Periodically, it’s a good idea to check out your Accounts Receivable (A/R) report. If you use accounting software, this should be available as a standard report. Be aware that since the A/R report is based on invoices, and invoices are associated with accrual basis accounting, there is no such thing as a “cash basis” A/R report. At minimum, start paying attention to the report during the final quarter of the year. If you have late payers, you still have time to send out reminders and, hopefully, get paid before year end. Definitely conduct a review of your Accounts Receivable in January as part of preparing your tax documents for the prior year.

The following assumes your tax year is the calendar year. For fiscal year filters, substitute the last day of your fiscal year for December 31 and the first day of your fiscal year for January 1.

Understanding Your Accounts Receivable Aging Report

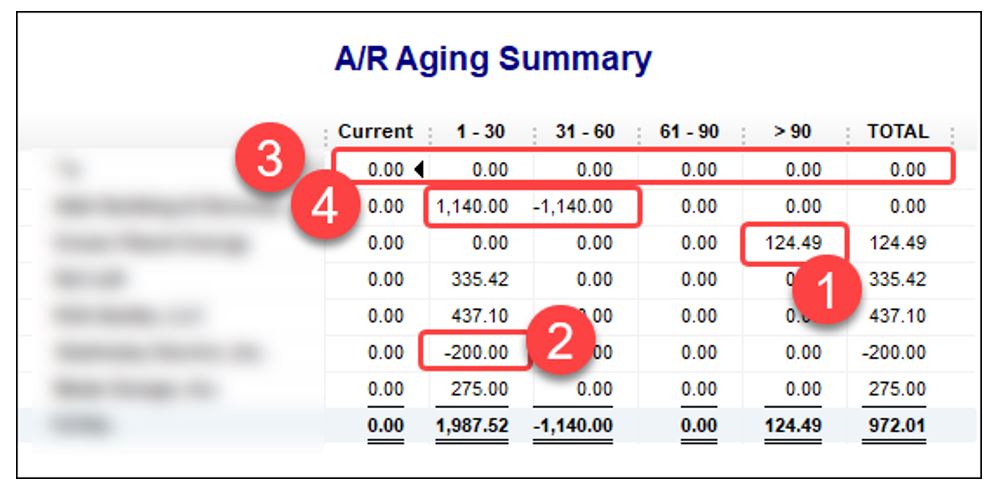

Typically, you will see a listing of all customers who have an outstanding balance, organized by “aging” or the number of days that have passed since the date of the invoice or, if you have set a grace period, the number of days from that. The report might look something like this:

#1 – Old receivables. The first thing to investigate is anything that is older than 90 days such as the $124.49 (#1). Is this still collectible? If not, how should you handle it?

#2 – Negative numbers. Are there any negative numbers? If so, are they real? “Real” usually means that a customer has overpaid an invoice. I see this often when (for some mysterious reason) customers avoid having to write a check that isn’t “round.” For example, if the invoice is for $5,109.58 they may write a check for $5,110.00, producing a “credit” of $.42 which will be displayed as a negative number (<$.42>) in the report. On the other hand, if they under-pay ($5,100.00), you may see an underpaid balance, which will be a positive number ($9.58) on the report. Perhaps you have a customer who simply likes to overpay in order to have a small credit balance. There is nothing wrong with this, as long as you understand what is creating the negative number.

#3 – The customer is listed on the report but has all $0 balances. This can happen if you have processed payment but somehow have failed to link the payment to the open invoice. In this case, your software may acknowledge the presence of the invoice (Debit to Accounts Receivable) and the payment (Credit to Accounts Receivable) so the balance appears to be $0, but unless the invoice and matching payment are linked, the invoice may remain “open” and the payment remain “unapplied.” If this occurs within the same reporting period in the report (such as with #3 on the report above), you will see $0 balances for this customer. To fix it and eliminate the paid-up customer from the A/R Aging Summary report, you will need to figure out how to apply the payment to the invoice(s) in question. The method will depend on your software. Note that in these cases, the unpaid invoice will be included in an Open Invoices report even though the customer has paid.

#4 – The customer shows both positive and negative balances, but overall owes $0. You may see a negative balance in one column and a matching positive balance in another column (#4). This usually happens if you create the invoice after receiving payment, or you give the invoice a date that’s after the payment. Let’s say the following happens:

You have completed an estimate for a new project and intend to generate scheduled payment invoices from the estimate. However, you haven’t yet gotten the estimate to your bookkeeper, so s/he hasn’t yet created an invoice. But the customer has paid $1,140, the amount of the first scheduled payment. Therefore, the bookkeeper must record the payment. Without an invoice, this will generate a credit for that customer.

Once the bookkeeper receives the estimate and is able to generate the invoice (for $1,140) to match the payment. If s/he dates the invoice using the date when the estimate was entered instead of a date before or on the day the payment was processed, you may see this result. The way this affects your reports is that while the customer’s balance may show $0, the $1,140 invoice will still be included in an Open Invoices report, leading you to believe the customer hasn’t paid. Also, this dating reversal (in which the date of the invoice is after the date of the payment) can mess up your Balance Sheet when run on a cash basis, resulting in a negative Accounts Receivable balance. Nine times out of ten, when I find negative A/R balances on a cash basis Balance Sheet, it’s due to errors in dating.

Handling Uncollectible Receivables

An uncollectible receivable refers to all or part of one or more invoices that the customer has not paid, and for which you have lost hope of collecting. This often happens at the end of the job, when the final payment is due (and is an excellent reason to keep final payment amounts very small!). Some unscrupulous customers apparently feel that they can afford to cheat you because the project is pretty much done and you no longer have substantial leverage over them. Or, alternatively, it could be a situation in which the customer is in a position where they are suddenly just unable to pay. This might stem from death or sudden and severe medical condition or some other unpredictable situation that you conclude is legitimate. Either way, you will have to determine whether it makes sense to pursue payment through legal means or a collection agency, or write it off.

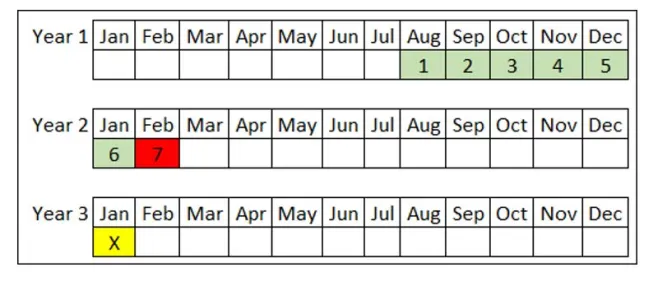

Example 1: Customer fails to pay final invoice and unpaid invoice is within the year for which taxes are now being prepared.

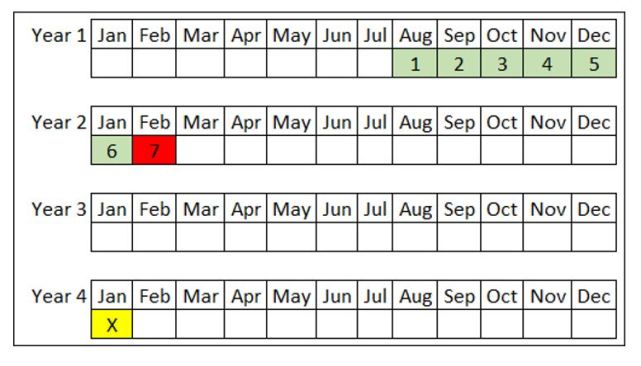

Let’s say that you sold a project with seven monthly scheduled payments. The job started in August of Year 1. Final payment was due in February of Year 2. The customer didn’t pay and you have concluded that they never will pay. You are now in January of Year 3, preparing to file taxes for Year 2.

If you file your taxes on an accrual basis, the February invoice will contribut to your reported income. Therefore, you are at risk of paying taxes on an inflated net income figure for Year 2. Also, your A/R figure on your Balance Sheet will be inflated by the amount of the unpaid invoice. Therefore, you need to remove the customer from your A/R report and simultaneously reduce net income. This can be done with a credit memo, and you have two choices. In either case, your taxable bottom line (net income) will be reduced by the amount of the unpaid invoice. For the sake of convenience and consistency, you may wish to date these credit memos 12/31.

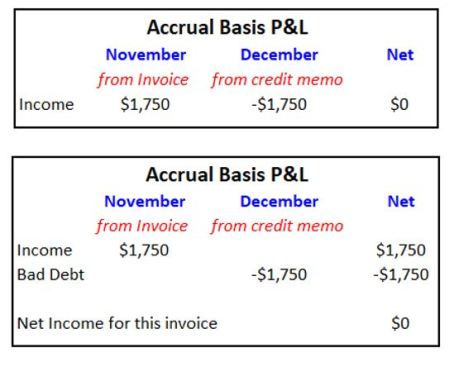

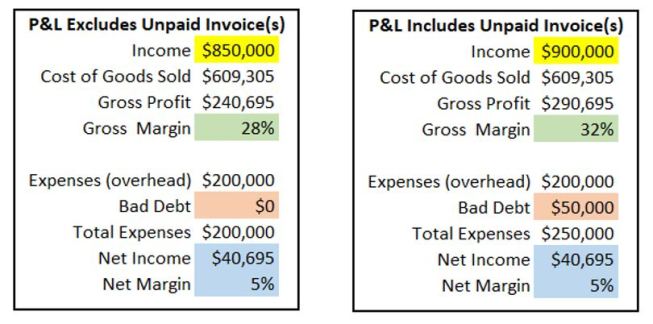

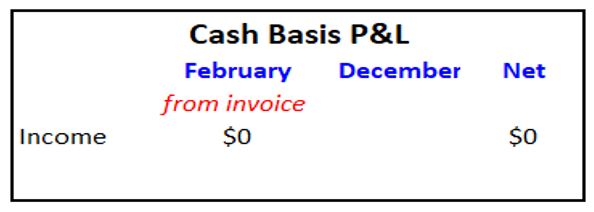

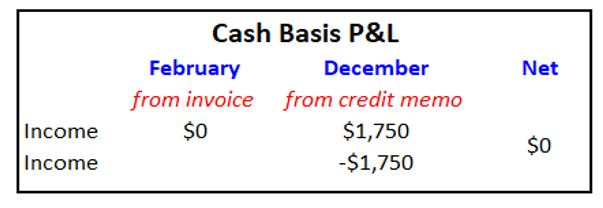

1. Generate a credit memo linked with an income account. This will reduce your reported income. This will also reduce your Gross Profit and Gross Margin figures.

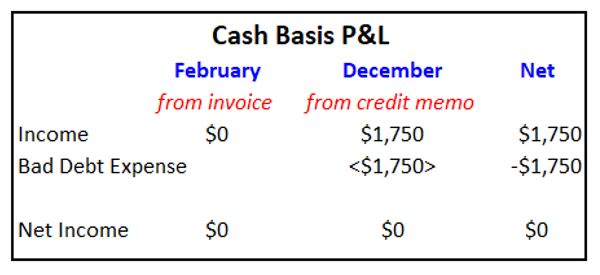

2. Generate a credit memo linked with a Bad Debt expense account. This will retain your reported income but offset it with an expense. This will retain your reported income, Gross Profit, and Gross Margin figures. However, if you are subject to any insurance or state tax calculations based on total income, you may be better off using the income offset method.

3. The results of each method on your P&L are shown below:

If you file your taxes on a cash basis, the unpaid February invoice will not contribute to your reported income. However, it will linger on your A/R and Open invoice reports and will continue to skew your accrual basis Balance Sheet. Therefore, it’s best to clean it up.

To do this, simply generate a credit memo. Year-end adjustments are typically dated 12/31 when the adjustment is for an invoice within the year for which the tax return is being prepared.

Since with cash basis accounting, the invoice contributes to income as soon as it’s paid, when you create the credit memo, the invoice will be considered paid, and will therefore be included as income.

The cleanest way to offset this is to link your credit memo with the same income account. The result will be that, as of the date of the credit memo, the invoice will simultaneously be paid and the amount of the invoice offset. The result will be to net the income associated with the invoice to $0.

Alternatively , as noted above, you may also choose to offset to Bad Debt in whichyou P&L would include an expense as shown at right.

What about unpaid invoices from closed tax years?

Let’s say you have an unpaid invoice dating from Year 2 and it’s now January of Year 4 and you’re about to file taxes for Year 3.

The process is actually exactly the same in terms of credit memos. However, since Year 2 has been closed and your tax return filed, it’s important to date any credit memos in Year 3. I typically date credit memos to clear invoices from closed years on January 1 of the year for which you are preparing taxes. In the above example, this translates to entering the credit memo to clear closed Year 2’s uncollectible invoice on January 1 of Year 3.

If you file your taxes on an accrual basis

Note that you paid taxes on an inflated net income in Year 2 since the unpaid invoice was included in the accrual basis P&L. Putting the offsetting credit in Year 3 will result in either a reduction in income or an addition to Bad Debt in Year 3 depending on whether you use an income account or the Bad Debt expense account in your credit memo. Either way, you will reducing your Net Income figure. Since you would like to maintain the accuracy of income in Year 3, it’s better to offset to Bad Debt to keep Year 3’s income figures correct. However, as with everything else tax-related, it’s best to consult your tax accountant on this issue.

If you file your taxes on a cash basis

The process is the same. Generate a credit memo on January 1 of Year 3. This will inflate income in Year 3 since this unpaid invoice was not included in income for Year 2. Therefore, it’s better to offset to income in the credit memo, in order to avoid skewing income figures for Year 3. Check with your tax accountant on this.

Wrap-up

It’s important to clean up Accounts Receivable, not simply to keep this account clean and your Balance Sheet accurate, but also because lingering open invoices can cause inaccuracies in your taxable bottom line. Try to avoid allowing uncollectible unpaid invoices to accumulate; do your best to review the A/R Aging report in the final quarter of the year and take necessary steps to remind customers of outstanding invoices. If you fail to get satisfaction and don’t want to take the legal steps required to fight it, then consider clearing these using credit memos linked either with income or Bad Debt. Your tax accountant is your best advisor in this department.

Rules of Thumb

- For uncollectible invoices within the taxable year, make the credit memo date be the last day of the tax year.

- For uncollectible invoices dated prior to the taxable year, make the credit memo date be the first day of the taxable year.

- Seek your tax accountant’s advice regarding whether to use a credit memo linked with income or Bad Debt.