It’s one of the most common scenarios replacement contractors face: A homeowner asks for a bid and then is surprised by how much the job costs. When that happens, homeowners have two choices: cutback on the project scope or do it in phases. Neither is a great option for the homeowner or the contractor.

For the homeowner it means having to settle for lower-grade products or repeated disruptions of their home life. For the contractor, it means missing out on a higher overall project cost and having a less satisfied customer.

“When the average ticket for a home improvement project is $10,000, if you don’t offer financing, you’re not in the game,” said Ger Ronan, owner of Yankee Home Improvement. “It will consummate the sale and make customers much more comfortable.”

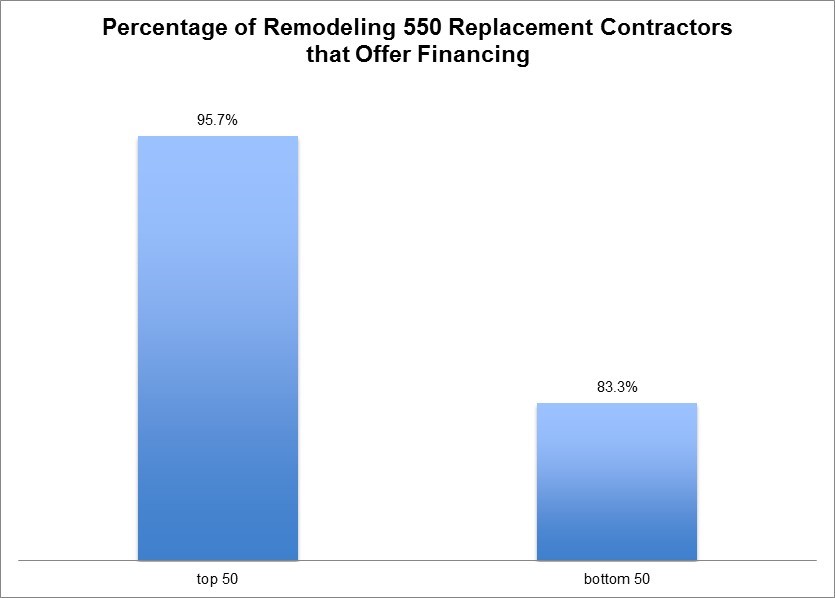

That’s why the most successful contractors make a point to offer customers financing options. The latest data from the 2018 Remodeling 550 list is a striking example. Almost 96% of the top 50 contractors on that list offer financing options, while just 83% on the bottom 50 of the list do the same.

“There’s a reasons those companies are at the top of the list,” said John Harris, sales and marketing executive vice president for EnerBank USA.

In fact, Harris said studies show that offering financing increases close rates 18% and job sizes 30%. “What ends up happening is that when you offer customers good, better, best options is instead of choosing the baseline solution, they end up picking the better or best solutions,” he said.

For example, rather than choosing basic windows, customers choose high efficiency models and do the whole home rather than just a few windows.

And thanks to technology, Harris said many of the larger contracting firms now use end-to-end software solutions to integrate financing options into the sales process. That way information that’s already being collected — name, address, etc. — can be used to auto populate loan forms. “They press a button and in a matter of seconds they get an answer about what kind of payment options they have,” he said.

Harris said the two most popular financing options are 12 or 18 months same as cash interest-free financing and more traditional financing over a period of months or years. Like accepting credit cards, contractors must often pay fees for some financing, typically around 6%. But Harris said those fees can simply be built into the cost of the job so customers are still paying for them.

Not all financing comes with fees. Some contractors work with credit unions, which offer no-fee financing and low interest financing rates.

But regardless of how contractors offer financing options, it’s clear those who want to grow their business need to consider it. “Just look at that list of contractors that are having great success compared to the ones that offer payment options,” Harris said. “That’s one of the way they got on that list.”