This month I want to talk about one of the most important aspects of a purchasing system: the ability to accurately capture, manage, and minimize unwanted job-cost variances. We’ll also discuss a related topic – using your purchasing system to better manage change orders and allowances.

A “variance” is anything that varies from what you had originally planned. A time variance occurs when a task takes longer or shorter than you had scheduled, and a cost variance happens when something costs more than you had estimated in your project budget. Since we’ve been talking about direct job costs, we’ll tackle cost variances in this column.

If you work mostly on fixed-price contracts, uncaptured variances can quickly put you upside-down on what should have been a profitable job. They can do a lot of damage to cost-plus jobs, too, because variances that come in after you’ve done your final billing can wind up coming out of your pocket – or out of your reputation as a good project manager.

Variance Codes

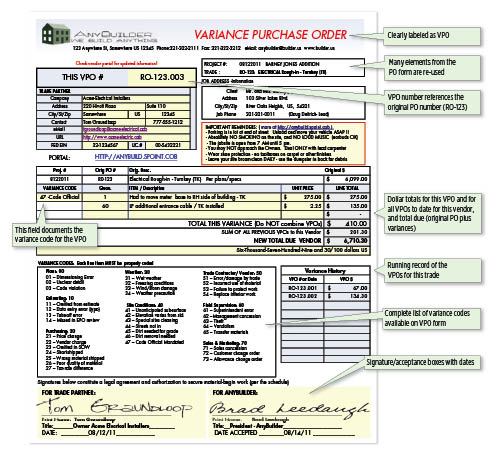

Tracking variances not only helps you protect the profit on your current job – it also gives you a way to measure the performance of your entire business so you can improve its operation over time. The first step is to develop a consistent set of variance codes. The set of codes I recommend appears in the variance purchase order (VPO) form.

Just the act of assigning a code to a variance is helpful, because it forces you to really think about the source of a problem. For instance, let’s say you end up needing more concrete than you’d planned. To assign this variance a code, you need to decide whether it was the result of an unexpected patch of bad soil you had to remove (#41-Unanticipated subsurface), or a screw-up that happened while shooting grade (#42-Elevation varies from standard).

But it’s over the long haul that this system really shows its value. After you’ve been using the codes for a few months, you’ll start noticing patterns – problems that crop up again and again. These red flags can help you pinpoint exactly where your business’s weak areas are, so you can figure out the most effective solutions. For instance, let’s say you’ve been coming up short on lumber lately. If you review your code history and see a whole string of #13-Takeoff errors, you’ll know that you should spend some time honing your estimating procedures. But if the code that pops up most frequently is #63-Theft, it might be wiser to simply arrange for better physical security on your job sites.

Or – another example – let’s say you need to reframe the floor system on a couple of jobs after your plumber incorrectly hacks an I-joist. Depending on what your variance codes tell you, you might need a new plumber (#51-Error/damage by trade) or you may just need better information on your plans so the toilet flanges are headered off properly to begin with (#02-Unclear detail). In short, properly coding and tracking variances over time will reveal the recurring problems that are draining money from your business. Having this record should take much of the guesswork out of analyzing cost overruns.

Variance Procedures

Variance procedures need to be part of the blanket trade agreement you put in place with all of your subs and suppliers (see “Putting Your Purchasing System to Work,” 9/11). Each supplier and subcontractor should be put on notice that unless a request for goods or services (over and above the original purchase order) is accompanied by a VPO that is prepriced, precoded, and signed by you or your project manager, you will not be responsible for it. This might cause some job-site delays at first, but you have to hang tough.

A good way to keep things rolling on the job yet still get the VPOs you need is to allow your lead carpenter, project manager, or office staff to hand-write and approve cost overruns up to some small amount – maybe $50 to $150 for a remodel and up to $250 on a new home. Anything above that cutoff must be pre-approved by you (or other senior management), with the VPO issued before the service is rendered or the materials are delivered. The idea is to address variances caused by external forces (theft, bad estimating, hidden conditions) immediately while avoiding variances caused by unwanted price increases altogether. Let your suppliers know that if they are unable to honor their original agreement (the signed PO), that’s their choice – but then you are not obligated to use them on your project. Some contractors set a limit for price increases – 1 percent to 2 percent, perhaps – and automatically re-bid the PO if that limit is exceeded. Again, all of this should be outlined in the vendor agreement so that there are no surprises when these issues come up.

Logistics. You don’t need a high-tech system to issue the field or office VPOs; preprinted three-part paper NCR forms are fine. One copy goes to the vendor, one goes to the field, and the third is for the office. The number on the VPO should reference the original PO so it can be tracked (which is another reason to always send at least a list of the open POs to the field with your project manager).

Once a week you’ll review all of the VPOs for the week, update the job costs, and see if there’s anything you can do to avoid more variances. Your goal is to nip little cost overruns in the bud before they become big cost overruns.

Variance Reporting

There are a ton of ways you can slice and dice your variance codes in order to gain useful insights into your business. Here are a few:

The total number of VPOs per project (or per project manager, per salesperson, per type of job)

The total dollar value of variances per job (or total variance dollars per trade)

The total number of variances per specific trade/operation (for example, framing lumber)

Total variances as a percentage of the original total project budget

Of all the variance reports you can do, that last item – total variances as a percentage of the original project budget – is the most important over the long term. The magic number you’re shooting for is 1 percent or less of the original estimated cost budget. For example, if you originally estimated that a job’s labor and materials would come to $15,000, your target would be to keep the total of all variances for the job below $150. Don’t be surprised if you start out in the 5 percent range or even higher – the idea is to get on a positive trend line as you tighten your estimating and purchasing procedures, and work toward that magic 1 percent over time.

Because you need absolute consistency in how you report variances, they should always be reported against the original estimated direct cost budget – not against the selling price!

Change Orders

A change order is a change to the contract scope-of-work that occurs after the construction agreement is signed. (Changes that occur before final agreement are contract addenda, not change orders). Change orders are a special kind of variance. Because you’re trying to develop a consistent variance trend line that you can track over time – and change orders are a complicating factor – you’ll want to track them separately from your regular job variances. If the change orders are extensive on a particular job, you should treat them as a completely separate project at the same address when you make out your variance reports. Here’s an example:

Jones Room Addition

Variance as percentage of original project budget: 2.25%

Jones Room Addition Change Orders

Variance as percentage of original project budget: 3.15%

Change-order VPOs. Change orders are supported by change-order VPOs. Once you have a signed change-order agreement, you’ll release a VPO to each vendor involved, coded to #72–CO. Like any VPO, a VPO for a change order should reference the original purchase order.

How About Allowances?

After change orders, allowances are the most common source of misunderstanding between builders and their customers. To address them properly I’d really need an entire column – but for now I’ll simply explain the easiest method I’ve found, which is pay-as-you-go.

This approach requires a good vendor agreement before the job and consistent communication between you and your supplier during construction. At the beginning of the project, you release a PO to each affected vendor for the full amount of the allowance. Your customers then visit the showroom with their shopping list and select their items. Anything they spend over and above the allowance is between them and the supplier – and your customers should write the supplier a check out-of-pocket for the balance of their selections (including any up-charges for installation labor) before they leave the store. What you do not want is an invoice from the supplier that is not supported by a PO or VPO; this method eliminates that possibility.

In the unlikely event that your customers don’t spend all the money available, you would issue a VPO to the supplier for the amount of the underage (lowering your obligation to that vendor) and cut a check back to the customers for the amount they didn’t spend (satisfying your agreement with them). The wrong way to handle an allowance credit is to wait for the vendor to send you a refund check – or worse, let the vendor keep the balance for you as “store credit.”

This pay-as-you-go method is clean and eliminates complicated reconciliation with your customer at the end of the project. Forcing customers to pay for allowance overruns at the time of purchase also helps keep them grounded in reality and greatly reduces the likelihood of “champagne tastes on a beer budget.”

JLC contributing editor Joe Stoddard moderates the Business Technology forum at jlconline.com.