The events of 2020 were a shake-up of business as we know it. The hit was uneven among construction contractors, with some firms seeing a large reduction in business and other firms experiencing a significant increase. Regardless of their market, though, all of the contractors I was in touch with over the past year had to work hard to adjust to changes in workflow, safety procedures, ways of meeting with clients, and most important of all, how they managed their cash flow and debt, priced their jobs, and monitored their financials. Resoundingly, all had to go back to the basics of business and take a hard, analytical look at what success would mean for their companies in the near- and long-term. This article is a summation of the lessons learned.

What approaches have contributed to your company’s survival and even success? The businesses I know of that have been successful have taken the following key actions:

- Demonstrated decisive leadership.

- Made decisions based on hard data, not guesses or wishes.

- Generated systems for oversight and compliance.

- Monitored and adjusted according to current data, including targets and trends.

Demonstrate Decisive Leadership

Leaders constantly observe current conditions, compare with the past, and take decisive action to establish future improvement. They prioritize the health of the company over the comfort of individual employees and make hard and often unpopular decisions, knowing that the short-term discomfort will likely lead to a more stable and secure future. Examples of decisive leadership include the following:

- Delegate, don’t abdicate. Too often, critical decisions such as setting up the financials, and even the categories for job costing, are left up to an accountant or a bookkeeper. Because neither typically has a background in construction, this rarely creates good results. The boss needs to take responsibility for making decisions on how the company will operate, and this includes structuring ahead of time to populate predetermined reports.

- Monitor sales-dollars-per-employee ratios and reduce the workforce when it cannot be supported intact by current or projected sales volume.

- Change suppliers or request deeper discounts on materials, negotiate more timely deliveries, or arrange for online receipts to eliminate the physical exchange of paperwork.

- Survey subcontractor performance to pare down to the most productive, reliable, and professional subs. Stop hiring those who send you insufficiently detailed or late bills or who have to be chased down; your office staff has better things to do with their time.

- Review marketing strategies. This might include cutting back in some areas, altering the message of what your company is about, or even expanding into new territory. This also means surveying your existing clientele to find out what kinds of safety precautions would need to be in place before they would commit to new projects. Then use this information to slant your marketing message to new prospects, who doubtless have similar concerns.

- Review production methods to look for ways to increase safety. Many contractors learned how to modify practices when dealing with lead paint; similar revisions may make you more desirable to prospects in addition to reassuring your own workforce.

- Review processes to look for ways to increase efficiency. This might include exploring technology that would permit existing workers to work remotely.

- Review customer-centric practices to see what can be improved or eliminated. For example, some contractors (particularly those doing cost plus or T&M) spend time copying and collecting bills to provide to customers as proof of costs, even when customers have not requested this service. If you have a “difficult” customer who insists on micromanaging job costs, then you can provide this detail, but if they don’t ask for it, don’t offer it. Also review your post-job contacts with customers. Are you staying in their field of vision by sending birthday cards, project “anniversary” cards or e-mails including before and after pictures of their projects, inviting feedback through surveys, or offering a “reward” for consummated referrals?

- Demonstrate consistency. There’s nothing more frustrating to employees than having a boss come out with one “great new idea” after another. When the boss reads a book, attends a seminar, or talks with a peer, they may get all excited and want to switch to that method—right now! All too often, the impact on the company of additional work or the need to implement new technologies is ignored, and the workforce gradually becomes cynical about and resistant to new approaches. Effective leaders introduce change only after thoroughly understanding the implications to those “in the trenches,” inviting contribution from those who will be impacted, weighing the cost-benefit, and setting up a specific step-by-step plan for conversion. When new practices are discovered and implemented, don’t jump ship the next time something cool comes along.

Follow your own rules. We all know that kids learn by observing, and that the strongest influence is from parents. Without insulting your workforce, understand that, like kids, they will watch and match what you do. If you deny wage increases or profit sharing due to low profits and then buy a fancy new truck for yourself, the message is mixed and you will lose credibility. If you emphasize the importance of good customer relations and then are heard being rude to a customer, the message is mixed. If you stress teamwork, professionalism, and mutual respect and then publicly chastise a worker, the message is mixed.

Make Data-Driven Decisions

Many contractors rely on their accountant to tell them (at the end of the year) how things went. When used in this way—as historians rather than as collaborative teammates—accountants may get your taxes filed, but they lack the contractor-specific training and knowledge to help you improve.

Instead, either you need to find a construction-savvy accountant or financial analyst to help you understand your numbers, or you need to get training yourself so that you won’t be held captive by somebody else’s availability.

First and foremost, you must have your books set up to provide numbers you can understand at a glance and then act on. This usually means setting up your books in a way far different from what an accountant without construction experience is used to. In fact, on many occasions, contractors who have been diligent about setting up and monitoring their books have gotten an unwelcome surprise after submitting them to their accountant and then finding that the accountant restructured things to make it easier to file taxes. In these cases, there are three solutions: Educate the accountant on the purpose behind the original setup, instruct the accountant not to make any changes to your accounting file but rather to file taxes based on whatever adjustments need to be made outside the software, or change accountants.

These are things you need to monitor:

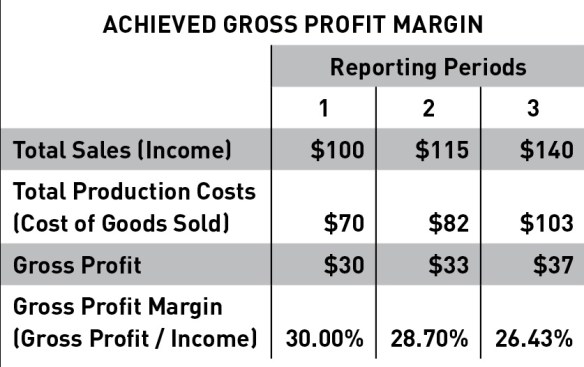

Achieved gross profit margin (the percentage of sales dollars due to profit). In the chart at the top of the next page, sales are increasing, but what is happening to profitability? Gross profit margin is probably the most important metric to track. Be aware, however, that if you are including “deposit payments” (“good faith” or “schedule place holder” money collected from customers prior to work starting and costs being incurred) in income, your gross profit figures and gross margin percentages may be skewed.

Total sales (total dollars coming in as the direct result of selling work). This figure should not include money from interest on savings accounts or money markets, money from selling that old truck on Craigslist, or money you won in a lawsuit. While profit is more important than sales volume (it’s not about what you bring in; it’s about what you get to keep), it’s critical to keep an eye on sales volume because your pricing must be based on projections. If your projections are higher than reality, you may run out of cash.

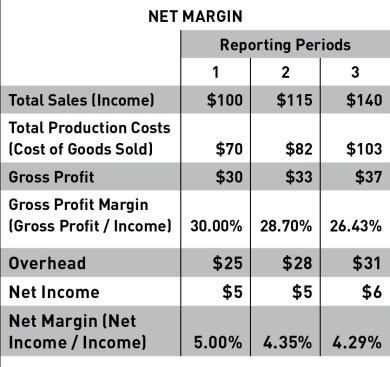

Net income (dollars left over after you have paid all your project costs and also paid for overhead). It’s easy to look only at sales dollars, see the growth, and assume that you can afford to increase your overhead, such as by adding a part-time office worker or doubling your marketing. If you do so, the effect of lowered gross profit and increased overhead will produce a double whammy.

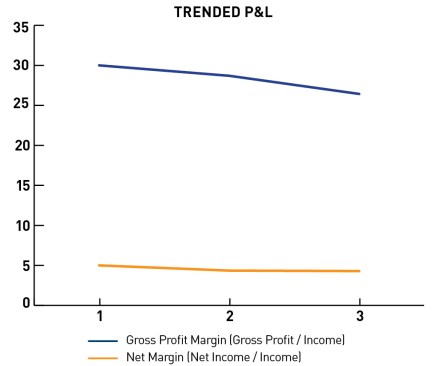

Trended reports should show you the direction in which the company is headed. Are things getting better or worse? When practical, graph the data showing multiple periods for easy visualization. If there is a change over time, is it consistent or are there peaks and valleys? Can these be explained? Can a downward trend be reversed? If so, how? And how long will it take? For example, if the issue is selling jobs at too low a price, and you’ve just sold projects that extend out the next 14 months, are you doomed to see the profit lines continue to drop, or can you take action now to reverse the trend?

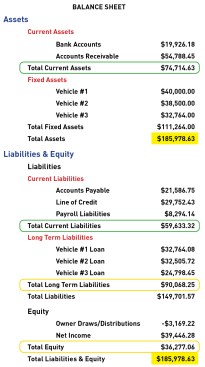

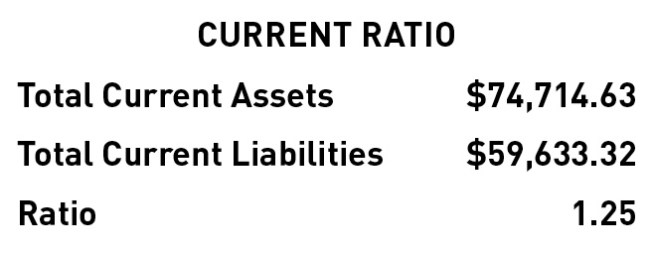

Balance sheet. Use a balance sheet in addition to a P&L statement. Everybody “gets” the P&L, but it is the balance sheet (see example below) that can give you a better overall picture of your business health. A P&L shows only a period of time (such as January 1–December 31, 2020) while a balance sheet is a point in time (such as every moment of your business’s existence through December 31, 2020). This report shows debt and can give you a heads up regarding cash flow as well as the degree to which your company is being sustained by borrowing.

Current ratio is based on two figures: total current assets and total current liabilities. These are outlined in green on our sample balance sheet. “Current” refers to something that occurs within 12 months. So current assets are cash or can be converted to cash within 12 months. Since you will be receiving payments from customers within 12 months of the invoice date, accounts receivable are considered current assets. Current liabilities are those payable within 12 months. These usually include accounts payable, payroll liabilities, and short-term loans such as lines of credit. You want to have $1.25 or more of current assets to pay for $1.00 of current liabilities. Therefore, the current ratio (current assets divided by current liabilities) should be 1.25 or higher. A ratio lower than that signals an imminent cash-flow crunch. In our example below, the current ratio is 1.25, signaling healthy cash flow.

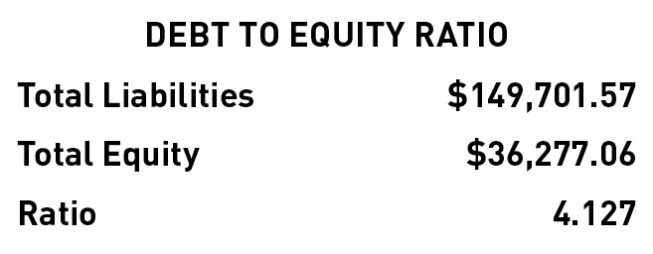

Debt to equity ratio is based on two figures: total liabilities and total equity. These are outlined in yellow on our balance sheet. Your total equity is roughly equivalent to the value of your company; if your liabilities are larger than your equity, then in the event of liquidation of your company, you would still owe money. Therefore, the ratio of liabilities to equity should be less than 1 (in other words, you should have a higher amount of equity than you do liabilities). In our balance sheet example at right, the company is essentially operating on debt. Why? Should it have held off buying those trucks or gotten cheaper ones? Accounts payable looks reasonable, but the company has less than $20,000 in the bank with a line of credit of nearly $30,000.

While the current ratio of 1.25 looks acceptable, further analysis suggests that this is due in part to having a generous amount of cash. However, the cash was added by drawing on the line of credit. Based on the debt to equity ratio the company is in trouble.

Price Jobs Correctly

It seems obvious that if you sell at too low a price, you will not make the profit you need and deserve, and eventually your company will fail. Yet too often contractors confuse optimism with planning and hope with reality. You can’t figure out what you need to charge unless you understand—and really believe—what it costs you to be in business. Yet too many contractors pick a price based on some arbitrary figure (possibly what their non-construction-savvy accountant suggests, or what markup they “hear” a competitor is using, or what their prospective customer can tolerate, or what seems “fair”), cross their fingers, and that’s what goes on the contract. This can be reflected in a fixed-price contract or in the details of the cost-plus / T&M contract. Then they simply go with that and fail to look at the results. Every job must be examined to determine whether or not the targets were met.

As always, what you need to charge depends on your company’s costs. For example, if you offer employees generous health and retirement benefits and you profit share, your costs will be different from a company with similar volume that uses only subcontractors. This is why you can’t simply copy what a company across town is doing and expect to get similar results as defined by profit.

I have written numerous columns on how to calculate what you need to charge, but in simple terms, you need to identify your overhead, your desired amount of profit, and your projected sales volume. After that, it’s just math.

If you find that, overall, you are experiencing slippage (the discrepancy between what you expected to make as gross profit vs. what you actually make) on virtually every job, then you can spend a lot of analysis time trying to figure out where the overages are, or you can simply allow for slippage by marking up more to allow for it. However, bear in mind that it can be extremely useful to identify specific tasks that your crew consistently goes over budget on.

Know Your Target Prospect Pool

Effective contractors know exactly who their target prospects are. This is because they not only analyze the profitability of individual jobs but also group their jobs by category. Categories may differ among companies, but there should be some established criteria by which successful jobs can be identified and replicated. Unless you discover that bathroom jobs with moderate levels of finish that are located more than 30 minutes from the office continually fall short of meeting their target margin, you will continue to sell that kind of job.

Establish some buckets into which jobs can be dropped and use that information when tweaking marketing, pricing work, or even deciding to turn down work.

Estimate Accurately

Unless you habitually practice “drive-by estimating” or have a crystal ball, you will need to estimate accurately. The topic is far too complex to delve into here, and there are gazillions of articles, webinars, and software designed for estimating. Larger construction suites allow you to take photos, drop them into CAD software, get takeoffs, and write up both proposals and materials orders all in one place. But here’s what you need to remember:

Labor is the hardest component to estimate. The total cost of labor (or burdened labor) is typically far greater than what first meets the eye. For example, if you pay a field worker $20/hour, you may calculate that he actually costs you $39.85/hour (in a company with generous benefits, it is not at all unusual to find that the burdened hourly cost is much higher than an employee’s hourly rate). So when you’re considering how much the labor will cost in a particular project, be sure you are estimating using the burdened cost. Leaving out some of the cost of labor will mean you will underestimate the total labor cost, leading to your underpricing the job. (For more on burdened labor, see “The True Cost of Labor,” Mar/08.)

Report Job Costs

You can’t improve what you can’t measure. So if the production team is consistently over budget on interior trim, for example, and you don’t notice it, you can only expect that the trend will continue. What’s more, the larger the percentage of interior trim on a job, the bigger loss of profit you can expect. It’s not enough to simply know that Job X brought in $45,000 and total costs were $35,000 (gross profit = $10,000; achieved gross margin = 22.2%); if your target margin was 30%, then somewhere, things went over budget. But where? Are projects taking more time than anticipated? Is there a higher percentage of waste than expected or reasonable? What’s going on?

You need to job-cost in such a way as to be able to identify the good, the bad, and the ugly components of production. How you set it up is up to you. I like job-costing by task (Framing Labor, Framing Materials, Framing Subs; Exterior Trim Labor, Exterior Trim Materials, Exterior Trim Subs; and so on), but it can be as simple (to start with) as breaking out total labor from total materials from total subcontractors. You can get more complex and detailed as your analytical skills grow and your production workforce is trained to provide the level of detail you seek.

Bear in mind that the greater the level of detail you seek in your reporting, the greater degree of complexity and need for training and oversight. You can’t suddenly spring 35 labor task categories on a production team that previously only reported total hours per job and expect to get accurate results. You will need to display leadership by thinking through it ahead of time to come up with an appropriately useful list of tasks that fulfill the “sweet spot” of sufficient detail to permit you to analyze jobs without swamping your production and office workforce. Then you’ll need to provide adequate training and create a plan for the transition, especially when new methods cross ongoing jobs.

You need to think through every task and be able to shoehorn it into your task list. Some things are obvious but others are not. For example, about half of my clients classify skylights with windows since they order windows and skylights together; the other half classify skylights with roofing since it will be the roofing subcontractor who installs them. Either way is justifiable and logical, but your employees need to know where to put skylights when coding time or costs.

Another example is gutters. They’re attached to fascia, which is associated with roof framing so does it get put with framing or roofing? But they’re part of exterior trim, so maybe that’s a better place. Or since gutters are designed to direct water away from the house, do they belong with drainage? Maybe gutter installation is such a significant part of your services that it becomes a separate task group.

Arguments can be made for any answer, but what matters most is that these questions are settled before the system is put in place and that sufficient time for training is built into the schedule. If you think it’s a waste of time to spend two hours training everybody on coding time and costs, compare that with spending time recognizing and recoding entries, as well as retraining to correct old habits.

Finally, be sure that if you are estimating burdened labor, you are also job-costing burdened labor. Keep your analysis “apples to apples.” Anything other than that will lead you to underreport the actual cost of labor, which will again lead to bad pricing and overly optimistic profit reporting on specific jobs.

Create Employee Standards

Effective business leaders provide workers with publicized standards (everything from dress code to construction methods) and targets (expected completion times, for example) and then hold workers accountable for meeting them. Objectives are communicated clearly and consistently, and excellent performance rewarded in some tangible way, whether by recognition (lunch with the boss, an achievement certificate or plaque, or the like) or monetary reward. Those who are noncompliant or fail to meet published standards are dealt with via a process outlined in the employee manual. An exceptional leader holds him/herself to these same standards and acknowledges his/her own mistakes.

Monitor Targets and Trends

Effective business leaders keep their eyes on the prize. They monitor results and look for ways to improve specific metrics. They recognize that past performance is no guarantee of future results. They not only examine results and analyze the reasons behind changes but also create and implement plans for improvement, often with the input of relevant employees.

Bottom line. The essentials of good business haven’t changed with the global crisis. What has changed is that the behaviors and systems employed by successful companies now, more than ever, need to be adopted by all businesses hoping to survive and even thrive.