When building professionals talk about how their businesses are doing, they often quote sales figures. “We’re already ahead of last year’s sales and it’s only October,” they’ll say. What is rarely mentioned is profit.

We can look at profit in two ways: in dollars (gross profit and net profit) or as a percentage of sales (gross margin and net margin). Let’s examine both.

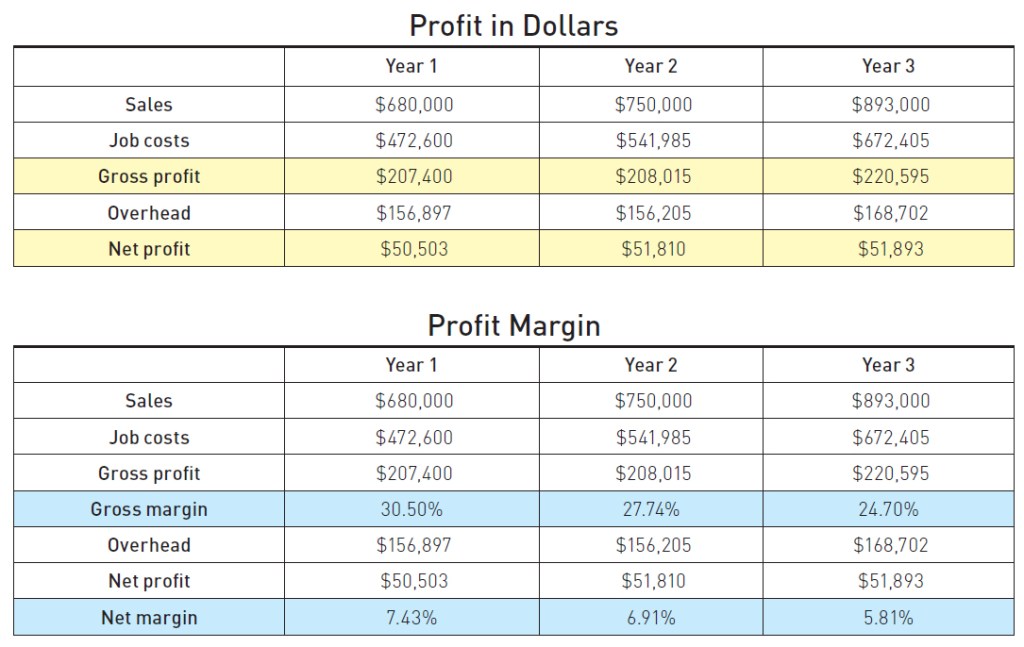

Profit in Dollars

Profit can be described as whatever is left over from sales after you deduct your project costs and your overhead. Profit exists in two forms:

Gross profit is what’s left over after you deduct your production costs from your income.

Net profit is what’s left over after you deduct your overhead costs from your gross profit.

Margin

Margin refers to the percentage of sales due to profit. For a simple example, if sales are $100 and your job costs to earn the $100 are $68, that leaves you with $32 of gross profit (what’s left over after your project costs are deducted from sales). The $32 of gross profit is 32% of your sales ($32 / $100), which is your gross margin.

Then you have to also deduct the costs of maintaining the company (overhead). If that’s $25, the $7 left is net profit. That’s equal to 7% of your sales ($7 / $100), which is your net margin.

While it’s tempting to look at profit in dollars, it’s more important to look at margin. Since margin is shown as a percentage, you’re not likely to be confused by figures that differ each year. If the margin is going up, you’re squeezing more profit out of every sales dollar. That’s a good thing!

For example, look at the financials in “Profit in Dollars” on the previous page. The numbers look great! After all, each year the company is showing increases in sales, gross profit, and net profit. That’s what’s important, right?

But what happens if we add margin figures to the same table (see “Profit Margin,” previous page)? All of a sudden, it’s easy to see that both gross and net margins are steadily falling. That means it’s actually costing the company more, proportionately, to produce work. If this company continues the trend, it may fall into the trap of believing that it needs to sell more work (less profitably) to try to make up for dwindling profits. We call this the “Death Spiral.”

Added to this downward spiral is the likelihood that as the number of projects grows, staff will need to be added in order to manage the additional jobs. This will cause overhead to spike, lowering net figures even further.

Correct Pricing Is The Solution

Instead of focusing on more sales, focus on selling jobs at the right price, and producing each job as efficiently as possible. You may find that if you do this, you will be able to sell fewer jobs (requiring lower management costs) at a higher profit and make a better bottom-line figure than you did when you were selling more jobs with lower pricing.

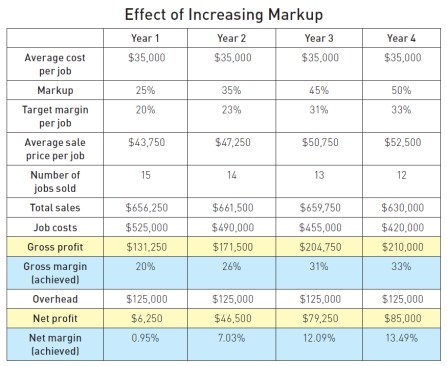

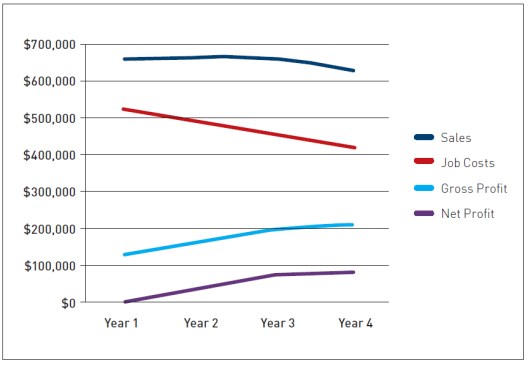

The table and graph below shows a four-year cycle during which a company’s average job cost and overhead costs are consistent. Note that by increasing the markup, this company actually produced fewer jobs and lowered its total sales volume while increasing its bottom line.

The key is selling jobs at the right price, and this may mean increasing your markup so you are realistically covering your costs.

Over a four-year cycle during which its average job cost and overhead remained consistent, this company increased profits by increasing markup. The company produced fewer jobs and lowered total sales volume, but the jobs it did produce were higher-value ones.

Do not be enticed to try to increase your sales dollars unless you’re simultaneously increasing your achieved margins. There’s no point in making yourself crazy (and possibly damaging your reputation) by focusing on sales dollars. Wouldn’t you rather concentrate on selling a manageable number of jobs to well-qualified prospects and sending more to your bottom line?