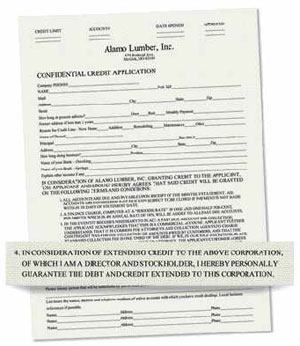

Most credit applications contain a personal guaranty. In this one, it’s clearly spelled out in item No. 4, but in some cases it’s buried in a longer document and written in language that makes it hard for the applicant to understand just what he’s agreeing to.

When the owner of a new or small business applies for credit, he or she is frequently asked to provide a personal guaranty. The guaranty is a contract between the owner and the creditor that in essence says, “I agree to be personally responsible for the debts of my business, so if the business doesn’t pay, I will.”

This has little effect on sole proprietors because their personal assets are already at risk for their companies’ debts. But a guaranty presents a dilemma for the contractor who has incorporated as a corporation or limited liability company (LLC). These business entities are designed to prevent creditors from accessing the owner’s personal assets. When an owner signs a personal guaranty, he is giving this access back to the creditor.

The trick for the small-business owner is to understand when to give the guaranty.

Why Creditors Want a Guaranty

Creditors often request a personal guaranty when the creditworthiness of the business is limited. The guaranty is used to enhance credit by making personal assets — otherwise unavailable to the creditor — available to satisfy the debt.

Assuring payment. There are other reasons creditors might want a guaranty. For example, they might want to use it as leverage to assure payment. They reason that if a business owner has to pay two debts, he will first pay the one that puts personal assets at risk. If the business goes under before the second creditor gets paid, that’s just too bad — it’s the second creditor’s problem.

It’s worth noting that if the business does file for bankruptcy, the court may undo recent preferential payments.

In leasing transactions, a guaranty for moveable equipment may provide greater assurance that the equipment will not “disappear” if there is a default by a failing company. In other transactions, the reason is simply “Let’s put it on our form and see if we can get it.”

Form of Guaranty

When a bank or equipment-finance company requires a guaranty, the guaranty is typically on a separate form or in a labeled section of the loan agreement and is often several paragraphs long.

Trade creditors, such as supply houses and lumberyards, often bury a single-sentence guaranty in the credit application form; it’s easy to miss if you don’t read the fine print. The sentence may say something like this: “The undersigned, even if a title is stat-ed, personally guarantees the prompt payment of all amounts due from the applicant and agrees to be jointly and severally bound with the applicant for any debt owed by the applicant.”

Who should sign. If a guaranty must be signed, a business owner should be the guarantor — not a nonowning officer or employee. The bookkeeper or salesperson who signs and submits the credit application with a guaranty for the boss could be in for a surprise when he or she becomes liable for the company’s debts.

If there is more than one owner, it is usually best to make all owners liable and to share the risk, preferably in a ratio reflecting the ownership of the business, although most creditors will require joint and several liability.

You may want to consult an attorney to draft an agreement between the owners that says that if one owner provides a guaranty on an authorized debt, all the owners will be responsible to him if he has to pay a share in excess of the percentage he owns.

Limiting Potential Damage

There are ways to limit the potential damage of a guaranty. The party requesting a guaranty will want it to be completely unlimited, but remember that this is a contractual agreement, so it should be negotiable.

If you do have to sign a guaranty, you want it to end as soon as possible; a guaranty puts personal assets at risk, and having too many of them can make you less creditworthy for future loans.

Expansive guaranty. A guaranty may be very expansive. It may cover all debt, including previously existing debt or other debt that one of the owners owes the lender. You may be able to limit the scope of the guaranty to that transaction only.

The point is to carefully read all guaranties. If you have any questions, consult an attorney.

You may be able to avoid giving a guaranty to a banking lender by showing creditworthiness. If your entity has a net worth of $100,000 and you sell only on a cash basis, there is probably not much risk to a creditor if you want an open credit of $10,000. But if you want to borrow $1 million to build your own building, you should expect to give a personal guaranty.

Other situations may not be as clear for the small-business owner.

Ending the guaranty. Many lenders require a personal guaranty for real estate and development loans if the borrower doesn’t have a large equity stake in the property. Equipment-financing transactions may also require a personal guaranty. You may be able to arrange a “burn-off” of the guaranty — that is, a guaranty that ends before the final payment or when the “equity investment” exceeds a stated percentage or dollar amount. This is good because it makes the guaranty end sooner.

Leasing agreements. If you have to sign a guaranty in connection with an equipment lease, be sure to maintain control over the equipment so that you can return it. If someone else ends up with the equipment and won’t give it back, you’re the one who has to pay.

The Client’s Debts

If you’re a remodeler, you do not want to guaranty the debts of your customers. But you may already be doing so if you are ordering nonreturnable items or making deposits with your own money based on the property owner’s promise to pay you.

I tell my contractor clients to include language in their contracts requiring the customer to pay all deposits and potential restocking fees in advance, and then to collect those amounts before placing the order. If there is going to be a very large dollar order from a particular supplier, you might want to have the owner open an account with that supplier and pay him directly. Just be sure that your contract allows you to mark the material up.

Lien rights. In many states, if the supplier delivers material to a remodeling site (rather than to your warehouse), the supplier will have lien rights against the property owner. You may be able to convince a supplier to open a separate account that you do not personally guaranty for material that will be delivered to sites where there’s a lien right against the owner.

Credit Cards

Credit cards opened in the name of the business may in some instances have a personal guaranty. Be cautious giving these cards to an employee. You may want to explore whether a credit card can be limited to the assets of the business, even if it costs you an annual fee.

At minimum, be sure that these cards do not have excessive credit limits.

Kevin M. Veler is an Alpharetta, Ga., attorney with 20-plus years of experience representing companies in construction, real estate, and general business transactions.