A client I met with recently expressed frustration with his cash flow. Since he’d been selling and producing jobs much more successfully than before, I was somewhat surprised, and together we started hunting for the reason.

Our first thought was that the latest job had been unprofitable. However, after I ran reports, it turned out that the job itself had been extremely profitable. In fact, because some costs had come in under budget, the job was actually among his most successful. Obviously, the problem wasn’t poor pricing or cost overruns.

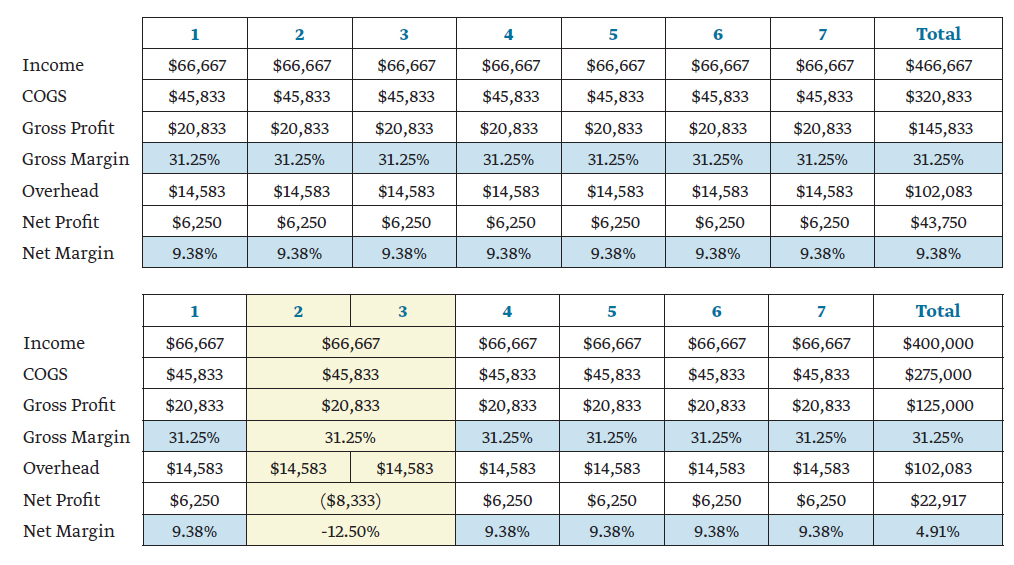

Click here for larger version.

Then, he mentioned that the job had gone well but very slowly. Family matters had required his attention and the job dragged on well past its intended duration. As a contractor with modest sales and workforce, his jobs are done serially; that is, he finishes one job before starting the next. The job itself, taken in isolation, went great, but because its duration was longer than anticipated, the selling price that had been adequate to cover his overhead and profit for a given time period became inadequate when that time period was lengthened.

Don’t Forget About Overhead

As a simplistic example, let’s assume a time period of seven units (see first chart, above). The units could be weeks, months, quarters; whatever is closest to your company’s typical job length. To keep things even simpler, let’s assume the following:

- estimated income for the period = $466,667

- average achieved gross margin = 31.25%

- average overhead for the period = $102,083

This produces an average net profit of $6,250 per unit of time, after paying for overhead—very comfortable.

But let’s see what happens when one of the jobs takes twice the estimated duration (see second chart, above). Instead of wrapping up in time period #2, this job continues into time period #3. The result is that there is twice as much overhead ($29,166) for the same amount of gross profit ($20,833), leading to negative net profit (-$8,333) and the inability to cover overhead. Note that although achieved gross margins on individual jobs look fine, total revenue drops because fewer jobs are being completed in the given time period. As a result, overall profit drops and cash-flow challenges can occur. If this happened twice, or more, the results would be even more dramatic.

So beware of the hidden effects of allowing jobs to fall behind schedule. This is the reason that many contractors place an increased markup on change orders, because they know that change orders usually delay job completion, which in turn can reduce overall income. Paying attention to delays is necessary in order to maintain not only your schedule, but also a healthy cash flow.