Since the day the first cave family hired someone to make them into a “hut family,” contractors have been struggling with the tough operational questions that go hand in hand with growing or running a business:

• When can I hang up my toolbelt and get out of the field?

• Should my first employee be a secretary, a salesperson, or a project manager?

• How much can I afford to pay employees?

• When does it make sense to move off the kitchen table and open a real office?

• How many jobs should a salesperson sell and a project manager manage?

• Should I discount my prices to get more work? By how much?

• What about starting a couple of spec houses — good idea or not?

There’s a way to take nearly all of the guesswork out of these and many other important business decisions. It’s broadly referred to as “management accounting,” and while it’s similar to the GAAP (generally accepted accounting principles) that your accountant would use to calculate your taxes or prepare financial statements when you need a loan from the bank, there are significant differences.

GAAP accounting — also known as financial accounting — is largely historical, a meticulous record of where you’ve been. Management accounting, by contrast, is forward-looking: It tells you not only where you’ve been, but where you’re going — and it tells you far enough ahead of time that you can change course if you need to. Once you understand the principles of budgeting and tracking in management format, you’ll have the closest thing to a crystal ball this side of Harry Potter. With a few key spreadsheets and reports, you’ll be able to operate your business like never before, knowing beforehand that a decision to hire an employee, open an office, or take on a new type of work will be successful.

Note that I’m not an accountant and dislike tedious “bookkeeping” as much as the next guy. Management accounting is not a substitute for your CPA. If you don’t already have a good accountant, please go find one who is expert in the issues surrounding a construction company: minimizing your taxes and managing your liability exposure (so you don’t lose everything you’ve worked for if somebody is hurt or killed on your job site).

While many of the same concepts found in financial accounting still apply — gross profit margin, direct vs. indirect costs, and fixed vs. variable costs, for example — management accounting practices will sometimes differ from what your accountant does. That’s perfectly okay. Just follow your CPA’s advice to the letter when it comes to any financials you need to show to the outside world.

Over the next several months I’ll cover the specifics of management accounting and show how it’s used to make specific decisions that every contractor faces. This month I’ll start with some basic principles and identify some of the key metrics. And if something doesn’t make total sense, don’t worry — I’ll be revisiting specific topics in greater detail in future articles.

Planning the Work, Working the Plan

Most builders understand a project budget — planning how many 2x4s or how much labor will be required for a project. The foundation of working “by the numbers,” though, is not just budgeting job costs but actually planning your sales and revenue based on some key factors: gross profit, break-even volume, and your personal income requirements. In other words, you’re going to plan to succeed instead of just taking any job that shows up.

Gross profit. Builders tend to think about “profit” in terms of what’s left over after all the bills are paid — that is, net profit. But in fact, gross profit margin is the primary business driver in a “by the numbers” approach, for reasons that will become clear as we go along.

The simple formula for gross profit margin is:

Total Sales ˆ’ Cost of Goods Sold = Gross Profit

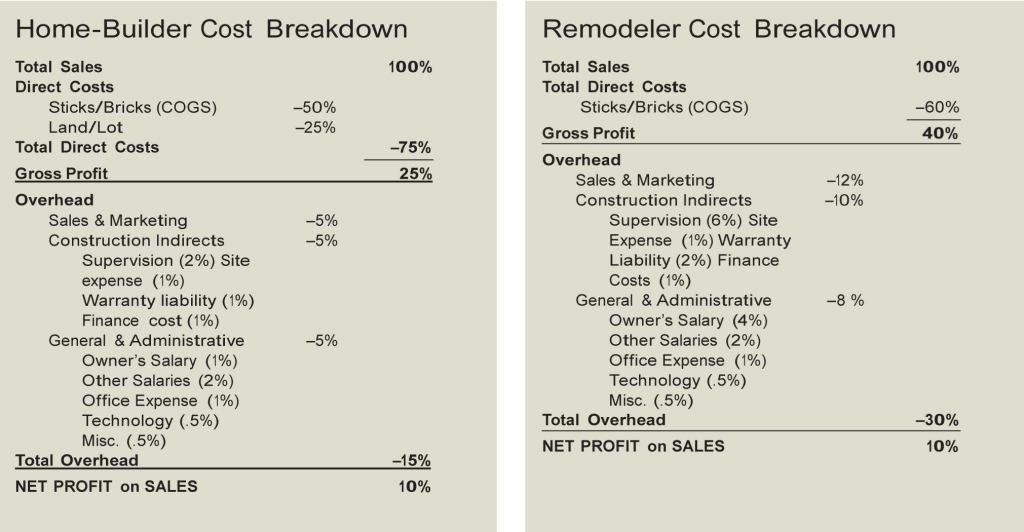

Gross profit (GP) is the difference between what you sell jobs for (total sales) and the cost of your “sticks and bricks” — the materials and labor required to produce the project. GP is what you have left before taking out any of your “overhead” (office expenses and utilities, for example) or any of your “indirect” job costs, such as supervision, warranty liability, or site costs like Porta-Johns and job trailers.

I’ll leave the details for a future column; for now, just remember that most new-home builders need to have a gross profit of 25 percent or so, but for remodelers that number jumps to 40 percent to 50 percent of sales. Why the big difference? Because remodeling projects are smaller in dollar volume, there are higher sales and marketing costs, there’s more supervision required, and there’s greater warranty exposure (see illustration, facing page).

Why is it so important to focus on gross profit and not just on the bottom line? Well, which would you rather do — run yourself ragged, or earn the same money dealing with fewer projects? Adding or subtracting just a few percent to your gross profit on every job can change your entire outlook for the year. Of course it’s important to keep your overhead under control, but it’s even more important to plan for the highest gross profit possible on every job you do. This brings us to the next important metric, your break-even volume.

Break-even volume. In a “by the numbers” operation, your break-even volume is the minimum amount of work (in dollars or number of projects) required to “cover your nut” and keep your doors open for some period of time, typically a year. It comes before your net profit, which is the return on your investment, but after you’ve paid yourself for everything you contribute to the business. The doors couldn’t stay open without you, so you deserve some percentage of sales as a salary for being the boss. If you sell the jobs, you’re also due a reasonable sales commission for that, and if you supervise jobs or work with tools, you should be compensated for those activities as well.

Most contractors have never calculated their break-even volume; instead, they take whatever work walks in the door, for whatever price they can sell it for at the time. That’s an inefficient way to operate, and it can lead to early burnout and business failure.

In a future column, we’ll examine how to calculate your break-even volume and the “contribution margin” for each job — the amount a job contributes to covering the total cost of keeping you in business. For now, let’s assume you’ve calculated your break-even point to be $120,000 in gross profit for the year, and your average job is an $80,000 addition that contributes $20,000 in GP. Your break-even volume is six of those projects (6 — $20,000 = 120,000), or $480,000 in total sales at a gross profit margin of 25 percent. To stay on track, you’d need to sell, start, and complete one of those jobs every two months.

Let’s say the year starts out strong — you sell two jobs at full price in January, but February brings no leads. In March, you decide to offer a 10 percent discount (–$8,000) to sign a job. Meanwhile, your lead carpenter throws in a few “extras,” giving away an additional $2,000 in upgrades to keep a customer happy. No big deal, right?