Many contractors struggle with cash-flow problems. They pay suppliers late, they dip into lines of credit too much, they miss tax deadlines — they even miss payroll. Even contractors who are profitable on paper often don’t have money on hand when it’s time to pay the bills. You can go out of business, in spite of being profitable, if you run short of cash at the wrong time. It doesn’t have to be that way.

The keys to keeping income ahead of expenses are really pretty simple. I’ve seen them work in my own years in the remodeling industry, and since I’ve been advising other contractors, I’ve seen them turn many businesses around. You just have to make up your mind to apply those key points consistently.

First of all, to stay profitable, you’ve got to know your costs and charge the correct markup on every job. Second, in order to be ready for emergencies, you’ve got to maintain an operating capital reserve account big enough to handle unexpected expenses, or to cover your overhead when your income falls short for any reason. And third, to stay ahead of all your job costs and your routine bills, you’ve got to structure your contracts so that the payment schedule works in your favor. In this article, I’ll focus mainly on the third point: structuring the payment schedule in your contracts.

I often talk to contractors who know their costs and charge the right markup, but keep coming up short of cash — and they can’t figure out why. In almost every case, I get them to restructure their contracts to provide for many small customer payments over the course of a job instead of just two or three large payments. Also, I show them how to schedule those payments at the start of a phase instead of the completion if possible. That way, they’re working out of their customer’s pocket instead of their own. Without exception, within four to six weeks of when the new payment schedules kick in, their cash-flow problems have gone away.

It’s a wise and prudent contractor who works out of his customer’s pocket. Take a look at the following two graphs. If you chart the expenses and income on your own jobs this way, will your jobs look like the first example — cash negative for most of the job? If so, you have taken on the burden of financing every job with your own money. You are not only in the business of construction but also in the business of being a lender to your customers.

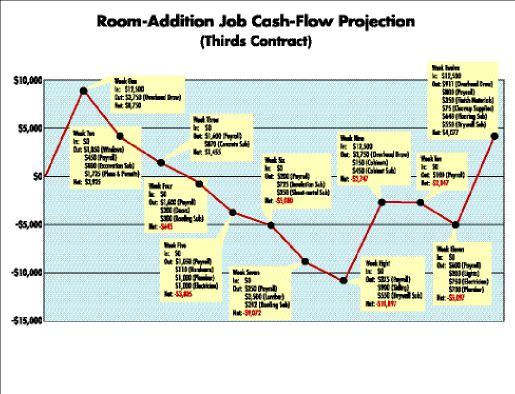

This graph shows the cash status of Joe’s room-addition job using his old contract. His cash on hand goes below zero during the fourth week of the job, and he does not go cash positive again until he receives his final payment at the end of the job. Any unexpected expense between the fourth and twelfth weeks could make his life very difficult.

Changing his schedule of customer payments improves Joe’s cash-flow position drastically. Outlays are the same, but frequent small inflows keep him cash positive throughout the job.

That means you have the risks of both industries. On top of the risks of being in construction — weather, job-site injuries, construction defect liability, labor shortages, employees quitting or getting sick or being late, price variations, bidding mistakes, and all the rest — you have assumed the risks of the lending business, which are basically default and late payment.

So ask yourself this: As a contractor who also finances construction, are you applying the safety measures professional lenders apply — such as credit checks, credit insurance, reserve requirements, and so on? And do you charge interest on the money you advance, like any bank or credit card company does? If the answer to both questions is no, what you’re putting on the line is your own rear end, and what you’re getting in return is nothing.

Where Did My Money Go?

There are many things that can happen quickly to leave you cash poor. Cash is always streaming out of your business. Payday comes every Friday; rent, utility bills, and truck payments come due every month; tax deposits come due at least quarterly. Job costs such as materials and subcontractors are often front loaded; at best, you’ll have a month before you’re billed. To stay on top of those routine outlays, you need money coming into your business every couple of weeks.

Then there are the surprises. Your equipment breaks down, a customer’s check bounces, the tax department audits you and finds an underpayment, or your insurance company audits your comp account and says you owe more money. No matter how good your plans are, that kind of unexpected expense can leave you scrambling for cash. That’s when you’d be glad to have a strong operating capital reserve account (see “Maintaining a Capital Reserve Account,” below).

Maintaining a Capital Reserve Account |

Every business should have an operating capital reserve account — money set aside to take care of emergencies or to tide the business over when income drops below expectations. Whether it’s a bounced check, an unexpected illness, or just a decline in sales, an adequate cash reserve can keep you operating until things improve. Your particular needs may vary, but in general I recommend that the fund should be able to cover five to seven months of overhead expenses for your business. You can’t create a fund like this overnight. I advise my clients to take a fixed percentage of every check that comes in and add it to their operating capital reserve account until the fund has reached its target level. Setting aside 1% to 4% is easy to stick with and won’t hinder your cash flow. If you have to draw on the fund, you should replenish it as quickly as you can. |

Surprise costs on top of routine expenses can make life difficult. Without naming any real people, let me give you an example based on the kind of thing I see all the time. I’ll call this business Joe’s Construction. If Joe’s experience reminds you of your own business, you might find my recommendations helpful.

Joe is a good mechanic and puts his jobs together well. He estimates accurately, and he knows his markup: He multiplies his estimated job costs by 1.48 whenever he prices a job. He can expect to make a fair profit on every project.

Joe is selling a room addition with a half bath. In his contract, he describes the job in detail and concludes with the following payment schedule:

Total price for labor, materials, and other costs | $37,500 |

One third down | $12,500 |

One third at completion of two thirds of job | $12,500 |

Balance due when job is complete | $12,500 |

I don’t know why so many contractors use this “thirds” formula in their contracts, but I see it all the time. This room addition will take 10 to 12 weeks to build. Joe figures that the $12,500 down payment will easily carry him until the progress payment in six or seven weeks. The customer signs the agreement, and he starts the job.

Joe’s overhead is just over 30%, so he takes 30% ($3,750) from the first customer check to pay overhead bills. He’s always careful not to draw on his profit until the job is done and all the bills have been paid.

He spends $1,250 getting the plans drawn and another $475 on the permits. He orders special windows that require an up-front payment of $1,850. He pays the excavator $800 as soon as he is done, then the concrete guy wants half his money up front and the rest — a total of $435 — within three working days of job approval by the inspector. Payroll comes to $450 for the second week and $1,600 for the third.

By the third week of the job, Joe has just $1,455 left of the original down payment, and it will be a good five weeks before he gets another payment. That won’t begin to cover his payroll, and there will be more suppliers and subcontractors asking for money before then. But he isn’t worried, because he has other jobs in progress. He assumes that he can move money back and forth as needed to be sure he is covered.

Joe thinks he has things well in hand. But two weeks after the room-addition job starts, the transmission breaks down in his main work truck. Boom: $1,850 to get it fixed. Then his insurance agent calls and says that his general liability insurance premiums are going up, and payment is due before the end of the month. Joe had also purchased several pieces of equipment from one of the big box stores, and his first payment is now due.

Soon Joe has more bills to pay than he has money. The payment schedules that he has written into his contracts mean that his company receives only two or possibly three checks during a typical month. He now finds himself robbing Peter to pay Paul. He’ll need to take money out of pocket to keep going until the next payment comes in. He may even be tempted to take the down payment for his next job and apply it to the current job’s costs.

A Solution

Joe wouldn’t be seeing this situation if he scheduled his payments better. The one-third down payment is fine, but progress payments need to be scheduled earlier and more often.

Base your down payment on the size of the job and make sure you get enough cash in that payment to get started. I recommend charging between 10% and 40% down on every job. Generally, the larger the job, the smaller the down payment percentage. That’s natural when you think about it; $16,000, or 40%, down on a $40,000 job is something the customer should be able to handle, but if the contract for a $400,000 house called for $160,000 down, it would be a different story.

Once your down payment is established, you should set a schedule of payments that provides you the cash you need for each stage of the job. The best way to define that schedule is to collect a payment at the start of a phase of the work. For example, you should schedule a payment at the start of framing, not the completion of the concrete installation.

Using the start of work to define the payment schedule reduces the potential for argument. A customer who’s looking for a reason to hold back money may point to some minor detail as evidence that the work is not complete. But the start is a point that’s less subject to argument. This way, Joe won’t have to deal with a customer holding up a big progress payment while his crew touches up paint or screws on outlet covers.

If Joe applied this method, the payment schedule for his room-addition job would look like this:

Contract price | $37,593 |

Down payment | $12,593 |

Start of framing | $5,000 |

Start of window installation | $5,000 |

Start of electrical rough-in | $5,000 |

Start of finish carpentry | $5,000 |

Start of painting | $4,250 |

Final, due on day of substantial completion | $750 |

This payment schedule keeps the money coming in regularly, about every two weeks, helping to match cash inflow with cash outflow. Other kinds of jobs can be structured the same way. A gut-job kitchen remodel might look like this:

Contract price | $46,985 |

Down payment | $15,985 |

Start of rough plumbing | $6,000 |

Start of sheet metal | $6,000 |

Start of cabinet installation | $6,000 |

Start of finish plumbing | $6,000 |

Start of painting | $5,750 |

Final, due on day of substantial completion | $1,250 |

A deck might look something like this:

Contract price | $8,897 |

Down payment | $3,897 |

Start of structural framing | $2,250 |

Start of decking installation | $2,250 |

Final, due on day of substantial completion | $500 |

In each of these examples, you’ll notice that the final payment is a small amount. I recommend that the final payment for a remodeling project should not exceed $1,000 or 2% of the total, whichever is less. Specialty work is about the same. New home construction involves larger amounts of money and final payments may be larger, but the final payment in the contract should still be no more than 2% of the total price.

A modest final payment takes away any lever that customers may think they have to get the contractor to do additional work for no pay. And it sharply reduces the dollar incentive for customers to refuse to make the final payment in hopes that the contractor will just walk away from the money that he is rightfully owed. I serve as an arbitrator in a lot of construction disputes, and I’ve often seen that happen.

State Legal Restrictions

It’s a cardinal rule in any business that you should set your own prices: You don’t let anyone tell you how much to charge for your work or what your payment schedule should be. Some state laws include limitations on the amounts of down payments. There are various ways to comply with those laws and still have the cash you need to run a healthy business. My clients have coped with such laws by changing the language in their contracts.

One way to arrange to have cash on hand when you start work is to write a separate design agreement, or just an Evaluation, Estimating, and Quotation Contract. That agreement ensures that you will be paid to do the estimate, prepare the plans, write the specifications, and get the entire job ready to be submitted for the permit process. You can collect for that preliminary phase before you start the physical work on the job. Your customer is paying you for services rendered, you are being paid for work done, and that’s fair to everyone involved.

Say you’re looking at a $100,000 job and you figure you need to have $25,000 on hand when the work starts. You simply write a contract for $15,000 that covers the plans, the permits, writing the contract, and working up a detailed estimate and materials takeoff, payment due upon completion of those items. So as soon as that’s all done, you collect $15,000. That leaves $85,000 to go for on-site work; you get an $8,500 down payment out of that, and then you get a progress payment of $10,000 at the start of the foundation work. By the time your excavator has to be paid, you will have collected $33,500 of the full $100,000. As long as the rest of your progress payments are well timed, you’ll be in a good position to stay abreast of your costs for the remainder of the job.

Builders of new homes may be working with a lender who wants to inspect the items completed before releasing a progress payment. In that case, contractors have to schedule their progress payments at the completion of some phase of the project instead of at the start. That’s okay — just arrange the payment schedule in a way that meets your company’s need for timely cash inflows. Here’s an example:

Contract price | $137,593 |

Down payment | $13,593 |

Completion of concrete (instead of start of framing) | $12,125 |

Completion of window installation (instead of start of siding install) | $12,125 |

And so forth |

|

Final, due on day of substantial completion. | $2,750 |

This is just a matter of wording. The point is that you get the payment when you want it, not when the homeowners want to give it to you. And you want it so that you don’t have to go three, four, or five weeks between payments. Even though your job costs, your price, and your net profit are the same in the end, you avoid those long dry periods that can kill a business.

Breaking your payment schedule up into smaller parts will level out your cash flow and give you the ability to pay your bills when you should (every two weeks). You will also be able to take discounts for prompt payment with your suppliers, and you’ll always pay your employees on time. Last but not least, this payment schedule will help you maintain the 8% net profit level that is needed for the long-term steady growth of your business.

Michael Stone has more than three decades of experience in the building and remodeling industry and currently serves as a business coach for construction companies throughout the U.S. He is the author of Markup and Profit: A Contractor’s Guide (Craftsman Book Co., 800/829-8123) and moderates the Markup and Profit forum at jlconline.com.