Labor burden refers to the costs above and beyond wages that a company incurs as a result of having employees. Most companies are only concerned with burdens as they are linked to production employees, since knowing these costs contributes to appropriate pricing and accurate job costing.

For most remodeling companies, burden consists of some or all of the following:

- Payroll taxes

- Worker’s comp insurance

- Liability insurance

- Benefits such as retirement, health, and dental contributions

- Other costs related to field workers including vehicle and communications

- Paid time off

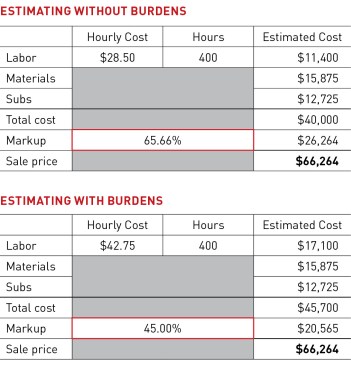

The impact of these burdens on financial and job-costing reports can be significant. Basically, the more generous and numerous the burdens, the larger the gap between the base hourly wage and the burdened cost per hour. When working through labor burden calculations with clients, I often see examples such as $28.50/hour for wages and $42.75/hour for burdened figures. This translates to a 50% cost increase due to burdens.

If you estimate without a fully burdened labor cost (top), you may be able to make up for it with a higher markup to price the job accurately. Note the difference in estimated costs (bottom).

There are multiple implications associated with not knowing your fully burdened costs, which I will cover in this article.

Estimating

If you estimate using a partially burdened cost for your labor, you risk underpricing the job. It’s that simple.

Some companies address this risk by putting only wages above the line and putting all burdens in overhead. This inflates overhead, and provided that they base their markup on a formula consisting of overhead and achieved margin (see charts “Estimating Without Burdens” and “Estimating With Burdens,” left), they may succeed in pricing the job correctly. Their markup will simply be higher than that of a company putting burdens above the line, but based on a lower estimated cost. The job price can be the same, but there will still be issues when it comes time to job cost and calculate work-in-progress (WIP) adjustments.

Job Costing

Let’s say that you have decided to estimate using burdened labor costs, but your software doesn’t allow for burden. It may pick up wages and payroll taxes and possibly worker’s comp and assign those to individual tasks and jobs successfully, but other burdens may be missed. So, you may be estimating at a fully burdened rate but job costing at a partially burdened rate. This is what you’ll need to watch out for.

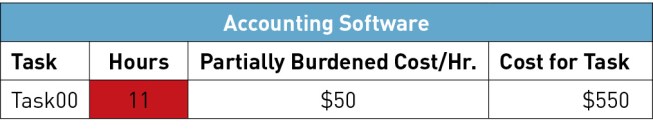

Focusing on a single task, “Task00,” let’s see how this plays out: Say you have calculated your burdened hourly rate at $60. Your estimate allows 10 hours to complete this task. Therefore, the estimated cost to complete Task00 is $600 (below).

However, if your software includes only partial burden, it may display an hourly cost of $50, not $60. When you review your job cost report, you note that Task00 “cost” $550. Since the estimated amount was $600, it appears that you are $50 under budget.

But wait! Task00 actually took 11, not 10, hours. Because the software applied only a partially burdened labor cost, it calculated a deceptively low cost of $550 (11 x $50) for the task (above). At the fully burdened cost of $60/hour, however, the actual cost for the task was $660 (11 x $60) and you’re over budget by $60 (below).

Obviously, this discrepancy will inflate as the size of the job or proportion of labor within the job increases.

Such reporting errors can lead to unfortunate results, such as bonusing or profit-sharing on a job that is less profitable than it appears. It can also cause estimators to think they are overestimating the length of time it takes for a task to be completed, which can lead to underestimating and underpricing the next job.

Work In Progress Adjustments

Sophisticated companies know that it’s important to differentiate between dollars that you have received and dollars you have earned. In this case, “earned” refers to the calculated amount of incoming dollars that correspond proportionally to actual costs incurred on a job-by-job basis. In other words, if you have taken a $50,000 “deposit” from a customer to hold their place in your schedule but have incurred no costs for their job yet, then you have not earned those dollars and they should not be included when showing ordinary income on your profit and loss statement (P&L).

One way around this is to use WIP (work in progress) adjustments to your income in order to correct a P&L to show earned income rather than income.

Note: The term “income” properly refers to your “bottom line” profit at the bottom of a P&L, while “revenue” refers to dollars that come in as a result of your conducting ordinary business. However, many popular accounting software packages use the term “income” in place of “revenue,” or mix and match them. For the sake of clarity I will use the term “actual revenue” to refer to all dollars coming in from customers and “earned income” to denote the results of applying WIP adjustments to this revenue.

The WIP process has three steps:

1. Calculate percent complete by dividing actual costs to date by total estimated costs.

2. Apply this percentage to the job price to establish earned income.

3. Adjust the income figure on your P&L with a WIP adjustment to display earned income. This adjustment may be done on a job-by-job basis, or all jobs may be put into the calculation and a single adjustment applied to reflect the net of all jobs.

Let’s apply this to two example jobs:

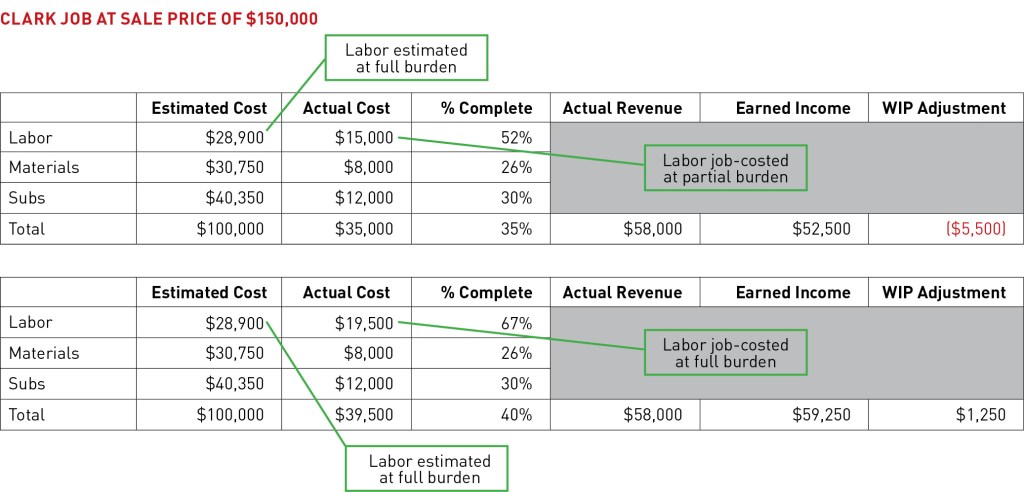

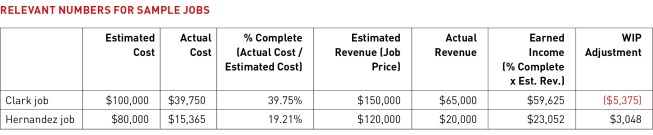

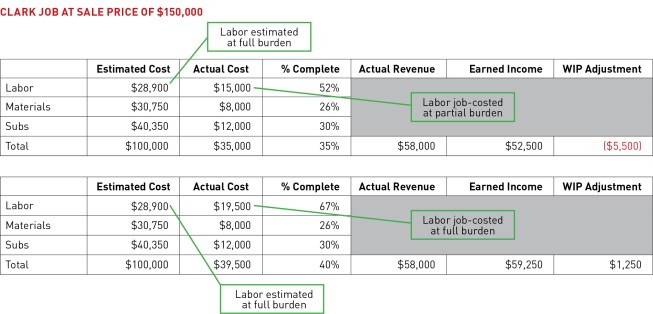

Clark job. Estimated costs for the Clark job are $100,000. The job was sold at a 50% markup for $150,000. The job costs to date are $39,750, and the invoices to date total $65,000.

Hernandez job. Estimated costs for the Hernandez job are $80,000. This job was sold at a 50% markup for $120,000. The job costs to date are $15,365, and the invoices to date are $20,000.

As of the first reporting period, the chart below shows the relevant figures for each job.

In the case of the Clark job, the customer has been overinvoiced (revenue—what has been invoiced—in excess of earned income) and the WIP adjustment is a negative number. In the Hernandez job, the customer has been underinvoiced (earned income in excess of revenue) and the WIP adjustment is a positive number.

Note that any time your actual invoices are lower than your earned income, you are no longer paying for job costs using the customer’s money. You are providing them with an interest-free loan. It should be obvious, then, that the “Actual Cost” amount should be as accurate as possible.

The “Estimated Cost” of labor in both charts above includes full burden. In the top chart, however, labor is job costed with partial burden (apples to oranges), which throws off “Earned Income” and results in a negative WIP adjustment. In the lower chart, labor is job costed with full burden (apples to apples), resulting in a higher amount of earned income and a positive WIP adjustment.

So what happens if you aren’t using a burdened figure? If your actual labor cost is understated (without burdens, as shown in the top chart, above), then “% Complete” will be inaccurate. Since your earned income figure is based on that percentage, your earned income figure will be incorrect. Since your WIP adjustment is based on the discrepancy between reported income on the P&L and earned income from your WIP calculator, your WIP adjustment will be wrong.

In a perfect world, you would be able to assign a 100% accurate burdened cost to each employee. This will never be possible down to the penny. However, it makes sense to either commit to calculating and then estimating, job costing, and performing WIP adjustments that take into account labor burden to the best of your ability or, at the very least, recognize the potential pitfalls of not doing so.