Last month, I introduced the concept of working “by the numbers” — meaning that you plan your annual income requirements in advance, then attempt to translate your goal into project sales, starts, and completions. You always work toward the plan, making adjustments along the way as necessary. I also made some distinctions between the kind of accounting your CPA does and “management” accounting and reporting — using the numbers your business generates to make successful operating decisions.

This process is the beginning of “strategic budgeting.” By establishing your goals for the year early on, you are building a road map for success — not just for the coming year, but for as long as you operate your business. Consistent strategic budgeting can make the difference between being able to retire with money in the bank and limping into your golden years. And it’s never too late to start. Whether you have four years in front of you or 40, this process will improve both your business and your lifestyle.

This month, I’ll look at “break-even volume,” which is the bare-minimum volume of work that you need to complete (and get paid for) in order to keep your doors open. This may be a little boring, but bear with me.

Required Information

To calculate break-even volume, you need several key pieces of information, including the following:

The basic financial/budgeting model for your business. By this I mean the percentage of revenue budgeted for the various expense categories (such as your office overhead or project supervision). As we saw last month, these numbers are somewhat different for builders and remodelers.

Projected average selling price for projects in the various categories you build or remodel.

Projected average gross-profit percentage for the budget period (see last month’s column).

Projected fixed operating expenses for the budget period.

Projected average variable operating expenses for the budget period.

Projected average construction indirect expenses for the budget period.

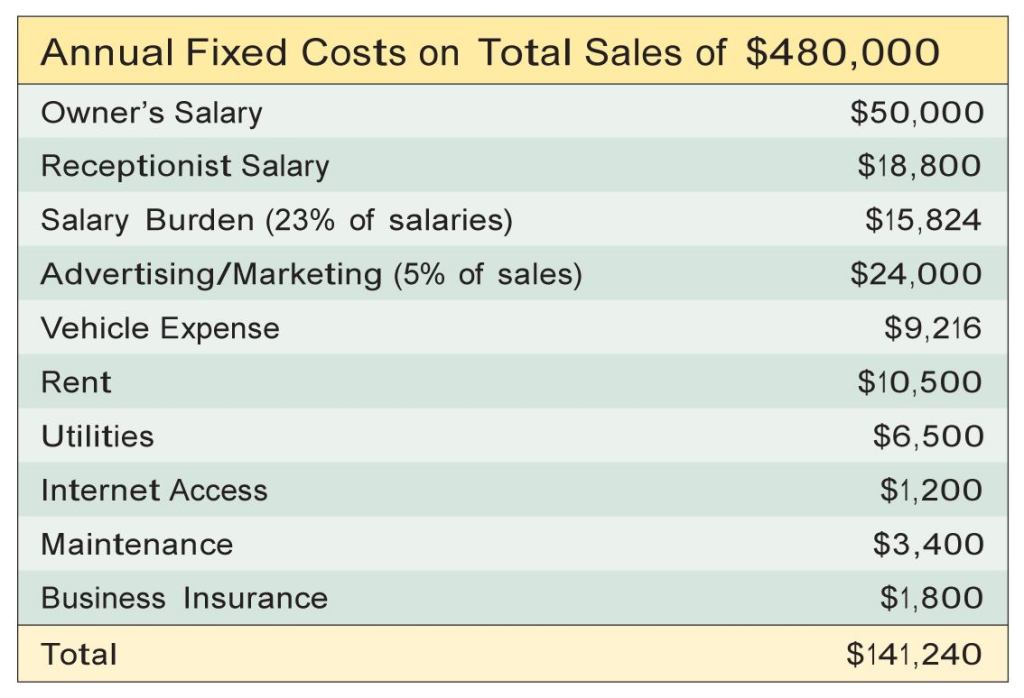

Fixed Expenses

Fixed expenses occur whether or not you build anything — they are the cost of keeping your doors open, and meeting them is what break-even is all about. They include:

All salaries and hourly wages not directly related to job costs, such as those paid your receptionist, estimator, and CAD operator, as well as your own salary.

The labor burden on those positions — Social Security, unemployment insurance, and any benefits you pay as an employer.

Vehicle expenses. This is a tricky category. Include only vehicle expenses that are truly fixed for the budget period — items that don’t change month to month and don’t go away if you subtract people or build fewer jobs, such as lease and loan payments, regular maintenance, and the like. (Treat vehicle allowances and mileage reimbursements for salespeople and superintendents separately.)

Advertising and marketing expenses. Even if you don’t actually spend a dime on advertising, budget something. (Use 5 percent of your sales if you’re a remodeler and 2 percent if you’re a home builder.)

Business insurance, including insurance on your building and its contents, general liability, and — if you’re a design-builder — errors and omissions insurance. (Be careful here, as some types of insurance are calculated against your gross sales or gross wages for the period.)

Office expenses: phone, utilities (for the office, not your job sites), facility maintenance (snowplowing, cleaning), repairs, and so forth.