First, what is profit? Let’s say when you look at your profit and loss statement, it shows a net profit of $50,000. The logical assumption is that you have at least $50,000 sitting in your various bank accounts ready to use, right? Well, as usual in accounting, things aren’t quite that simple. In addition to the profit and loss statement, there are two other primary financial reports—the balance sheet and the statement of cash flows—and each has a different purpose and tells a different part of the story. Let’s look at a simplified example to see how the reports all contribute to the story of how much money you have.

Profit and Loss

A profit and loss statement (P&L) records the coming in and going out of money for a specific time period (say January through December of a given year) as a result of conducting a business. The incoming money is income (which could include incoming dollars from the sale of a project, accumulated interest from savings accounts, and so forth). The outgoing money is divided between the costs associated with the production of projects (cost of goods sold) and the necessary costs to maintain the company (overhead). The P&L will not include loan payments or capital investments (such as the purchase of equipment or a vehicle). So if you put $5,000 down on a new van, don’t expect to see that on your P&L.

A P&L can be run on either an accrual basis or a cash basis. When viewing one on an accrual basis, you will see everything you’ve invoiced to customers, whether or not you’ve received payment for the invoices; similarly, you’ll see all the bills that have been entered, whether or not you’ve paid them yet. If, for example, you invoiced a customer $15,000 in December of last year and she paid you in January of this year, the $15,000 would appear on last year’s P&L.

Viewing the P&L on a cash basis means that you will see only those invoices and bills that have been paid. You’ll see payments made in the current period for bills entered in both current and prior periods, and you’ll see customer payments in the current period for invoices entered in the current and prior periods. So the $15,000 in the example above would appear on a P&L for this year.

While a cash-basis P&L may be useful in terms of seeing net cash figures for each reporting period, it’s not an effective management tool. After all, if you decide not to pay your bills in February and then view a P&L for February on a cash basis, you will appear to have loads of cash and low costs when in fact you may have $30,000 in bills that you’re just not seeing. On the other hand, an accrual-basis P&L lets you compare what you’ve invoiced with the costs you’ve incurred— instead of simply showing when payments came in or went out—so that you can judge whether or not you’re invoicing a sufficient amount to cover your costs each month.

Balance Sheet

A balance sheet records a company’s assets, liabilities, and equities.

- Assets are things that the company owns, such as cash in the bank, accounts receivable (which will be converted into cash as soon as customers pay), inventory (if any), and fixed assets (stuff you can touch) like vehicles, large tools and equipment (more than $2,500 in value), office furnishings, and the like.

- Liabilities are things that the company owes, such as accounts payable and credit-card debt (which will reduce your cash as soon as you pay your vendor bills and credit cards), payroll taxes, and loans.

- Equity is what’s left after you subtract liabilities from assets. This is also where draws and distributions (monies withdrawn by owners, partners, or officers from the company for personal use) are recorded.

Unlike the P&L, the balance sheet includes all of the company’s activity through a certain date. So if the company started in January 2010 and you run a balance sheet as of December 31, 2018, the report will reflect activity for eight years.

Like the P&L, the balance sheet can be run on a cash or accrual basis but is most revealing to view on an accrual basis. For example, you can check to see if your current assets (like cash and receivables) are sufficient to cover your current debt (payables, payroll taxes, and so on). This can help you see when you’re getting into a cash crunch.

Statement of Cash Flow

The statement of cash flow is a report that “reconciles” the number of dollars you have in cash at the end of the reporting period. It includes a starting cash balance, then records the net income (from the P&L), investing activity such as the purchase of a new jobsite trailer (from the balance sheet) and the paying down of loans (from the balance sheet). This is the report that will show you where your cash went. The simplified sample reports shown above reflect all the typical kinds of entries you’re likely to see.

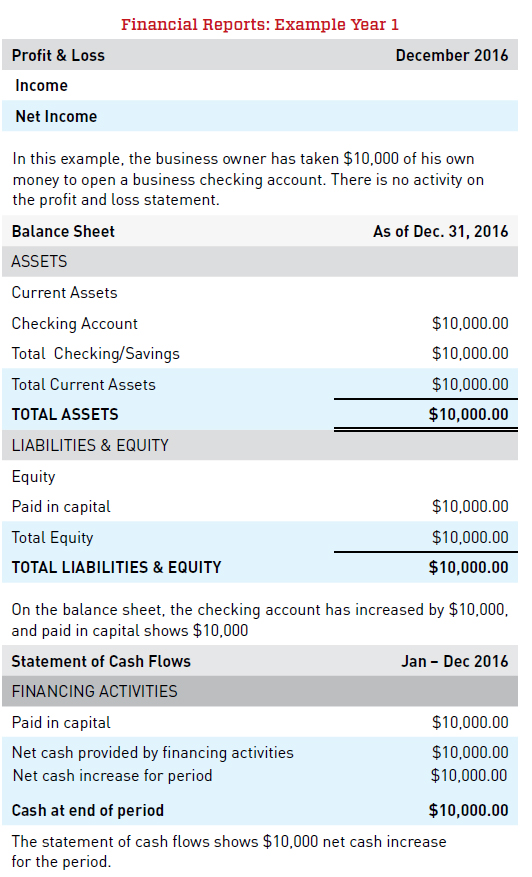

A Simple Example

Let’s assume that you are the owner of a startup company and that you took $10,000 of your own funds and opened a business checking account on December 31, 2016. That was the only business activity for 2016, so at the end of the year, the three reports would have looked like the examples above.

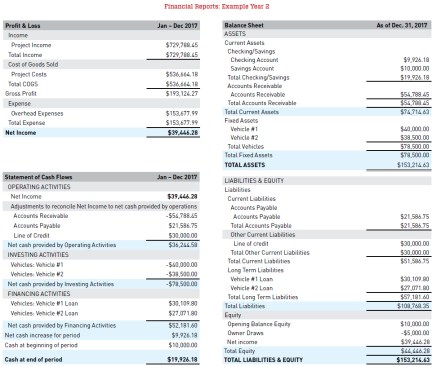

One year after. Now let’s check back exactly a year later. In 2017, the company was actively engaged in business. The relevant facts about this company’s activity are shown in the three financial reports on the facing page; here is a summary provided by these statements of the business in 2017.

- Net income. The company “made” $39,446.28 according to an accrual-basis P&L.

- Adjustments to reconcile net income. But wait! Some of your customers haven’t paid yet, so you’re missing $54,788.45 in cash. That deducts from your cash.

- Unpaid bills. Wait again! You haven’t paid some of your suppliers yet, so you still have $21,586.75 of cash in unpaid bills. That adds to your cash.

- Line of credit. But wait yet again! You took a $30,000 draw on your line of credit and that adds to your cash as well.

- Investing activities. Even though you only put down a small bit of cash on each of the vehicles, they are now considered company assets and this report shows the value of the vehicles ($40,000 and $38,500) subtracted as if you had paid entirely in cash. The financing loans appear in a different part of the report.

- Financing activities. Because you financed both vehicles, you should see the loan amounts adding to your cash since you didn’t actually have to shell out the full purchase price. But because you made a bunch of payments on the loans, the current balance for Vehicle #1 Loan has been reduced from $37,500 to $30,109.80 and the current balance for Vehicle #2 Loan has been reduced from $35,500 to $27,071.80. Finally, the owner withdrew $5,000 from the company for personal use. In accounting terms, that money is also included under “Financing Activities.”

- Cash at end of period. When you start with net income and then add and subtract the adjustments, investing, and financing activities, you end up with a cash increase for the period of $9,926.18. Because this company started with $10,000 in cash, the cash balance at the end of the year should be $19,926.18. Checking the balance sheet, we see the total cash is indeed $19,926.18.

Where’s the Money?

So the answer to the question, “Where’s my cash?” is more complex than it appears on the surface. While most people are comfortable using and interpreting the P&L, it doesn’t show the full story—it doesn’t include investments made (such as purchasing vehicles and equipment), payments on loans, and withdrawals from the company for personal use. Next time you look at your bottom line and wonder where the cash is, check out the statement of cash flows report; it will tell you exactly where your money went!