As a financial consultant to small construction companies, I’ve seen lots of cases where a builder finished a job and the bookkeeper closed the books on it — only to have a late subcontractor bill for that job show up months later. I’ve also seen cases where material costs on a job ran as much as $20,000 over budget, but the project manager didn’t tell the boss until the project was complete. The owner thought he was making a decent profit and then got a nasty surprise.

The source of these problems isn’t necessarily the bookkeeper or project manager; it’s the process itself — which is, of course, determined by the company owner. The reason bookkeepers in construction offices often seem to be inefficient is that their bosses don’t give them the information they need. In many companies, a bookkeeper handed a stack of bills properly coded to a job would go into shock and faint; more typically, he or she has to figure out which bill goes with which job. Inevitably, such guessing leads to costly mistakes. But again, don’t blame the bookkeeper. It’s her job to do the bookkeeping; it’s the responsibility of the person buying the materials to allocate them to the proper job.

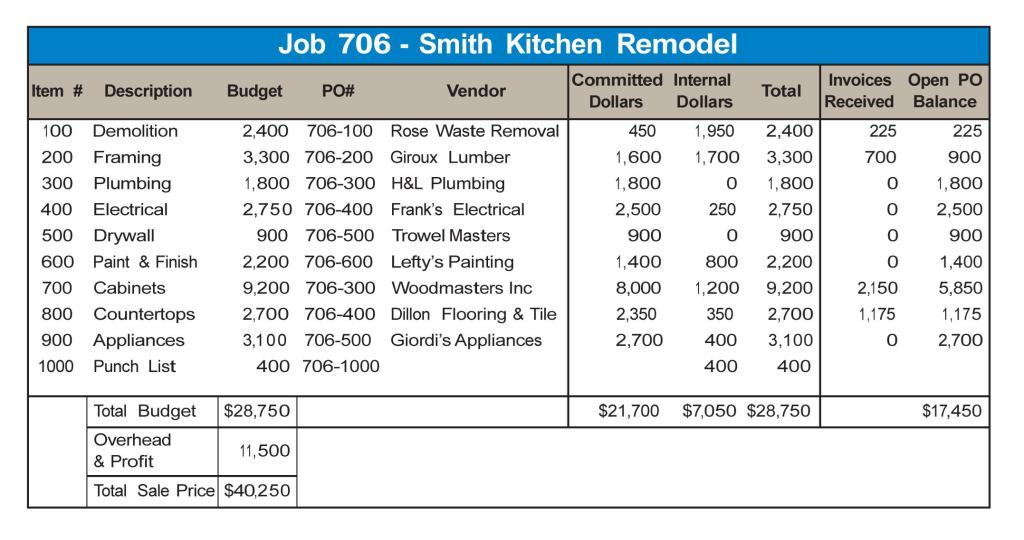

A purchase-order system allows you to keep track of a job’s expenses. All “committed” costs — essentially subcontractor payments and material purchases — receive a PO number, which gets plugged into a basic spreadsheet like the one shown here. As the job progresses, you can compare invoices received with what has been budgeted.

Speaking in Code

For that to happen, the purchaser needs to have a code to give the supplier — and the company needs to have a good purchase-order (PO) system. A lot of contractors don’t use POs because that would require planning jobs more carefully, and they don’t see much value in time spent planning. But in the examples cited above, the reason the contractors lost track of bills or didn’t know jobs were going over budget was that they lacked a PO system.

With a good PO system, you calculate at the start how much you’re going to spend on each part of the job (or, for very small projects, on the entire job), and you create a budget for that amount. Most small contractors already do that, based on the job estimate.

The next step is to assign costs to suppliers and subs. Then, whenever a crew member working on the project buys materials, or a subcontractor submits a bill, he provides a PO number that links the bill to that job and to the proper phase. The payoff is that you and your bookkeeper will always be able to see how much you have left in the budget, and therefore whether the job is on track.

Committed Costs

The biggest advantage of a simple purchase-order system is that it helps you keep track of “committed” costs. These are costs you have very little control over once the job is under contract — material and subcontractor costs are the best examples. By contrast, your “internal” costs — primarily your own labor costs — are under your control.

To use the PO system, go through your job budget and determine which line items are committed costs and which are internal. Then issue a PO number for each committed cost and set up a spreadsheet — like the one shown on the previous page — so you can tell as the job progresses where you stand against budget and where you have money left to work with.

Say you exceed your labor budget for demolition. Since it’s early in the job, you can still make up for this on one of the other phases — as long as you use internal money. You know, for instance, that there’s unspent money set aside for the cabinets and you don’t have to pay the balance for them until near the end of the job. But the spreadsheet makes it clear that those dollars are spoken for and you’ll have to find the savings elsewhere.

A simple kitchen remodel like the one in the sample spreadsheet uses several suppliers and subs. Each cost is assigned a PO number — based on the job number and phase — that should be given to each sub or vendor and to any carpenters who might be purchasing materials.

It’s smart to have a rule: No PO, no payment. Once your subs and vendors get used to it, they’ll make sure they include POs on their invoices. Having to provide POs will also reduce those impulse purchases at the lumberyard counter; everyone is accountable for what he buys.

No More Overpayments

The PO system also eliminates another common problem: overpayments. Let’s say a sub has a contract for $8,000 and bills for $4,000 at the beginning of the job, but doesn’t get paid. Later, at the end of the job, he sends a second bill for the full $8,000. The bookkeeper — who in this scenario doesn’t have a PO number to compare the bills against — pays the sub $12,000. By the time the contractor figures out what happened, he may not be able to get the money back. An updated PO spreadsheet would have made it clear how much the sub was owed and how much he had billed for.

Simpler Still

Even if you decide not to use a purchase-order system, you should at least have what I call a “purchased order” system. All you need are line-item numbers and job numbers.

Say item number 6000 is framing lumber; when you buy lumber for job 63, you give the supplier 63-6000 for the PO number. This won’t let you compare actual numbers with budgeted numbers or know what has already been committed, but costs will get credited to the right job and the right line item, and the bookkeeper will know the job number and line item without having to ask.

Creating Codes

When creating a budget, resist the impulse to use too many codes. That may mean not listening to your project managers, who often want to job-cost at the same level of detail they create estimates.

I had one client who ignored this advice and, rather than use one line item for countertops and tile, created a list that included separate codes for master-bath tile, master-bath granite, master-bath Corian, first-floor bath granite, first-floor bath tile, and so forth. Don’t make this mistake. Not only will the bookkeeper balk at entering costs with that level of detail, but the sheer number of categories will make it too hard to get an accurate picture when you’re comparing budgeted costs and actuals. The ultimate outcome could be that everyone gives up and decides that working from a budget is too hard. So keep it simple.

Leslie Shiner is a financial and management consultant for builders and remodelers. Her office is in Mill Valley, Calif.