Many contractors have learned that it’s important to separate overhead costs (expenses) from those associated with production (Cost of Goods Sold, or “COGS”). Some of the production costs are pretty obvious. If you go to your lumberyard and buy framing lumber for the Jones job, for example, it’s a no-brainer to assign that cost to a COGS account. And some overhead costs are pretty obvious—office rent, utilities, office supplies, and the like (see Overhead Cost?, top left).

What about the costs that are associated with producing jobs, but are not necessarily associated with a specific job—costs such as small tools that will be used on multiple jobs, gas for the trucks, and communication plans for phones and tablets that are used on the jobsite? These are less straightforward to classify, but anything that is directly associated with the production process—even if it is not associated with a specific job—should be considered COGS, not an overhead expense.

Here’s another way of looking at it. Let’s suppose for a minute that you have absolutely no projects at all. It’s a horrifying thought, but it’s just to make a point. Pretend that you’re going to switch from being a remodeler to selling ice cream. What costs would you still need to pay for in order to keep the company in existence? Thinking about it this way should make it a bit easier to decide whether a particular cost is related to production or not.

But why is it important to figure this out?

Know Your Overhead to Find the Right Price

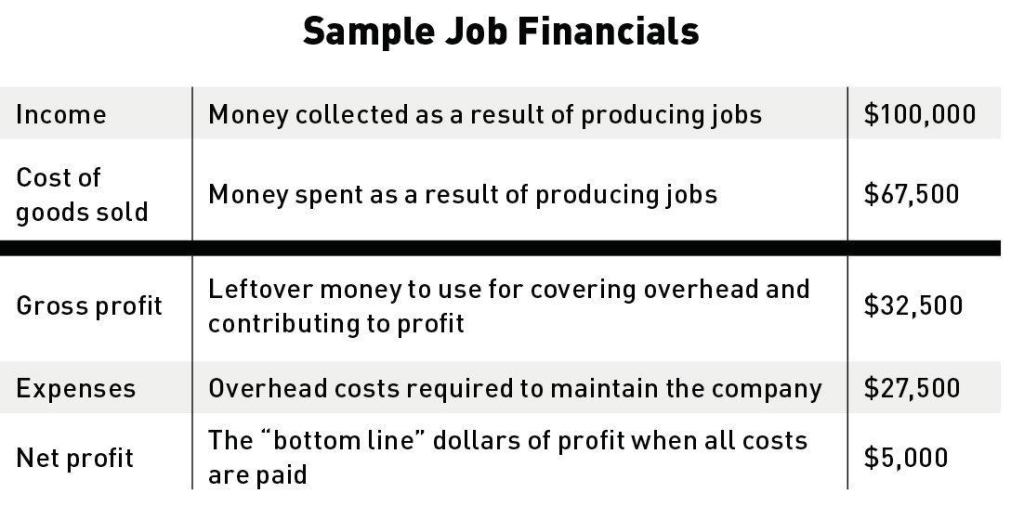

In the uncertain world of construction, there aren’t many constant and predictable figures you can put your hands on. Income (sales volume) is an unknown. Because your production costs are tied to sales, COGS is unknown. But you can predict overhead, and this becomes the basis for your figuring out how to price your work. No matter what else happens, you know you must have at least enough dollars left over when you finish producing work to cover overhead (see Sample Job Financials, above).

Hopefully, you’ll also have some left over for profit. The next part in this series will show you how understanding your overhead will help you price your work so profit won’t be left to chance.