It’s that time of the year when all the little oopses – all those financial issues that accumulated over the past year(s) because you were too busy to deal with them – come home to roost.

A Balance Sheet is divided into three main parts.

Although most contractors live and die by their P&L statement, the place to start identifying areas for correction is actually the balance sheet. If your balance sheet is wrong, 99% of the time your P&L will be wrong too.

Conducting a Balance Sheet Audit

This may sound intimidating, and something best reserved for the special knowledge and experience of an accountant, but it’s actually something that anybody can do, at least to a certain extent.

The first thing you need to know is whether you file your taxes on a cash or accrual basis. If you file on an accrual basis, that invoice you generated last February for $15,000 that the customer never paid will be included as income unless you take appropriate steps to eliminate it. If you file on a cash basis, that same invoice will not be included since only paid invoices will be included as income. (NOTE: The same holds true for bills: if you entered a bill for $5,000 back in August and still haven’t paid it by the end of the year, on an accrual basis P&L it will show up; on a cash basis P&L it won’t.) This is important in terms of understanding how to clear up some old transactions. The last thing you want to do is to look like you’re evading taxes!

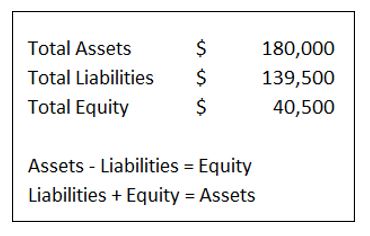

What should you look for? Your balance sheet is divided into three main parts:

- Assets (stuff you “own”)

- Liabilities (stuff you “owe”)

- Equity (the difference between them)

Assets are further divided into

- Current Assets – those that will most likely increase your cash within 12 months (bank accounts, Accounts Receivable, and inventory if you carry any) and

- Fixed Assets – depreciable things like large equipment and vehicles

Liabilities are further divided into

- Current Liabilities – those that will most likely decrease your cash within 12 months (accounts payable, payroll taxes, credit cards, sales tax, and lines of credit)

- Long Term Liabilities – debt that must be paid back over a period longer than 12 months (vehicle and equipment loans)

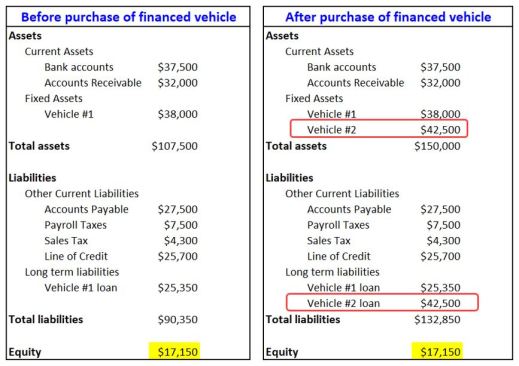

Long term liabilities are often associated with fixed assets. For example, if you buy a new vehicle for $42,500 and finance 100% of the purchase price, you would end up with a fixed asset of $42,500 and long term liabilities of $42,500. At that moment in time, the purchase has not induced any changes to equity because the asset and liability offset each other.

For Current Assets

1. Confirm your bank balances are accurate as of the end date of your tax year. This requires that you not only reconcile to each month’s statement, but also clean up any uncleared transactions from prior periods. For example, if you accidentally duplicated a Worker’s Comp payment check of $7,500, your cash balance will appear to be $7,500 lower than it really is. Look for uncleared transactions that reflect duplicate payments, lost checks, or similar. Clean them up before you submit your paperwork for tax preparation since cleaning up such lingering entries after the year is closed requires more effort.

2. For Accounts Receivable, review all unpaid invoices. Are these accurate? If you’re still clinging to that unpaid invoice from 2019, do you really expect to collect? If not, you need to write it off to Bad Debt or generate a credit memo that will take care of it. Again, the longer you wait to clean up unpaid invoices, the more difficult and time-consuming the process will be.

3. If you hold Inventory, perform a physical inventory and adjust quantities and values as required.

For Fixed Assets

If your accountant is on top of things, s/he will send you a list of questions or tasks around the end of the year. One question might be whether or not you have incurred any large expenses such as improvements to the office space you rent or the business owns, the purchase of any vehicles or equipment, or anything else that will be subject to depreciation. Any such purchases will be entered into the accountant’s Depreciation Schedule so that each year, the appropriate amount of depreciation can be recorded. This is important since the value of such investments diminishes over time. We all know that as soon as you drive that shiny new truck off the lot, its value begins to drop. The only good news is that this reduction in value can be taken as a depreciation expense over its lifetime. If you don’t record this depreciation as an expense on your P&L, you will end up paying more than you should in taxes. Also, if you don’t record depreciation on the item, its value will never appear to change, and your fixed asset balance will be wrong on the balance sheet.

Accumulated depreciation is properly classified as a fixed asset type of account, and it is normal to see a negative balance in it. This should be one of only two negative amounts on the balance sheet.

I often find that vehicles have been sold or traded still remain on clients’ balance sheets. This is incorrect and gives a false picture of the company’s overall value. Review the fixed assets and confirm that they are still property of the company. If not, confer with your accountant regarding the proper way to remove them.

(Note: If your accountant doesn’t prompt you to report significant business events such as these, or provide adjusting entries at year-end to record depreciation, kick up a fuss. If you don’t get satisfaction, change accountants!)

For Current Liabilities

1. Review your accounts payable. Look for overdue balances, missed payments, duplicate payments, or uncollected credits that may show up as negative balances. Investigate any prior year transactions that continue to linger.

2. Reconcile your credit cards to be sure you haven’t either missed charges or need to clean up any duplicates or other errors. If you have missed charges, these legitimate business costs won’t be included on your P&L and your taxable bottom line will be inflated.

3. Review payroll taxes and confirm that balances are accurate.

4. Review sales tax (if relevant) and be sure that the sum of your annual payments matches the taxable sales multiplied by your state’s tax rate. Adjust if there are errors. Be aware that sales tax is not considered income, so don’t expect your sales reports to match the income shown on your P&L. For example, if you charge $10,000 for a retail sale of cabinets and your state charges 5% sales tax, the invoice amount will be ($10,000 x 1.05) $10,500. So, the sales figure will be $10,500 but the income figure will be $10,000. Also review whether you are paying sales tax on a cash or accrual basis. If you pay on an accrual basis, then if you generate that $10,500 invoice on August 30 and you pay sales tax monthly, you will be subject to pay the $500 in sales tax in September. If you pay on a cash basis, then if the customer doesn’t pay you until mid-September, you don’t have to pay the $500 until October.

5. Reconcile your line of credit. Unlike a loan, a line of credit provides a potential sum of money against which you can draw. For example, if you get a $25,000 five-year loan, you get $25,000 right away and that’s the balance that will show on your Balance Sheet as a long term liability. You will pay it off, typically via a monthly payment plan established when you take out the loan. But if you get a $25,000 line of credit, you may only draw $5,000 on it now, then pay back half, then drawn another $10,000 in two months and so forth. The payoff balance fluctuates and is often unpredictable. Therefore, lines of credit are properly classified as other current liabilities. Once again, any interest payments made on the line of credit account should be captured and recorded as interest expense to reduce your taxable bottom line.

For Long Term Liabilities

Research the year-end balance on each of your loans. You may be able to access this information online or you may need to contact the lender directly. Either way, you want to be sure that this balance is correct. Often it is challenging to split out the principal and interest on your monthly payments. This leads many people to simply enter the total amount of the monthly payment. Unfortunately, this leads to the balance on the loan being inaccurate. If the loan balance was $25,000 at the start of the year and you made a $500 payment each month, then your records may show that the current balance is ($25,000 – $500 x 12 months) $19,000 when in fact a substantial portion of the $500 monthly payment might have gone to interest. There are two results of this kind of error. First, your loan balance will be incorrect. Second, you will be missing the interest which is an expense and therefore reduces your taxable bottom line.

For Equity

From a mathematical standpoint, Equity represents the difference between assets and liabilities. Equity is typically comprised of three main accounts:

- Net Income (from the P&L)

- Draws or Distributions

- Retained Earnings (this is a calculated value that may be entered automatically by your accounting software and will fluctuate throughout the year as the balances of assets, liabilities, and Net Income fluctuate)

Draws and distributions represent monies taken out of the company by the owner or officer. The terms are similar, but

- Draws refer to monies that serve as sole compensation. Owners or partners of a sole proprietorship, partnership or an LLC report their business’s earnings on a 1040 tax form; they are not compensated via payroll (in which deductions are made from wages, and these wages are reported via a W-2). Instead of wages, monies are simply paid out. Unlike wages, these do not reduce the taxable bottom line since they are recorded on the Balance Sheet, not the P&L. You will still end up paying taxes on these dollars, however. Remember that draws are not reported on the P&L; therefore, they do not reduce your taxable bottom line. Since your personal income taxes will be based in part on your bottom line, you will pay income tax on your draws, if only indirectly.

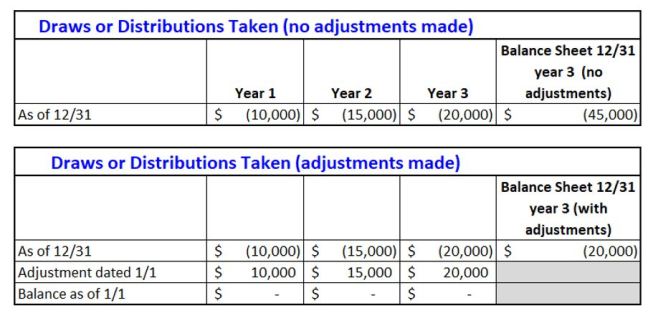

- Distributions refer to monies paid out to officers of corporations in addition to wages. Like draws, they are recorded on the balance sheet and do not reduce the taxable bottom line on your P&L. Distributions are used by officers of corporations, or LLC owners that file taxes using a 1120S form rather than a 1040. There are rules of thumb governing the ratio of distributions vs. wages. Obviously, the IRS isn’t going to condone a corporate officer paying herself $10,000 in wages and $190,000 in distributions! All too often, I find that draws and distributions are permitted to accumulate over many years. That is, if the owner withdrew $10,000 during year 1 of operations, and $15,000 during year 2 of operations, and $20,000 during year 3 of operations, the accumulated value ($45,000) may appear on the balance sheet at the end of year 3. This is misleading as it can look like that amount was withdrawn in a single year. Instead, astute accountants will zero out the draws or distributions on the first day of the following year, in order to show on the balance sheet only the draws or distributions that have been taken in that year. The offsetting account on these adjustments will be typically the equity type account.

- Retained Earnings, which is another equity type account.

Note: There are rules governing the amount that can be offset to Retained Earnings. This adjustment should be made with the assistance and endorsement of your accountant.

Year-end cleanup should be part of your procedure. Leaving “stuff” that accumulates produces a number of negative results:

- Your past year’s (or years’) numbers, if any, remain incorrect

- Transactions from closed years can be difficult to resolve

- Bad numbers from past years typically are brought forward into the current year, so it’s likely that reports for the current year will be skewed

- Reports should be easy to interpret, without constantly having to remind yourself that a particular number is skewed (I often hear comments such as “Oh, I know that customer actually did pay; their balance is wrong; I just sort of ignore it when I’m looking at accounts receivable reports” or “No, we don’t really owe that. I think maybe we double-entered something.”)

Why not start each year “clean” and be confident about the accuracy of your data?