In previous articles (Business, May/15 and Jun/15), we differentiated between overhead costs and production costs (classified in accounting as “cost of goods sold” and often abbreviated COGS); thought about profit as just another expense; and then saw how looking at gross margin makes it easier to analyze the overall profitability of your jobs. In this article, we’ll explore the concept of margin. Only by understanding margin can you set accurate volume and markup goals.

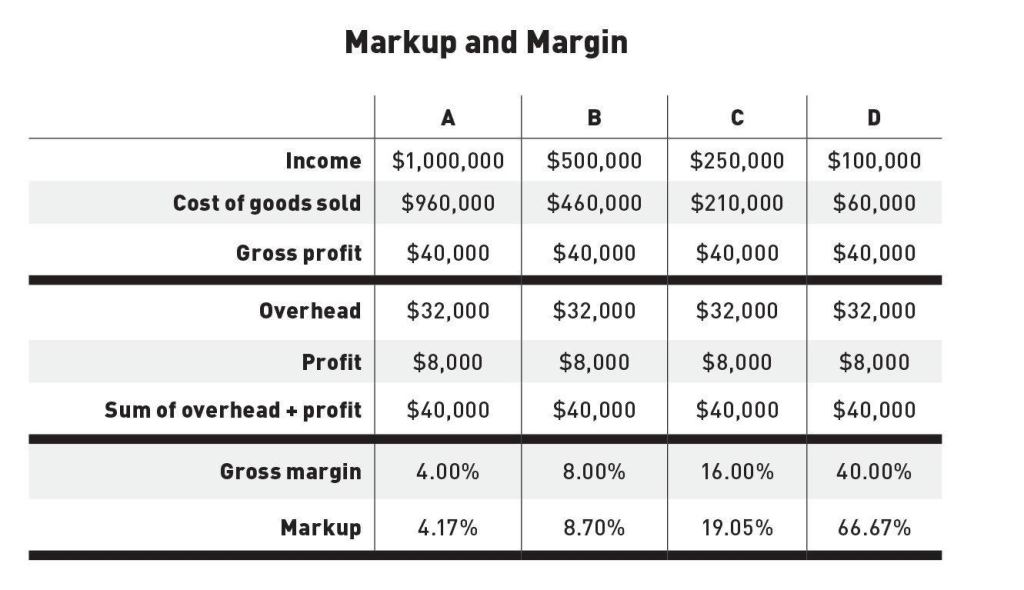

As an example, we estimated that our overhead costs for the coming year would be $32,000 and we identified $8,000 as a target net profit. That meant that we’d need $40,000 left over in gross profit when we finished producing work. That $40,000 could come from a variety of different sales volumes (A, B, C, and D in chart, below).

Gross Margin = Gross Profit ÷ Income

Using the formula for gross margin, let’s find it for each of the jobs. Although it’s a no-brainer that getting $40,000 from a $100,000 job is a more profitable scenario than getting $40,000 from a $1,000,000 job, let’s put some actual margin figures to it.

Doing so, we can see that the $1,000,000 job had a 4% gross margin while the $100,000 job had a 40% gross margin. Another way of looking at it is to say that for every $1 that came in on Job A, only 4 cents were left to cover overhead and provide for profit, while for every $1 that came in on Job D, 40 cents were left to cover overhead and provide for profit.

So, if you apply the gross-margin formula to your own financials, what do you get? Looking at the chart, it’s easy to see that the higher the gross margin you achieve, the lower your sales volume needs to be in order to provide the required dollars of gross profit.

Let’s say your gross margin turns out to be 28%, which just happens to be midway between Job C at 16% and Job D at 40%. Then if you needed $40,000 for overhead and target profit, you would need to sell and produce at the same degree of profitability somewhere between $100,000 and $250,000.

But isn’t there a more accurate way to pinpoint what you need to sell? And what about markup? Most contractors calculate their costs and then add a markup to it, whether they add the markup to the sale price when the job is sold at a fixed price, or they add the markup to actual costs if they sell T&M.

The key is the relationship between gross margin and markup. Although both use the gross-profit figure, gross margin relates gross profit to income while markup relates gross profit to costs.

Markup = Gross Profit ÷ COGS

As shown by the markup results in the chart, if you’re willing to add a 66.67% markup to your costs—and you’re able to sell work at that price—you can earn your $40,000 by selling only $100,000. On the other hand, if you only dare to mark up about 19%, you’ll need to sell $250,000 (two-and-a-half times as much!) in order to make that same $40,000 of gross profit.

What markup should you use? What volume can you sell and produce with your resources? It’s all in the numbers.

Melanie Hodgdon is owner of Business Systems Management. melaniehodgdon.com