by Anne W. West

Ask any deck builder which he’d rather do, hammer nails or punch a calculator, and few, if any, will pick the latter. In fact, most deck builders consider themselves tradespeople first and businesspeople second.

Here’s a common scenario: A deck builder goes into business for himself after seeing how much the contractor he worked for was charging for labor. Instead of making $15 an hour working for the contractor, he starts his own company and charges $20 an hour for his time. Months later, he can’t understand why the business is losing money.

Business experts, however, can quickly point to a number of reasons. The builder hasn’t factored in the costs of overhead, nonproductive time, and insurance. He hasn’t built in the right rates for estimates. He hasn’t looked beyond his hourly rate to develop a solid financial plan for his business. In a nutshell, he’s been thinking like a tradesperson, not a businessperson.

That mindset must be reversed for a builder to be successful. Melanie Hodgdon, president of Business Systems Management, in Bristol, Maine, says of deck builders, “They should be thinking of themselves as businesspeople delivering the service of deck building instead of as technicians building a deck. Builders tend to focus outward on each job instead of inward on the business they are running.”

Expert help is available. There are companies and consultants who can help set up a business plan. There are multiple versions of accounting and planning software. SCORE (Service Corps of Retired Executives, www.score.org) offers guidance for free. Still, many contractors decide they can do it all themselves, or they might have a family member take care of the financial aspects of the business. Regardless of how they choose to manage their business, contractors can avoid some common mistakes by paying attention to the following seven areas.

Understand the True Cost of Labor

It’s not uncommon for contractors to use rule-of-thumb approaches for the money end of their businesses. But the contractor who simply doubles the hourly wage he’s paying his workers is oversimplifying the situation and likely won’t realize a profit. “What you charge for labor has to be based on your true burdened labor costs. It has to be marked up sufficiently to cover your overhead and to attain a target profit amount,” says Hodgdon.

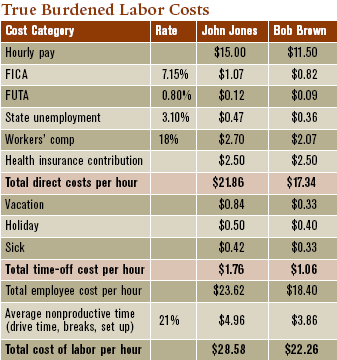

True burdened labor costs include hard and soft costs. Hard costs are what you actually pay the employee, including wages, taxes, and benefits. Hodgdon points out soft costs often are overlooked — some examples are workers’ comp, liability insurance, and mileage and tool reimbursement; also uniforms, cell phones, and vehicles, if those are supplied to the employee. Another factor to consider when determining true labor costs is nonproductive time like paid holidays and vacation, time in meetings, and time spent getting to and from a job. “Any time when they aren’t banging nails is nonproductive,” she notes.

Not having the proper productivity factors and labor rates can dramatically impact the company’s bottom line. “When you account for down time, lost time due to weather, and delivery delays, your actual time swinging a hammer may be cut to 30 hours a week,” says Bob Kovacs, an independent construction consultant in Iselin, N.J. “You need to estimate [additional] hours to cover the costs of that lost productivity.” In other words, if you think that actually building the deck will take 30 hours, you should price it at more like 40 hours to account for the nonproductive time.

Knowing the true hourly cost of your workers is critical to job costing and measuring profits. It's not hard to break down, either. Multiply the dollars per hour by the rate — for costs such as workers' comp that are figured as percentages — or divide the annual cost of, say, vacation pay by the number of hours an employee works per year.

Do Simple Job Costing

“People are pricing based on intuition at a point in time (during the sales cycle) when they are motivated to keep the numbers small,” says Richard Steven, president and owner of Fulcra Consulting in St. Paul, Minn., and Seattle. “Job costing provides objective feedback about the true cost of that job.” (See “Labor Costs,” PDB, September/October 2007.)

Steven says most builders avoid job costing because they think it’s too complex. He says they make it complex by unnecessarily breaking big categories such as labor into smaller ones like framing or finished carpentry. “Job costing is that information that is at the heart of your business. Ninety percent of job costing is to add up all materials, labor, and subcontractor costs, finding the actual costs in each of those big categories,” he says.

Job costing can show if your estimates have been profitable, assist with more accurate current and future estimates, and eventually sustain the business. “It’s the old adage of not sharpening the saw,” notes Steven. “If you don’t take the time to do it and your estimates are significantly inaccurate, you will go out of business.”

Carefully Estimate All Costs for Each Job

Be sure to include the correct price of all building materials and supplies, equipment rentals required, cost of hauling materials to the site, and replacement tools. Visit the site to be sure it doesn’t require special equipment, altered construction techniques, or more time physically getting manpower or supplies to the site. This sounds basic but it’s often overlooked.

The contractor also has to build in a material waste factor for each job. “Make sure you have enough material waste factored into the job, whether that’s due to the unique layout of the project or the materials themselves,” says Kovacs. Even though some lumber yards may take back poor-quality wood, the contractor must be prepared to absorb the cost of unusable material, plus the cost to dispose of it.

“How many contractors buy another shovel because they lost one at the last job?” Kovacs asks. “Even though it’s an inexpensive item, $15 per shovel adds up over the course of the year.” He suggests adding an estimate line item for miscellaneous tools to cover lost shovels, tape measures, trash bags, trash cans, and other minor items that are considered routine on every job.

It's easy to remember to include regular costs like labor and materials when bidding a job, but every job has some costs that may not occur in every bid. Using a spreadsheet that reminds you of these costs keeps you from eating them. And adding in a small amount to cover unpredictable costs such as tool loss keeps those eventualities from impacting your bottom line.

Understand Gross Margin and Net Profit

In simple terms, gross margin tells you how much profit your company earns relative to the cost of producing its products or delivering its services. (The term “gross margin” as used in this article describes that profit in dollars. Other authors may use the term “gross profit” for the dollars and “gross margin” only when expressing the profit as a percentage.) Cost of goods sold includes all costs incurred specifically to produce a job, such as materials, direct labor, subcontractors, permits, portable toilets, dumpsters, and project management.

Gross Margin = Total Sales Revenue – Cost of Goods Sold

Gross margin is the amount needed to cover operating expenses (overhead such as liability insurance, office space and equipment, sales salaries, and the like) plus net profit. “It’s important because, regardless of the gross margin on any one job, if the company doesn’t earn enough total gross margin to cover operating expenses and provide a net profit, it will not be self-sustaining and will go bankrupt without cash infusions from a source other than sales,” says Steven. Gross margin can also be expressed as a percentage, to show the ratio of gross profit to sales revenue:

Gross Margin Percentage = (Revenue – Cost of Goods Sold) x 100

Revenue

Gross margin plays a role in markup and estimating, and it demonstrates the relationship between financial analysis and estimating. “In remodeling, a 30 percent gross margin is common. To get that margin, you don’t mark up your costs by 1.3. Instead, you apply a multiplier of 1.43. You have to understand what multiplier you need in your estimating to achieve your targeted gross margin,” says Steven.

Steven explains that the multiplier (or markup) is always higher than the gross margin number because it is a factor of the cost rather than of the price. Consider this example of how a contractor with a targeted gross margin percentage of 30 percent arrives at a multiplier (or markup) of 1.43, using the following formula:

Sales Price = Cost of Goods Sold ÷ (1 – Gross Margin Percentage)

First, he identifies his targeted gross margin percentage. Next, he calculates the job costs. If job costs are $100 and the desired gross margin percentage is 30 percent, then the sales price must be $142.85:

Sales Price = $100 ÷ (1 – .30) = $100 ÷ .70 = $142.85

To find the multiplier to use on future jobs (rather than having to redo all this arithmetic), just divide the sales price by the job costs:

$142.85 ÷ $100 = 1.43

Simply multiplying the cost of any job by 1.43 (as long as your cost estimate is correct) will give you the sales price you would need to charge to earn a gross margin percentage of 30 percent.

Understanding the gross margin also helps a company prepare the next year’s budget. Gross margins that are too low mean the business can’t cover the costs of operating. The business will need to either raise prices or lower operating costs to realize a profit.

Know Your Numbers

“Pay as much attention to your financials as you do to that set of plans for the next project,” advises Hodgdon. “You have to get your financial numbers in a readable form and have the reports that you need to make good decisions for the company.” In other words, you need to be able to see at a glance if you’re making a profit, what bills are coming due, and if you’ll have cash on hand to pay them. Up-to-date information allows you to identify and correct bad trends before they wreak havoc on your bottom line.

Hodgdon says deck builders fall into two categories — those who make the investment to correctly set up their financials and understand them and those who prepare financials only to generate a tax return. The first group invests in the appropriate accounting software, usually trains someone in the business to use the financial system, and generates regular reports that show where the business is and where it needs to be. “They trust the results. Their accounting file is a day-to-day guidebook for decision making,” she says. Hodgdon adds that the responsible person needs knowledge in three areas: accounting, the construction industry, and software.

The second group uses an accountant or a family member to maintain the accounting files and often loses information that can impact business decisions because the focus is only on income tax preparation.

“Set the software up right and use it properly. Make it do what the company needs it to do. It’s just like how you use lumber to build a deck. Having a pile of lumber in the yard isn’t enough to build a deck,” says Hodgdon. In addition to providing a complete picture of the business’s financial health, knowing the company’s numbers can provide a competitive edge in winning new business. For example, there is no “going rate” in deck building. Instead, a builder has to understand the range of rates in the market. “If the range is between $8 and $12 per square foot and your numbers show you need to charge $30 a square foot, your business model isn’t going to work,” Kovacs points out.

Carefully review your process for producing a quality product in the market and identify the factors that are causing your price to be higher than the competitor’s. This investigation and comparison sometimes presents an opportunity to up-sell or market differently. “Maybe you find out that the competition isn’t building to code or pulling permits for the job,” says Kovacs. “You can explain to the client that your price is higher because you build to code and secure permits. You can promote the fact that they won’t have a problem when they sell their house.”

Keeping tabs on your profits requires that you first find your gross profit by tracking and comparing job costs and job incomes. From your gross profit, deduct the overhead costs of running your business to reveal your bottom line.

Project Cash Flow

“The number one mistake deck builders make is not buying materials and covering other costs with their client’s money,” Hodgdon says, adding that when a contractor fronts the cost of material, permits, and design, they are in effect giving the customer an interest-free loan. “I’ve seen instances where, because of cash flow crunches based on this kind of error, the company is forced to draw a line of credit and pay interest to get sufficient cash to provide their client with an interest-free loan.”

Builders may not think about the costs incurred before the job starts, such as overhead in selling the job, estimator salaries, the cost of delivering materials to the site, or equipment rental deposits. Getting a substantial deposit before the work begins helps eliminate the cash flow problems that can occur before each job.

Steven suggests taking cash flow a step further. “Plot all the jobs on a grid along with the projected schedule for payment, and you have a realistic idea of projected income,” he says. “Compare that with projected cash out such as payroll, supplier purchases, and insurance payments. You’re not looking at profitability; you’re looking at cash in, cash out.”

Projecting your income and outgo for each month identifies times when you might not have the cash on hand that you need. Knowing ahead of time allows you to address an occasional cash crunch by, for example, accessing a line of credit.

Maintain Your Equipment

A contractor who bases each estimate on the assumption that everything needed is available and in good working condition may be setting himself up for trouble. That approach requires all the tools and equipment to function properly for the estimate to be accurate and the business to realize a profit.

Yet, equipment maintenance is often overlooked until a malfunction brings the job to a screeching halt. Failure to maintain equipment can bring about significant delays and financial losses, so experts recommend setting aside time to prevent such mishaps, as a normal part of business.

“Budget a certain amount of time for ongoing maintenance,” says Kovacs. “Take one day a month and allocate and budget for it in your productivity numbers to cover equipment maintenance, vehicle service, or sending people to training classes.” He also suggests that instead of sending employees home on a rainy day, to use that down time as an internal maintenance day. •

Anne W. West is a freelance writer in Dunwoody, Ga.