To understand true profitability, it’s important to look at earned revenue instead of cash received. For example, if you require a 20% deposit at contract signing, and the job is sold at $100,000, the $20,000 check you receive shouldn’t be classified as earned income because you don’t have any costs to record against it.

There are several ways that you can end up with the desired result, which is to see only earned income on your profit and loss statement (P&L). Be aware that if the method used ends up with your having dollars of payments in a liability account, in terms of tax reporting, “cash is cash”; that is, if you file your taxes on a cash basis (check with your accountant on this), any dollars—earned or unearned—that you receive from customers must be reported as income. This is typically handled at year end by the tax preparer making a journal entry to temporarily classify these dollars as income on the last day of the tax year (December 31 for calendar year filers) and then reversing the entry on the first day of the following year (January 1 for calendar year filers). Doing so properly adds the received dollars to the P&L where they can be included as taxable income, but the reversal keeps things accurate for the following year.

METHOD 1: T&M INVOICING

In this method, the job is sold with the understanding that actual costs (burdened labor plus actual material and subcontractor costs) will be reported, an agreed-upon markup will be applied, and the customer will pay as the project progresses.

Pros: For contractors who have limited confidence in their estimating abilities, this can be a safe option.

It can also be useful when costs fluctuate wildly due to supply issues.

If payments are scheduled on a regular basis (say, every Tuesday following submission of the invoice on Monday, when all costs from the prior week have been assembled), the customer will be dealing with bite-sized outlays of money, and the weekly payment will be expected and hopefully planned for.

Cons: For the customer, there is no way to have a budgeted cost up front. If things crop up, too bad; they still have to pay.

Also, because invoices are generated as the job progresses, it’s impossible for the contractor to avoid shelling out money before it is reimbursed by the customer. This breaks the rule “Always pay for the project using the customer’s money.” For example, with a contract price, an invoice typically accompanies the signing of the contract. These bucks are designed to cover the startup costs (and accompanying overhead) that inevitably occur prior to what the customer would call “the start of the job.” With T&M invoicing, if state law permits, it’s best to request a “deposit” amount beforehand. This can be sold as a way to “hold your slot in our schedule” or anything else that sounds reasonable. These dollars can then be credited back to the customer on each invoice. The customer will end up paying the same amount, but the contractor won’t have to carry the job between signing the contract and creating that initial invoice that follows the first visible work on the project.

With T&M invoicing, the harsh fact of the markup amount will be in the customer’s face with every invoice. With contract pricing, the markup is embedded, as it is with virtually any other product we buy, from groceries to tools.

The contractor may feel compelled (by a desire for total transparency or in response to customer demand) to provide detailed information regarding time spent and actual costs incurred. This can be time-consuming, although with the proper preparation, reports can be memorized (a QuickBooks function) and easily run for each billing period. Under no circumstances should the contractor feel compelled to provide paper copies of everything.

T&M jobs have a tendency to go on and on. While there should be an agreed-upon scope of work, T&M projects seem to expand more easily than contract price jobs. One reason may be that with a contract price job, changes are recorded as change orders, which must be reviewed, agreed upon, and paid for by the customer. But with T&M jobs, the creation of change orders may not occur. Such changes may simply be viewed (sometimes by both parties) as an expansion of the existing job rather than as reason to commit to a separate agreement.

With fixed-price invoicing, your financials will show income based on the scheduled payments, not on earned income.

Because the customer will see actual costs (the level of detail provided will probably vary from company to company), the harsh fact of the markup amount will be in the customer’s face with every invoice. With contract pricing, the markup is embedded, as it is with virtually any other product we buy, from groceries to tools.

METHOD 2: PERCENTAGE-OF-COMPLETION INVOICING

On the surface, this may seem identical to T&M invoicing. However, the difference is that there is a set budget (the sale price) to which all parties have agreed. The scope of the job is understood, and the payment schedule may be time-based (invoice every week or two) or milestone-based (payments tied to milestones within the project). Just avoid creating milestones based on “completion of” since supply delays, inclement weather, crew injuries, or any number of delaying events can happen. Instead, tie to “start of” or “ready for” milestones that provide more flexibility.

Pros: Because, in theory, invoices are based on actual costs incurred to date, this method conforms to the Matching Principle, which states that revenue is earned at the same proportion as costs are incurred. For instance, let’s say the project budget is $100,000 and the project was sold at a 50% markup for $150,000. Then if you have spent $35,000 in costs (and remain on budget), the project is considered 35% complete, and you have earned 35% of the job sale price ($52,500).

Everybody knows ahead of time what the job will cost (excluding any change work).

Cons: Success is completely dependent upon accurate job costing. Errors such as not using fully burdened labor costs when calculating how much the company has spent on labor can cause huge problems if the cost of the job was estimated using burdened labor costs. (For more, see “Getting Labor Burden Right,” Apr/22.)

Cost overruns must be tracked carefully. If the budget for materials was $100,000, but somebody cut the Parallam 5 inches too short, the additional cost of replacing it (or even the time required to figure out and execute an acceptable workaround) can’t contribute to the original budget, because doing so would artificially decrease the percentage of completion. Deviations from the budget must be tracked carefully and a predictable method for reviewing, adjusting, and then calculating percentage of completion must be established (and followed).

A reasonable method of tracking and invoicing change work must be established, incorporated into the contract, and explained to the customer. Some contractors prefer to invoice 100% of the change order, treating it more or less like a small separate job. Others prefer to add the estimated cost of the change order(s) to the original contract and then calculate percentage of completion based on the revised budget. Whatever you do, just be sure it’s consistent.

METHOD 3: FIXED PRICE WITH PAYMENT SCHEDULE (NO WIP)

The job is estimated, markup is applied, and the price is set. The contractor sets up a schedule of payments that will provide positive cash flow. A method for handling change work is incorporated into the contract.

Pros: All parties agree to the price and the payment schedule before the job starts. The customer knows upfront what the payments will be and can make whatever preparations are required to cover the costs as they arrive.

The contractor can front-load to cover startup costs. Typically, the first invoice is “at signing,” and these funds will cover any costs incurred (including a portion of the job’s “fair share” of overhead). No, this payment should not be used to make up for the last job’s profit shortfall! While accurate job costing is always important (so you can spot discrepancies in expected costs and take action as the job progresses), invoicing is not dependent on it. Another nice feature is that customers typically review, approve, and then pay for change work as it occurs.

Cons: Your financials will show income based on the scheduled payments, not on earned income. So let’s say you have three jobs with contracts that were signed in April. They won’t start until May or June. You record the “at signing” payments as income, but none of the jobs have identifiable costs associated with them. So April’s income and gross profit look fantastic, but wrong.

Note: Some companies try to avoid this by simply recording a credit to accounts receivable instead of creating an income-based invoice. The problem with this is that your overall accounts receivable will be inaccurate, as they will contain a bunch of negative figures. This also affects your current ratio, which provides a measure of positive cash flow.

METHOD 4: FIXED PRICE WITH PAYMENT SCHEDULE (WITH WIP)

This method is exactly the same as Method 3, described above, but on a regular, periodic basis (typically monthly), a WIP (Work In Progress) calculation is made and financials are adjusted based on the results.

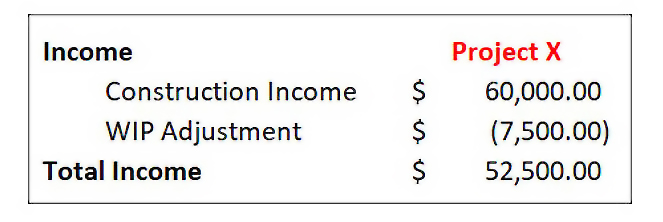

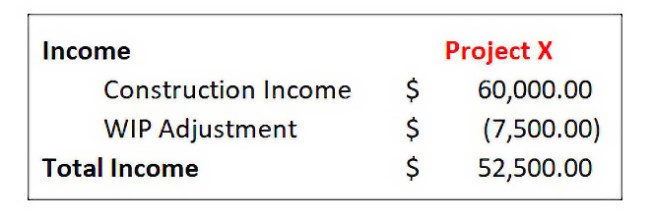

WIP is based on the Matching Principle (defined in Method 2, above). Revisiting the example used in Method 2, if the project budget is $100,000, and it was sold at a 50% markup for $150,000, then if you have spent $35,000 in costs (and remain on budget), the project is considered 35% complete, and you have earned 35% of the job sale price ($52,500). But if you have front-loaded your payment schedule (which is advisable in terms of cash flow), and you have actually invoiced $60,000 instead of the earned $52,500, then you have overstated your income for that period and must make a correction. This is called the WIP adjustment. In this example, if you look at the P&L for that job for that period, you will see $60,000 in income. But you should see only $52,500. Therefore, you will need to subtract $7,500 from that job’s income. It is best to create a new income account called WIP Adjustment and make the adjustment there. The result might look something like this:

WIP adjustment account on P&L Statement

Depending on where each project is (start, middle, end), how the payment schedule has been set up, and the nature and extent of cost deviations from budget, the WIP adjustments might be either positive or negative.

Pros: If the contractor is already doing fixed price with payment schedule, this method only requires him/her to add the WIP adjustment step to increase the accuracy of the financials.

Cons: Everything said in the methods above with regard to the importance of accurate job costing (especially cost overruns) applies here. If you don’t have a good handle on job costing, don’t even try this, as the results will create more problems. It’s one thing to have numbers that you know are accurate (the number of dollars invoiced in a given period) but misleading (they aren’t all earned), and it’s quite another to “improve” things by making adjustments that are wrong.

WIP Adjustments for multiple projects

Because WIP adjustments are reversed each month, income on financial reports will be correct only 12 days out of the year—one day each month when you’re making WIP adjustments.

Unless you keep a separate spreadsheet for tracking which customers are overbilled (you have invoiced more than what the job has earned) or under-billed (you haven’t invoiced enough to cover the costs that have been incurred, which really means you’re financing the customer’s job), it can be challenging to know where each customer stands.

There’s much more to calculating and tracking WIP, but this should give you the gist of the issues.

METHOD 5: THE “TWO-JOB” SYSTEM

This represents a blend of percentage-of-completion invoicing and contract price with payment schedule. Two “jobs” are created for each project. One job (the “payment” job) is used only for invoicing according to the payment schedule, and all payment dollars are considered liabilities. Invoices for the payment job affect accounts receivable but not income. This avoids including payment-schedule invoices as income on the P&L. The second job (the “project” job) is used for estimating, job costing, and invoicing percentage of completion. These invoices are “paid” immediately using a credit memo from the liability account, so the accounts-receivable balance on project jobs will always be $0.

Pros: No adjustment to income is needed because all income on the P&L is earned. It is generated via percentage-of-completion invoices on the project job(s).

Because a single liability account (typically called “customer deposits” or similar) is used, it is easy to generate a report that shows each customer’s balance in the liability account. Customers with positive balances have been invoiced for more dollars than the job has earned; customers with negative balances have been invoiced for fewer dollars than the job has earned.

On the balance sheet, the balance of the account reveals the net amount of unearned dollars the company has collected. A positive balance indicates that the company has collected dollars that have not been earned. This is great for cash flow, but it’s important to remember that your cash balance has been inflated by these dollars. In other words, if you have $100,000 in your checking account but $79,000 in your customer-deposit liability account, you really have only $21,000 in “available” cash to spend.

This account can also be easily reconciled at the end of each job to confirm that the amount invoiced via the payment job matches the amount of income reported for the project job. For tax purposes, at year-end, a single adjusting entry can be made to zero out the balance in the customer-deposit liability account with an offset to income. As with any such tax-related adjustment, the entry would be reversed on the first day of the following year.

Cons: Unlike WIP adjustments, the two-job system typically uses periodic costs rather than cumulative costs. In other words, costs for a given period (usually a month) are included in a report that forms the basis of the percentage-of-completion calculation. This requires careful dating of bills, paychecks, etc.

As with WIP, it’s critical to take into account change orders and projected deviations from estimated costs. Otherwise, your percentage-of-completion invoices will be inaccurate.

Because income-related invoices for the project job are always paid using a credit memo to apply the customer’s dollars from scheduled payments to the project job, it’s all too easy to over-credit. In other words, it would be possible to “pay off” the income-recognizing final invoice for this job based on the Matching Principle and using liability dollars in the customer deposit account.