The longer you’ve been in business, the more war stories you accumulate about how a project fell apart due to inclement weather, power losses, forest fires, loss of your most responsible carpenter, or the homeowners who morphed into the customers from hell as soon as the contract’s ink was dry. You can’t predict the nature and timing of the next disaster, but you can draw on your experience to smooth out some of the inevitable ups and downs of your business.

There are three categories of risk—financial, contractual, and operational—that you can assess about a job.

Financial factors include the amount of cash reserves, the timing of your billing, and the likelihood that the customer will pay you on time.

Contractual factors include the clarity of the scope of work and change-order process, and how accurate and current your legal documents are.

Operational factors include how familiar the work to be performed is, the quality of the crew and project manager, availability of the appropriate equipment, insured status of subcontractors, and the likelihood that required materials will be available on time.

Once you’ve considered a prospective job’s risk factors, how can you quantify this in a useful way? Obviously, if a job looks too risky, you should walk away from it. But let’s say it doesn’t.

If you price a risky job accurately enough, you are more likely to make a profit—or scare the prospects off.

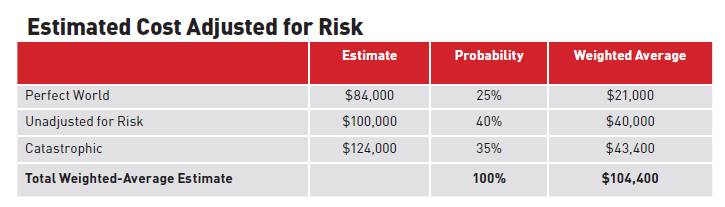

First, come up with an estimate for the job, unadjusted for risk. Let’s say $100,000. Next, come up with “perfect world” and “catastrophic” estimates for the same job. This is where your gut and years of experience come in and where you can consider the likelihood of bad weather, crew loss, sour customers, and so on. Assign a probability for each scenario. For example, you may feel that there’s a 40% chance that the job will run as usual, 25% that conditions will be perfect, and 35% that the job will be a disaster (note that the probabilities must add up to 100%).

Create a table like the one above. Complete the “weighted average” column for each of the three conditions by multiplying its estimated cost by its probability. The total of the weighted averages reflects the estimated job cost including risk. In this example, 4.4% was added to the estimated cost to account for risk.

While you can’t see the future, you can provide a cushion against the inevitable. Your final step will be to add a markup suitable for your company’s overhead and its target profit, based on the total estimated cost adjusted for risk.

This article originally appeared in Remodeling.