Over the years, I have observed my clients struggling with a number of obstacles to pricing their work right. First, let’s define “right.”

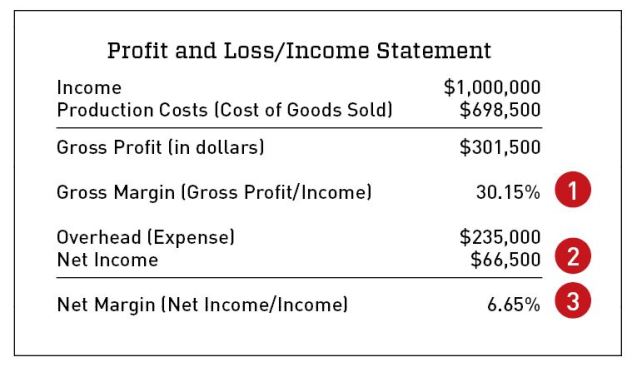

To me, pricing right means that you have determined and achieved targets for one or more of the measurable objectives shown on the sample Profit and Loss statement, below.

1. Achieved gross margin expressed as a percentage (of income) 2. Bottom line (net profit) dollar figure 3. Net-margin amount expressed as a percentage (of income)

The causes of failure typically fall into two distinct categories—not knowing how to use financial information to generate pricing strategy, and being reluctant to charge what is required. Let’s look at each one of these separately.

Financial Curveballs

It’s extremely easy to calculate what you need to charge if you have accurate financials that are organized correctly, and I have covered this topic in great detail in previous articles. However, there are some common curveballs that tend to invalidate or degrade the process. These include the following:

- Basing charge-out rates (on T&M work) on partially burdened labor (leading to loss of profit when invoices fail to cover the fully burdened cost of labor)

- Basing estimated labor costs (on fixed-price work) on partially burdened labor (leading to adding markup to partially burdened labor, which leads to loss of profit when invoices fail to cover the fully burdened cost of labor)

- Neglecting to add sales tax to materials costs when estimating (if not using a tax-exempt number). Consult your state’s regulations to find out what kind of costs on which category of jobs are subject to sales tax; your state will expect to receive sales tax revenues whether paid at time of purchase or charged to and collected from your customer.

- Failing to include workers’ comp costs on uninsured subs when estimating (fixed price) or charging out (T&M)

- Neglecting to charge for consumables (saw blades, bits, sanding disks, batteries, paint supplies, and the like) and the repair and replacement of small tools; these things will always be used on jobs but are rarely accounted for in estimates, or charged out on T&M jobs

- Not accounting for nonproduction (no nail banging) time required of lead carpenters, whose responsibilities include “administrative” or “management” duties such as ordering and checking in materials, supervising subs, writing up change orders, and dealing with customer questions and concerns; this is time that should be added in estimates of fixed-price work, and charged for in T&M jobs

Missing these costs or invoiceable charges can mean underestimating a fixed-price job or underinvoicing a T&M job.

As soon as your production costs are higher than allowed for, your gross profit (in dollars) and achieved gross margin (% of income) will be lowered.

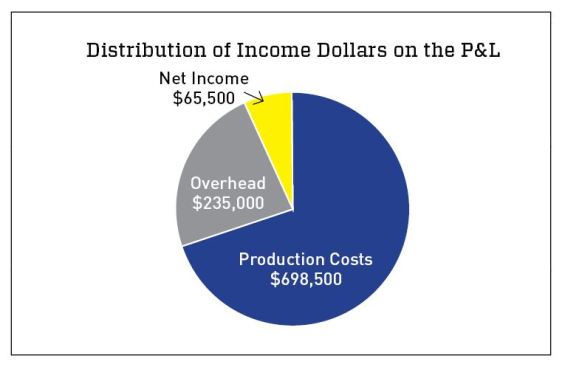

Bear in mind that the only dollars you can use to pay for overhead and contribute to profit are those left over after you’ve produced jobs. If your invoiced costs fail to adequately cover your production costs, your bottom line will suffer. That’s because every sales dollar will be distributed in only one of three ways (see pie chart based on our Profit and Loss statement, below).

If your production costs exceed what you expect, then what will “give” is net income. That slice will shrink and your profit target won’t be met. Similarly, if you have failed to account for overhead accurately, or have added a new expense (such as the salary for a full-time estimator) without planning sufficiently far in advance to allow time to increase markup, then your overhead will expand and your net income will shrink.

Another way of stating this is that production and overhead costs are “non-negotiable” (they are what they are), while net income is “negotiable.” In other words, the net income will be what takes the brunt of cost overruns.

Reluctance to Charge Enough

But perhaps a company is successfully creating estimates that are all-inclusive and that accurately define what that job will cost. Maybe that company has even done the required math and uses historic data to identify a markup that will lead to the right net profit. But even this company may fail to pull the trigger and actually charge enough. Why? This is where a business owner’s emotions kick in, and it’s not uncommon. I see two general problem areas—fear and what I call the “generous craftsman” effect.

Fear of Charging Too Much

Let’s take fear first. The knee-jerk reaction to any suggestion that prices need to be raised is, “I’m already one of the highest-priced companies around; if I raise my prices, I’ll never sell any work.”

The very fact that the contractor’s “go to” place is price suggests that jobs are being sold with an emphasis on price. If, during the sales process, your emphasis is on price rather than painting a picture for the prospect of how their experience with your company will be different from what they would experience elsewhere, then the prospect’s focus will be on price also. Shifting the focus means that you separate yourself from the “competition.” In fact, if you do it right, you will appear to have no competitors who deliver what you do.

When I ask other contractors why they believe customers choose them, I often hear two things:

- We do high-quality custom work

- We have a reputation for honesty

When I know for a fact that the company is undercharging (I know this when they became a client because they are unhappy with the amount of money they’re making in relation to the amount of effort they’re expending), and I ask them why they aren’t considering the possibility that maybe they’re getting work because they’re good and they’re inexpensive, the result is usually a stunned silence. My point is, if your reputation is that good, why not see what happens if you raise your prices? Aren’t you worth it? If you don’t know exactly why you’re different (and better), how can you communicate this to prospects and make them happily embrace a price that’s a bit higher but offers a world of difference? In my experience, contractors who are brave enough to test the waters of higher pricing usually see virtually zero drop-off in sales.

The “Generous Craftsman” Effect

One of several reasons that I have chosen contractors to be my market niche is that I find the vast majority to be the total opposite of those bad apples who have, sadly, given the industry a bad reputation. In general, I find that contractors:

- Are honest

- Are people-centered

- Take enormous pride in creating beautiful and lasting work

- Consider their work to be a form of legacy

- Do whatever it takes to “make it right” (including doing lots of additional work without creating change orders, because “it has to be done,” or “it will look better”)

- Bend over backwards to make their customers happy (often in the face of outrageous demands, I might add)

- View what they charge from the standpoint of their own personal budgets (“How can I charge that when I couldn’t afford to pay it?”)

- Judge the “value” of a job not by its profitability but by how beautifully it turned out; this tendency can be amended to include pride regarding the design, the use of new or “trendy” materials or methods, or the fact that the project won an award (even when doing so caused them to go over budget)

- Assume a paternalistic relationship with employees, subs, and suppliers, often to the extent that they will hold off paying themselves in order to take care of others

- Implement their personal value system through company policy (including pricing!)

- Emphasize being “fair” to their customers

- Undervalue what their company provides

Sadly, the very characteristics that make contractors incredible neighbors all too often lead to decades of hard work with little to show for it. Equally unfortunately, I am often called in only when things have gotten to a fairly desperate or discouraging point or when it’s time to pass the company on to the next generation. I have heard from more than one worn-out contractor that what was good enough for him or her to subsist on just wasn’t good enough to pass on to the kids. It is often only when their concern for their kids’ welfare (there’s that wonderful, generous spirit) overrides their concern for their customers’ welfare and their passion for being “fair” that they can even consider pricing realistically. And for those “living” their value system through the service they deliver, this can be traumatic.

Summary

Pricing right means understanding your production costs (all of them), having a handle on overhead (including any upticks in costs due to planned increases of staff, marketing, insurance, and so on), and being realistic about the profit you feel you deserve based on the effort you expend.

Once you have your target numbers, the next step is to actually implement a strategic pricing plan that will hit those targets. This may require you to take a fresh look at the most important things your company delivers. You will probably find that customers are far more impressed by your staying on budget, sticking to a timetable, communicating clearly and frequently, and holding your crew to dress, language, performance, and jobsite cleanliness standards than about how perfect those outside miter joints are on the crown.

When you have calculated what you need to charge and identified those characteristics of your company that you feel justify your pricing, the final step is to deal with reluctance, regret, and fear. One client said to me, “If I’d met you 10 years ago, I’d be rich by now!” He felt bad that he’d been underpricing and undervaluing work for years. That was then, this is now. Focus on embracing new ways of thinking about your company and the manner in which you express your value system through your company, and reconcile to the fact that you may need to start favoring the good of the company (including you, your family, your employees, and their families) over the good of the customer.