected to project volume), not all indirect costs are fixed. There is another important category of overhead that is both indirect (below the line) and variable (it changes in response to volume in some way). The most common of these costs are known as “construction indirect” costs; they include items that are less obvious like dumpsters and trash hauling (the more projects you do, the more trash you generate), job trailers, vehicle expenses, and hand-tool replacement. Other below-the-line variable indirect costs recognized in the NAHB chart of accounts include such things as sales commissions, warranty expense, and construction financing costs.

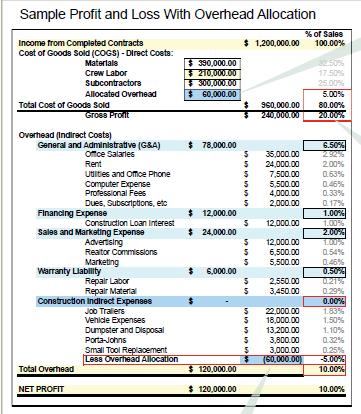

Reallocating Variable Overhead Costs

Most contractors include dumpsters, cellphones, and vehicle costs in overhead (below the line), and rightly so. For one thing, it makes sense for tax purposes. But another reason these expenses get lumped into overhead — even though they vary according to job size — is that it’s difficult to apply such costs to specific jobs. You can’t ask your bookkeeper to enter a cellphone bill and split it among all the individual jobs the employees worked on that month. Likewise, the bookkeeper would balk at creating an enormous spreadsheet to split out every fuel and vehicle maintenance bill across individual jobs, according to job size and duration. It would take forever and wouldn’t be worth the time.

And yet, to be accurate in estimating and markup, you need to know what percentage of these costs should apply to each job. Otherwise, you don’t know the true cost of the work you’re performing. So the question is, how can you make sure these costs get allocated to the proper jobs? And how can you know, when estimating, what percentage should apply to a given job?

I’ll suggest two approaches. With both methods, you continue to code these variable costs to overhead accounts, but you also charge them to specific jobs — in other words, move them above the line. But to keep your books balanced, you’ll create an additional negative, or contra, overhead account where you will record the reallocation of the variable costs as you post them above the line. So, for example, you would create a pool of all your vehicle costs, including maintenance, fees, insurance, fuel, and so forth. Separate these costs as you normally do in the overhead section of your P&L. Then, create another account, a contra account for these variable overhead expenses, where you post the reduction of overhead as you charge them to jobs (see sample P&L, previous page). You can do the same for cellphones and small tools — or any overhead expense item that fluctuates with volume.

The Labor Burden Method

One way to allocate these costs is to add a labor burden item through your payroll system that adds on a specific dollar amount or a specific percentage of every labor dollar. The same amount would be posted to the contra overhead account, which carries a negative balance — similar to a liability account used for payroll taxes. The net effect will be to increase job costs while reducing overhead.

So what number should you use? One strategy is to use last year’s numbers to come up with an educated guess. For example, say you spent $3,000 in small tools last year. You and two employees worked all year, clocking 2,000 hours in the field. Therefore, the figure you would add to your labor burden would be $3,000 · 3 · 2,000, or $0.50 per hour. This is how much it costs to cover the small tools that your field staff uses in a year.

If for some reason last year’s numbers are not an accurate representation of your costs, use the dartboard method: Just pick a number and start allocating it to your jobs. After a few months of using that figure, your P&L can help you determine if it’s too high or too low. If by midyear you’ve spent $2,000 on tools but only allocated $1,500, your allocation is too low. If, on the other hand, the numbers net to a negative amount, the allocation rate is too high. In a perfect world, the actual costs less the allocated costs should net to zero, but it’s not a perfect world. As you review your numbers, you can always adjust the rate. Analyze these numbers every few months, and make adjustments as needed.

Monthly Allocation

Another approach is to total your variable overhead costs monthly and create a single entry that allocates them to the jobs. You can charge them to specific jobs as a percent of revenue or a percent of total labor costs. While this approach is not as automated as the payroll entry, it can provide a more accurate allocation because it’s based on actual costs.

The ultimate goal with either method is to get a handle on how much it costs to actually run your jobs. Separating out variable overhead costs in this manner will give you a clearer picture of your fixed overhead, the true cost of staying in business regardless of the number of jobs you perform.

Note that allocating variable overhead costs to specific jobs does not change the net profit margin, and in fact actually lowers the gross margin. So, you might ask, why bother? To answer a question with a question: Don’t you want to know how much your jobs really cost? In years past, contractors got away with marking up jobs with enough padding to cover the extra stuff. But in this new era of tight margins, you’d better know your actual job costs and what it takes in fixed overhead just to keep your doors open. Then, when creating proposals, you’ll be certain of your numbers, and confident that the sales prices will cover all your costs and ensure a profit.

Leslie Shiner provides business advice to builders throughout the country. She is based in Mill Valley, Calif.