A client recently sent me an e-mail asking an accounting question. But first, he provided a brief update: “I have been busy working and, I believe, making money?”

What stood out to me was that he added a question mark to what might otherwise have been a celebratory statement. And that reminded me of how easy it is to get lost in the work and lose sight of the profit—and to fool yourself into thinking things are going one way when they may not be. In these challenging times, as the pandemic forces the work to slow down, ramp up, and potentially slow down again, it’s even more important to pay attention. Here are two tips that can help you keep your finger on the pulse of your business.

Tip 1: Choose Accrual-Basis Reporting

Many people mistakenly view their financial reports on a cash basis, either because it makes more sense to them or because the reports look better or healthier to them. Don’t do it! Remember that even if you file your taxes on a cash basis, you can (and should) run your business on an accrual basis, because it gives you a far more accurate picture of what’s going on. Most accounting software will allow you to toggle between accrual basis (for managing) and cash basis (for tax preparation) reporting, so check out yours.

What’s the difference? There are two kinds of transactions:

“One-step” transactions. These include writing a check and using a debit card (where there is no accounting delay between writing the check and considering that cost to be debited from your checking account). On the income side of things, a one-step transaction would be creating a deposit to record money (such as payment from a customer) going into your account.

“Two-step” transactions. These include entering a bill, entering a credit card charge, and creating an invoice. Each of these transactions has a second step: You must pay the bill, pay your credit card account, and process payment from the customer before making the deposit.

In cash-basis accounting, you typically record only one-step transactions, which will be included on your cash-basis financial reports. Alternatively, you may record some two-step transactions, but these will not be included when you run your report.

Almost all companies generate invoices (a two-step transaction) from their accounting software, but many don’t enter bills and delay entering credit card charges until they actually get their statement (entering the total in bulk as a single entry when they’re ready to pay). Such companies are operating in a hybrid mode in that income is treated on an accrual basis and costs on a cash basis. If these companies run an accrual-basis profit and loss (P&L) statement, the invoices will be included (inflating income) but the costs will not be; and if they run a cash-basis P&L, any unpaid invoices will be excluded. Either way, they don’t get an accurate picture.

I’m going to focus on “above the line” transactions (income and cost of goods sold, or production costs), but the theory applies to overhead as well as balance sheet accounts.

Accrual-basis accounting and reporting. In accrual-basis accounting, you input data about all incurred expenditures and income (two-step transactions including bills, credit card purchases, and invoices). When a financial report is set to be viewed on an accrual basis, you will see all these costs and all the income in the report.

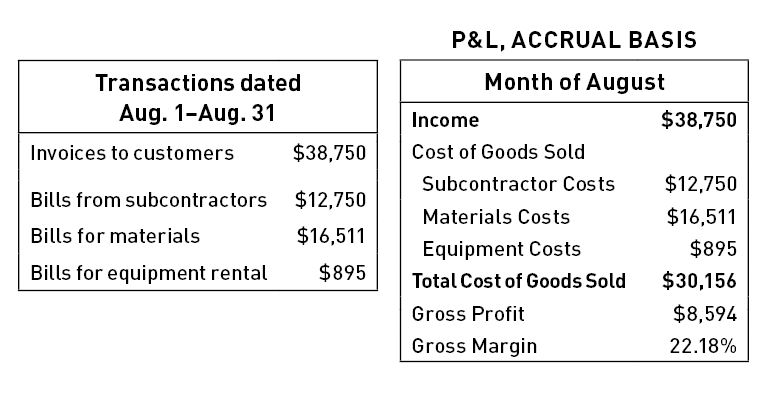

In the example above, let’s look at just the transactions that occurred within the month of August. If you are running your books on an accrual basis, you will enter all the invoices for customers and all the bills and credit card charges you may have received for subcontractor services, materials, and other direct costs (such as equipment rental) in August. Since you are entering these as they come in, on any day you will see the accrued costs on your P&L (as well as on your job cost reports)—whether or not they have been paid. The invoice gives you a more accurate picture of what is owed to you, and the bills and charges give you a more accurate picture of what you owe others within that time period. If you have invoiced more than you have incurred in costs, that’s good! In the example, invoices for $38,750 were sent out, and total costs for the same period were $30,156.

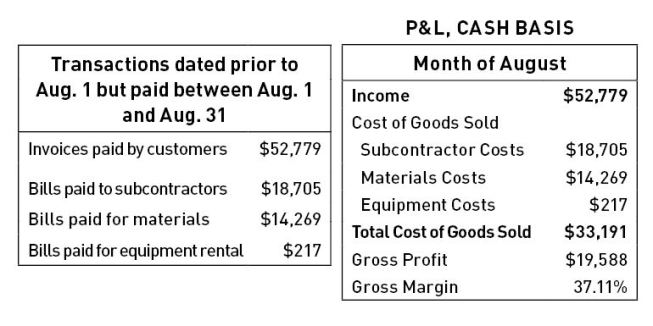

Cash-basis accounting and reporting. Now let’s look at cash-basis reporting for the same period (see table, below). On a cash-basis report, the only transactions included are cash inflows or outlays. In other words, if you received customer payments within the month of August, those dollars will be included. If a customer pays $25,000 on a $40,000 invoice, only $25,000 will be included on the report. If you paid bills in August (even if they were payments for charges from prior periods such as July or even June), those dollars will be included. As with invoices, if you paid $500 on a $1,200 bill, only the $500 will be included.

Notice that when you ran the P&L on an accrual basis, the gross profit for August was $8,594 and the achieved gross margin was 22.18%. But when you ran the P&L on a cash basis (below), the gross profit for August was a whopping $19,588, yielding an achieved gross margin of 37.11%. What happened and which can you believe? In the cash-basis P&L, income is reported as $52,779. This amount reflects payments on invoices created prior to August (assuming that none of the August invoices were paid in August). So these payments may have been for invoices from July, June, or even May if you had some late payers. You can’t determine when that income was requested since the report includes only the payment.

In cash-basis accounting, you typically record only one-step transactions. Note the reported margin here is much higher than on the accrual-basis P&L for the same business.

Now let’s look at the bills you paid. Presumably, in August you were paying for bills from July (and possibly June, if you have good-natured subs and suppliers). But how do you know whether you paid for everything? Remember, you aren’t seeing any unpaid bills on a cash-basis report. Or you may have made a partial payment. So that achieved gross margin of 37.11% may be wrong in part because you haven’t paid all your bills.

And that’s the biggest shortcoming of cash-basis reports: If you don’t have the cash to pay for something, it won’t show up. Since you only see a partial picture, you cannot draw accurate conclusions.

Earned vs. unearned income. Be aware that to be accurate, your reports should show earned income only. If you invoice for a large deposit (customer pre-payment), those dollars should not be considered income until the job starts and has generated a matching amount of costs. Unless you are adjusting for unearned income, including this income on either a cash or accrual P&L could be misleading and lead to overstating your gross profit and margin. More information on earned income is available in numerous articles on WIP (Work in Progress) adjustments.

Tip 2: Monitor Your Balance Sheet

Although most people are more comfortable and spend more time with their P&L than their balance sheet, the balance sheet can provide two quick ratios that will give you a sense of how well a company is doing overall.

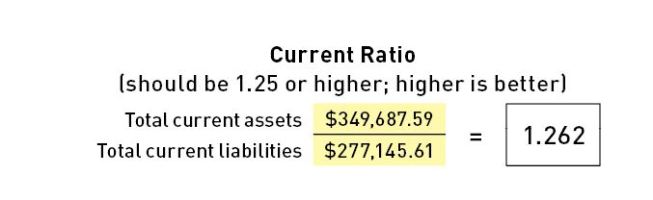

Current ratio. This ratio is derived from two numbers on your balance sheet. It is simply a measure of how well the company is able to cover short-term debt (liabilities) by using short-term assets.

On your balance sheet, short-term debt will be termed “other current liabilities.” (In accounting parlance, current refers to a term of 12 months or less.) Examples of short-term (current) debt include payroll tax liabilities, credit card debt, bills, and lines of credit.

Short-term (current) assets include cash (bank accounts, money markets), accounts receivable (will be turned into cash in less than 12 months), and inventory (can be sold and turned into cash in less than 12 months).

There’s nothing magical about this ratio. Simply look at your balance sheet; the total current assets and the total current liabilities will each be subtotaled. Divide the current asset subtotal by the current liability subtotal. Ideally, you should have $1.25 of current assets available to pay off each $1 of current liabilities. If your ratio is smaller than that, you are headed for a cash crunch and need to send some invoices out. You can create a simple calculator that will give you the ratio. Then every month, just input the subtotals and see how you’re doing.

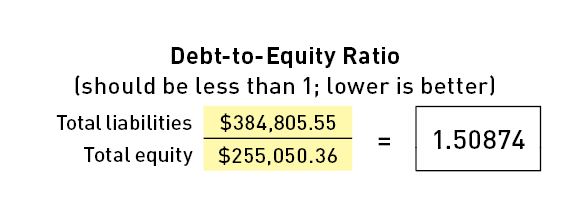

Debt-to-equity ratio. The purpose of this ratio is to show the degree to which your company is running on borrowed money. For example, let’s say that you took out a five-year loan for $120,000. That would certainly increase your cash (current assets). Your current ratio would probably look great since that five-year loan would be excluded from the other current liabilities subtotal. But that loan, which would be classified as a long-term (longer than 12 months) liability, should be included when considering your total debt, both current and long-term. That’s where this ratio comes in.

In an extreme oversimplification, equity can be considered the net worth of the company, assuming that all assets were liquidated in order to pay off all debt. Whatever is left over would be the company’s equity. So it’s helpful to understand how the amount of debt a company has compares with its equity. Hopefully, the total debt will be smaller than the company’s equity. The formula simply divides the company’s total liabilities by total equity.

Both of these figures are provided on the balance sheet. Again, create a simple spreadsheet to track these. You want debt to be smaller than equity, so the resulting number should be less than 1. In the example at right, this company’s debt is too high. The business is being sustained by borrowing. To improve the ratio, it will be necessary to reduce debt. To reduce debt, the company will need to increase income (not borrow more), which means revisiting pricing and production strategies

In Summary

Consider operating your business on an accrual basis—entering “two-step” transactions and monitoring financial reports on an accrual basis to get a truer picture of how what you’ve asked others to pay you (income from invoices) aligns with what others have asked you to pay them (bills and credit card charges) for any given period.

And track your short-term cash requirements and overall debt position using the current ratio and the debt-to-equity ratio.