Big-ticket remodeling activity nationwide will rise at double-digit levels through much of 2014 before starting to slow next winter, according to the latest forecast from Harvard University’s Joint Center for Housing Studies (JCHS) released today.

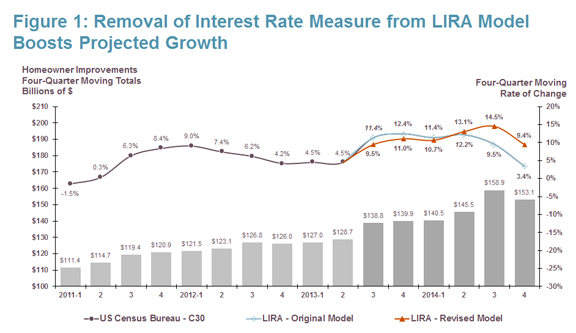

The center’s Leading Indicator of Remodeling Activity (LIRA) predicts that spending on home improvements will reach $153.1 billion this year, a 9.4% rise from spending in 2013. That’s a slower pace than the four-quarter moving growth rates of 10.7%, 13.1%, and 14.5% indicated in JCHS’ last three quarterly reports.

“Sluggishness in the housing market and specifically in home sales may result in a deceleration of home improvement spending,” a JCHS announcement said. The Center’s estimate of spending takes in all improvements of $500 or over that involve homeowners. Improvements costing less than $500, as well as all spending on rental housing, is excluded.

“In the near term, lower rates of household mobility and lean inventory levels of homes on the market seem to be helping the home improvement industry,” JCHS analyst Abbe Will wrote in the Center’s blog. “That, coupled with an aging housing stock and deferred expenditures during the recession, have owners catching up with delayed remodeling projects this year.”

“Home improvement spending has already recovered a significant share of its losses from the downturn,” Kermit Baker, director of the Center’s Remodeling Futures Program, was quoted as saying. “As spending moves into the next phase, we expect to see double-digit growth tail off to its longer-term average in the mid-single-digit range.”

The forecast of 9.4% growth through 2014 would have been two-thirds lower, but JCHS removed consideration of long-term interest rates from the mathematical model it uses to produce LIRA. “With the upheaval in markets in recent years, the traditional relationship between interest rates and home improvement spending has significantly deteriorated,” the Center explained. A chart on the JCHS blog shows what the LIRA would have looked like had the interest-rate factor been kept.

{kind=link}