It’s not uncommon for people to use the terms “markup” and “margin” interchangeably, as if they mean the same thing. And, as dollar amounts, they do; but as percentages, they’re very different—and that affects your business.

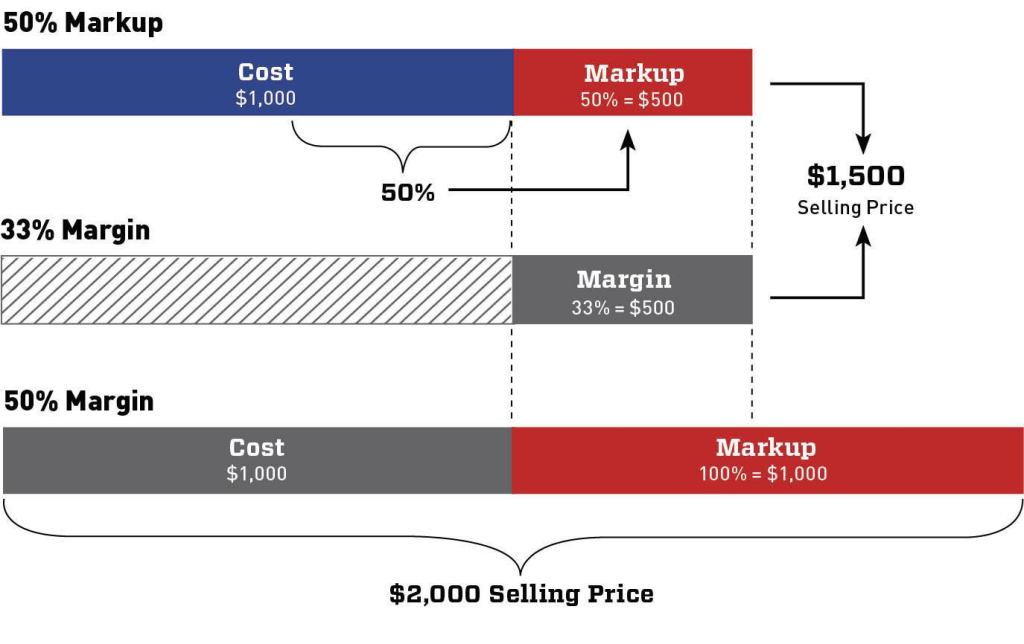

Imagine that you have estimated a project and have totaled all the costs including labor, materials, and subcontractors. That’s everything inside the blue box in the diagram, below. Upon your leaving the project, everything inside that blue box stays on the job.

If you plan to sell the job at a 50% markup, the correct method will add half the costs (50% x $1,000 = $500) to the estimated project costs ($1,000) in order for you to determine the total selling price ($1,500).

This constitutes a true 50% markup. Many people believe that’s also a 50% margin. Here’s why it’s not:

Margin is a ratio over the selling price:

Margin = Markup / Selling Price

Markup is a ratio over the cost:

Markup = Margin / Cost

Start with the total selling price.

In our example, markup, which is a percentage of costs, is 50%.

If we have $1,000 in direct costs, our markup is set at $500—thus equaling a total selling price of $1,500.

That’s paralleled on the margin side. But, whereas the $500 on the markup side is half of the cost, the $500 on the margin side is one-third of the total selling price. Therefore, a 50% markup is equivalent to a 33% margin.

How would you mark up your costs to get a 50% margin?

Starting once again with the total selling price ($1,500): If we expect to earn a 50% margin, we already know that costs will make up half the equation, and the other half is margin.

How much do we have to mark up these costs to get that 50% margin? If we take 100% of costs ($1,000) and add them on top of the total cost ($1,000) in order to determine a selling price ($2,000), that leaves a 50% margin. So, a 100% markup gives a 50% margin.

If you’d like to earn a 50% margin on your next project, you must double the direct cost amount to achieve it.