On the heels of the Great Recession, I had to find a job. With 20 years of home building behind me, there was little else I knew well enough by which to make a decent income. Want ads for experienced home builders didn’t exist, but I found that skills honed in construction and remodeling provided a good base for careers in real estate sales, building inspections, and property insurance adjustments. I explored all three.

If you’re looking for a career change today, it’s likely not because of a sluggish construction economy; things have picked up. But your knees and elbows may need a break, or you may have other reasons to trade in the toolbox for a briefcase. Let’s face it, construction is a younger man’s game. It’s also fraught with risk and uncertainty, even in good times. After I switched careers, my stress level diminished, my bank account recovered, and I have no warranties to worry about or employees to pay on Friday.

INSURANCE ADJUSTMENTS

The most satisfying and lucrative work I found involves adjusting insurance losses after catastrophes, such as 2013’s Moore, Okla., tornado and Superstorm Sandy. You’re helping people in need, and you make a percentage of every loss you adjust. Working 16-hour days while on storm duty, you can earn $750 to $2,500 a day, on average. Since 2008, I have been deployed 30 to 60 days a year, and in that brief but intense time, I make about half my annual income.

But it’s not an easy job, and you do earn the money. Big natural disasters are chaotic, the workload is overwhelming, the phone calls are incessant, and you never know when you’ll be deployed. Notice comes in two phases: First you receive a text alert that deployment is likely, then a call a few days (or sometimes hours) later telling you where to go for orientation. When that call comes, it means leaving within 24 hours. I keep two plastic totes with all of my supplies ready to load in the trunk, and I pack my suitcase on first notice.

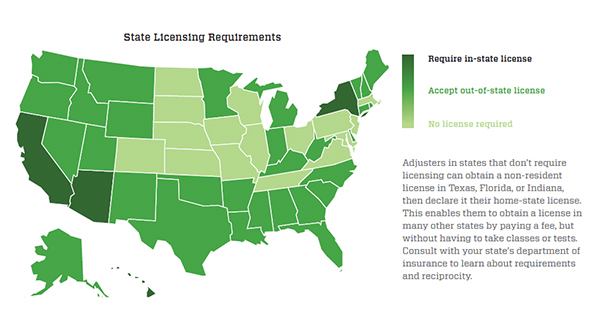

Licensing. To become an independent catastrophe, or “CAT,” adjuster, you have to obtain a license. Check with your home state’s department of insurance to find out what the requirements are (see map, page 52). You would begin by applying for an “all lines” or casualty and property adjuster’s license in your own state. Some states, such as my home state of Colorado, don’t require a license, but without one, nobody takes you seriously.

Licenses from Texas, Florida, and Indiana are among those that enjoy the highest level of reciprocity. Having one will allow you to obtain a license in most other states just by paying the fee—no tests or classes required. (The exceptions are Arizona, California, Hawaii, and New York, which require separate licensing.)

If your state does not require a license, you can obtain a nonresident license in Texas, Florida, or Indiana and designate it as your “home state” license to enjoy most of the benefits of reciprocity. Texas offers the greatest number of approved adjuster license courses, many of which are online. Its license is the most widely recognized in the industry, so it’s generally the one recommended for those starting out.

Another reason to get a home-state license is that insurance companies prefer to deploy adjusters already licensed within the disaster area in the first wave, before a state of emergency is declared. And they often employ locally licensed adjusters to stay afterward to handle any additional damage discovered after the initial claim. That said, states often waive their license requirements in a state of emergency, granting temporary emergency licenses to out-of-state adjusters.

For a license, you’ll need to complete the 40 hours of required training, pass a test, and submit your application to the regulating authority. For Texas and Florida, this entails fingerprinting and a criminal background check. Usually you will receive your license within a few weeks. Indiana currently does not require fingerprinting, and its process takes less than one week.

Once you have a home-state license, it’s a good idea to get licensed in areas where big storms occur, such as along the Atlantic coast, or in underserved areas where few independent adjusters have licenses, such as Arizona. In every instance, you’ll need to take continuing education classes to maintain your primary license.

Training. Your background in construction establishes a good foundation for this type of work because one of the job’s two basic skills is creating estimates, which you already know how to do; the other is determining how the insurance policy responds to the specific loss, which will be a new area of expertise.

After obtaining your license, you’ll need to learn to use Xactimate, the estimating program used by 75% of the insurance industry. You can learn the basics online, but I highly recommend week-long classroom training with plenty of practice. It’s a big, powerful program that’s complicated at first but so well-tailored to the industry that you’ll marvel at its capacity. Two of the largest and best-known training companies are Vale Training Solutions and Adjuster Pro. You can view a list of approved Adjuster Licensing Providers on the Texas Department of Insurance website (tdi.texas.gov). For a full listing of adjusting firms, large and small, see the directory at catadjuster.org.

Price of admission. Pre-licensing courses that satisfy the basic requirements for obtaining a resident or non-resident state license are available in the classroom or online. The online format can be boring, but the courses are inexpensive ($150 to $350) and convenient if you need to stretch the training out over time.

Classroom courses are less flexible but are more engaging and quicker to complete—you can finish in about three days. They also offer a broader perspective on the industry, but are considerably more expensive at $500 to $750.

License fees vary from state to state in the $50 to $500 range. Some states require an annual payment; others, biannual. Also figure on spending $100 to $150 every two years to complete approved continuing education classes to maintain your license.

Additionally, you can attend adjuster’s school online or in the classroom, which is worth considering if you have no background in insurance restoration, such as mitigating water damage, assessing roof damage, and understanding policies. These classes cost from $450 to $1,450, with the online version at the lower end.

Depending on the demand for adjusters, you may get the training you need from your employer. If you go to work for one of the four major independent adjusting firms— Worley Catastrophe Response, Pilot Catastrophe Services, Eberl Claims Service, and E. A. Renfroe & Co. — you may get the training you need for a small fee or gratis, or you may even get paid a day rate (about $600) to attend classes.

GETTING WORK

Insurance adjustment work is unpredictable. It comes and goes with the weather, and it fluctuates year to year. When a huge hurricane makes landfall or several storms hit back-to-back, it’s easy to get hired. Otherwise, you may get licensed and trained, then wait two years for your first deployment. But in my opinion, it’s still worth it: In a banner year, top-level adjusters can earn $200,000 or more.

A few major adjusting firms, such as the four mentioned above, and many small ones as well, keep a stable of qualified adjusters eligible and ready to deploy in the event of a catastrophe. Every year, tropical storms, hail storms, tornadoes, and floods provide deployment opportunities. Whether you sign up with one large company or several, the goal is to generate a steady stream of deployment requests that you can accept or decline at your discretion.

Certifications. Disasters occur everywhere, and your adjuster’s licenses allow you to adjust most claims, from hail to hurricanes. But some claims require specialized certification. I worked flood claims during Superstorm Sandy and found the niche rewarding. It is paperwork intensive because most flood insurance is underwritten by the Federal Emergency Management Agency (FEMA), but the pay is about a third more for the same dollar value. The claims process is also cut and dried because there’s only one policy to learn, unlike in the general insurance market, which has a dozen or more polices to deal with.

The other certification to consider is for earthquake claims in California. They don’t come often, but when large earthquakes do occur, there’s a lot of work to be done.

BUILDING INSPECTION

The only problem with CAT adjusting is that you have to wait for a storm, so most adjusters have a second job to fill in when the weather is calm. One option is municipal building inspection. The gig comes with benefits and a steady paycheck, but positions open rarely and fill quickly, and anyone used to self-employment will struggle with the bureaucratic environment. Also, you won’t be able to take off with three days’ notice whenever a storm hits the area.

The alternative I found was working as an independent commercial property inspector performing annual mortgage inspections for banks. Lenders were hammered during the recent recession, with bad loans on properties in extreme disrepair. In response, regulators ratcheted up due diligence requirements so that lenders must now inspect their collateral regularly to make sure it is being taken care of. A few large national companies get the bulk of the third-party inspection business and delegate the field work to a small army of qualified inspectors. By qualified, I mean a high-school diploma, considerable knowledge of building trades, and familiarity with commercial and large multifamily properties.

For certain types of inspections—principally of properties underwritten by Fannie Mae and Freddie Mac—commercial property inspectors must have certification. This comes with an eight-hour class and an exam. You also need decent computer skills because the reports (and there are many) require knowledge of programs such as Microsoft Excel and Word. You don’t need to be a computer whiz, but most jobs require computer literacy and a facility for learning new programs.

The basic routine involves setting appointments, requisitioning documents, (such as rent rolls and market reports), and meeting with property contacts to walk the site. You take photographs, ask questions, and make note of deferred maintenance. Looking at the rent roll, you may notice that the lease for an anchor tenant expires at month’s end, so you ask if the tenant has renewed. You also may notice that the parking lot needs resurfacing and the roof needs to be replaced—both items that represent important information for the lender. Back at the office (your kitchen table or a spare bedroom), you fill out the necessary reports.

Overall, I like the job because it allows me to do other things. I set my schedule and I can limit the number of assignments I do in a month. There’s plenty of work, so if you want more, it’s easy to be busy. Property inspection pays about a carpenter’s wage, but it serves me well, filling the gaps between other assignments.

—Previous to his exploration of insurance adjusting and property inspections, Fernando Ruiz was a developer and builder who specialized in affordable green housing for almost 30 years.