It happens all the time. Work is slow, so the construction company owner decides to put the crew to work on his own home, or on his mom’s house. How this is handled on the accounting side can produce a variety of effects on the company financials.

Setting the Scene

For the sake of simplicity, let’s assume that all the work performed occurs within the company’s tax year. Let’s further assume that the project was set up as a job and costs were recorded in exactly the same manner as if it were a “real job.” In this case “real job” refers to the fact that the cost to produce will be offset by income that exceeds the costs by a margin adequate to cover overhead and allow for profit.

Identifying the Costs

It should be possible to run a report showing all the costs for the job. This will only be true if the costs (including time that was incorporated into payroll) are consistently recorded for the job.

Effects on the Financials

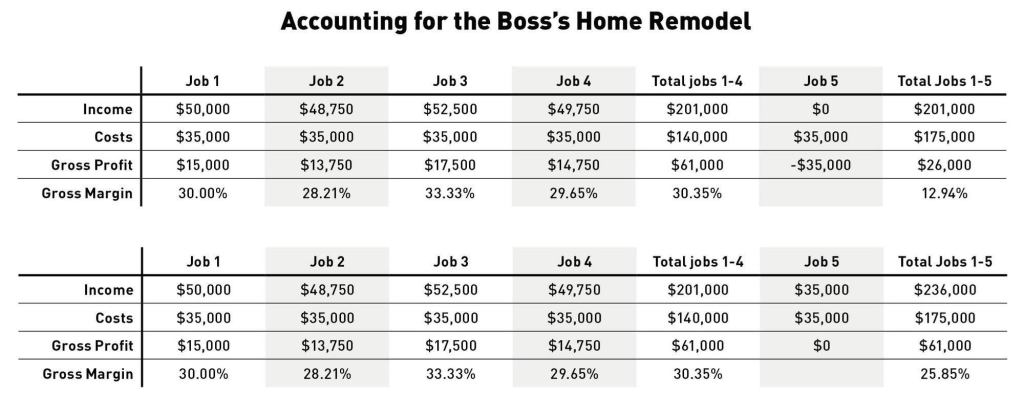

While it may feel like there’s nothing wrong with having the crew perform personal work, the result will be to reduce the achieved margin. In the example below, let’s assume that there are four “real jobs” that each cost exactly $35,000. Let’s further assume that they have been sold at a reasonable markup and that the average margin on the four jobs is 30.35%. Things are looking pretty good, right? OK, now let’s add a fifth job with the same cost. Because there is no income to offset the costs, the overall margin of the five jobs drops by more than half, to just under 13%.

Many business owners then think, “Well, all I have to do is charge myself (or my mom) exactly what the work cost. That’s still a bargain and because my production costs are covered, my overall margin shouldn’t be affected.” But there’s a problem with this reasoning, as shown below. The margin still is significantly reduced because the “sale price” of Job 5 doesn’t include markup. The overall margin still drops by nearly 5%, to just under 26%.

What to Do About It*

Option 1: Invoice for the costs and accept the reduction in profit. This means that the owner will appear to owe the company the invoiced amount. If desired, Accounts Receivable can then be credited and offset to draws or distribution (depending on the nature of the business: partnership, corporation, and the like).

The final result will be:

- Costs and income that remain on the financials

- Job profitability of $0 (on the financials and job cost reports)

- The owner will owe nothing

- The costs will eventually be classified as income on the owner’s personal tax return*

Option 2: Remove the costs from the financials by entering an adjustment to reclassify the dollar value of the work as a draw or distribution (depending on the nature of the business: partnership, corporation, and the like). This will probably eventually show up as income on the owner’s personal tax return.

The final result will be:

- Exclusion of the job from the financials since the costs were adjusted to equity and the work was never invoiced

- Job profitability showing a loss (job cost reports only)

- The owner will owe nothing

- The costs will eventually be classified as income on the owner’s personal tax return*

*Seek the advice of a qualified tax accountant before implementing any of these suggestions.

Final Thoughts

There’s nothing wrong with using the company’s resources for personal use. After all, taking a draw is the only way a sole proprietor can pay himself, and even corporate officers take distributions in addition to paychecks. The key is to recognize that having the company perform work for the owner isn’t essentially any different from taking money out of the company, and this fact should be reflected in the way it’s recorded in your financials.

Melanie Hodgdon is owner of Business Systems Management and regularly speaks on business topics at JLC Live. She is co-author (with Leslie Shiner) of the book, A Simple Guide to Turning a Profit as a Contractor. melaniehodgdon.com