Regularly comparing job estimates with actual expenses seems like a no-brainer. But after years of training hundreds of contractors about finances, I suspect that many contracting businesses don’t make this type of comparison, at least not in a systematic way, and I’m certain that means they’re losing money.

How do I know this? The answer is that I’ve run my own custom building and remodeling business both ways — with and without checking estimates against actual costs — and have seen the difference. Once I developed a system for reviewing these numbers and got disciplined about following it, my company became significantly more profitable.

How It Works

Every Friday afternoon, I set aside 10 minutes to review project numbers. I began doing this in 1990, soon after I started using a computerized accounting and project management system. The review alerts me to cost deviations on individual jobs so I can actively manage those deviations before they overrun the project. In addition, the lessons I learn help me to estimate more accurately in the future.

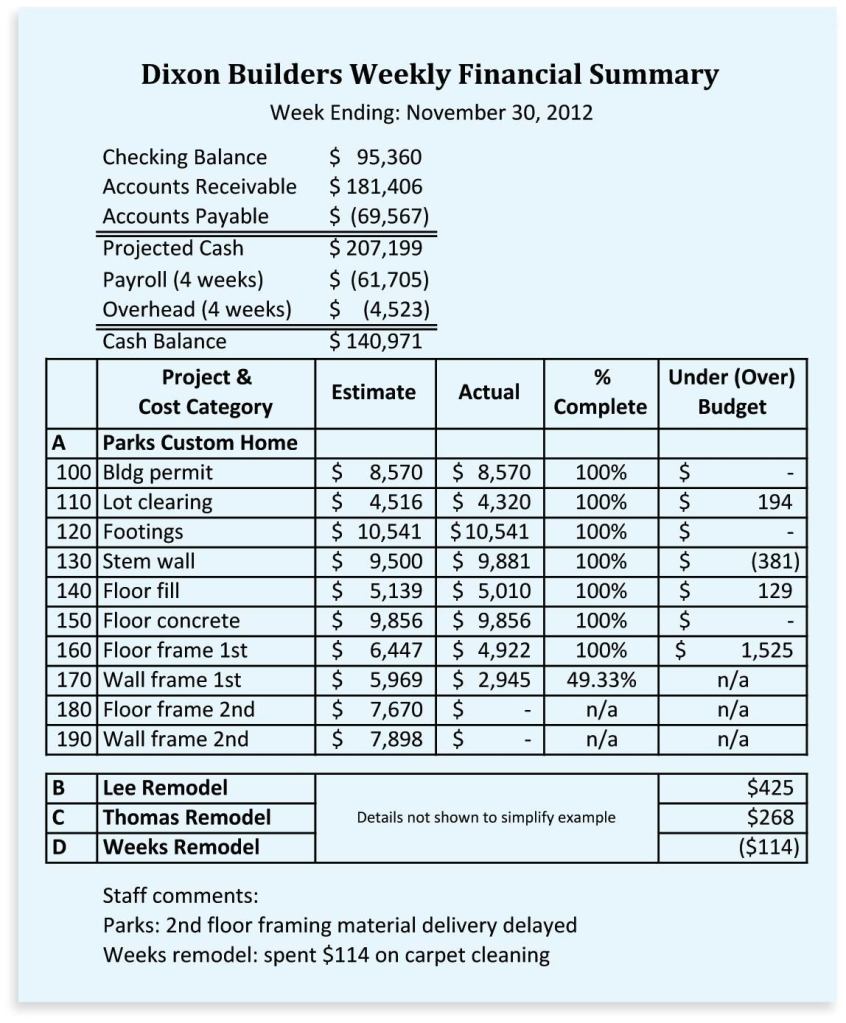

The numbers are compiled in a report I run every Friday after any invoices in that day’s mail have been entered into the computer. It begins with a simple cash summary listing my company’s bank balance, accounts payable and receivable, plus payroll and other overhead obligations. I use this section to get a quick read on what my short-term cash requirements are and to make sure I will be able to cover them. In the example here, cash flow is good, but when the “Cash Balance” line approaches $10,000, it’s a signal that something has to be done to improve cash flow.

The rest of the report is where I spend most of my time. It’s organized by project, and because all invoices are coded according to the phase of work — electrical, drywall, roofing, and the like — the projects are broken down into those categories. For each cost category, as well as for each project overall, the report shows the estimated cost, the actual cost, the percentage of the task that’s been completed, and the amount by which the actual cost is under or over budget, each in a separate column. This lets me see at a glance how the job itself stands, and alerts me to any cost categories that are over budget.

Correcting Course

For example, look at the Parks job in the sample report. It shows that the cost category “Stem wall” is $381 over budget. That’s not a huge overrun and the job overall is still under budget, but it tells me something didn’t go as planned. To find out what, I first look to the “Staff comments” section at the bottom. These are mostly taken from notes written on invoices by job supervisors, and are entered into the system along with the invoice amounts. In this case, the comment tells me the reason for the overrun.

If there’s no comment, I may know the reason from having talked with the project manager; in fact, the comments are often just a reminder, because I’m in close day-to-day contact with the project manager on each job, and I rarely have more than three jobs going at once. But if there’s no comment and I don’t already know the reason behind the overrun, the report has served its purpose by alerting me to something I may need to look into.

Sometimes an overrun is caused by something unforeseen — as was the case with the stem wall. In that case, I may talk with the job’s project manager about how we can tighten our belts in other cost categories to get the job back on track. Other times, an overrun may be caused by additional work that is out of the project scope. The action I take depends on how the individual job is performing overall, as well as on how all jobs taken together are performing.

For instance, sometimes a homeowner asks for a few extra electrical outlets. Typically, we will install them as a courtesy. (I actually think this is good marketing, and I make it a point to write a “no charge” change order.) But if the job is already over budget, our change order will charge for the work.

I also look at each job in the context of my entire workload. Say I have three remodels going, and my review shows a $500 cost overrun on one of them because of a roof repair. The budget for that job may be so tight that it would be difficult to make up the loss. But if my report also shows that the other two jobs are under budget, I’ll feel better about writing off the $500. I will certainly look to learn from the experience to avoid repeating the problem, but what’s important is that the company as a whole is meeting its earnings projections.

Caveats

This system only works if you accurately estimate projects. In fact, one benefit of doing this weekly is that you will find out very quickly if your estimating has become sloppy.

This system also demands that you understand the portion of your overhead borne by each job, and that you properly allocate overhead charges to cost overruns and job delays. My company overhead is $55 per hour, which I calculate by taking the dollar value of my yearly overhead (a number that includes all office expenses as well as my salary) and dividing by total working hours per year. If an overnight blizzard requires carpenters to spend three hours shoveling snow before they can start work the next morning, and if there’s no other job underway that they can go to, the extra cost is their time plus $165 in overhead.

When there is a cost overrun, you can diagnose it only if you have accurate details. To get them, your employees’ time cards have to record exactly how they spend their time. That’s especially important for extra work that’s eligible for a change order. By the way, this only works if managers don’t chew out employees for making honest mistakes. A carpenter who gets in hot water for doing work that’s essential but out of the scope of work will be less forthcoming about it in the future. You have to make sure everyone, including your crew and your subs, is working as a team and not blaming others.

There’s an old caution that “ghost supervision breeds apathy,” but doing this weekly review sends a clear message that I’m an active manager who pays attention to details. Employees and subs know I’m watching the numbers and will be talking with them if there’s a discrepancy. The fact that I’m always sharpening the pencil makes them a lot more careful about the budget.

I used to work from a more complex, more detailed report, but it took too long to plow through it. In fact, I used to dread Friday afternoons. Since I’ve whittled it down to one page, I can get all the information I need in about 10 minutes. I end the week knowing that either every job is on track or I’ve implemented a plan to get it back on track. That makes for more-profitable jobs — and stress-free weekends.

Dennis Dixon is a licensed general contractor in Flagstaff, Ariz., and a frequent contributor to JLC.