Remodeling Industry Experts Expect Steady Growth

In their attempts to explain the most recent housing boom and calculate a rate of recovery from the seemingly endless downturn that followed it, most economists have focused primarily on new-home building (particularly single-family). But the events in that industry – though related – don’t always translate directly to the home-improvement industry. In a report released in January, “A New Decade of Growth for Remodeling,” the Joint Center for Housing Studies of Harvard University (JCHS) takes a comprehensive look at the recession and recovery solely from the perspective of the remodeling sector (see the whole report at www.jchs.harvard.edu).

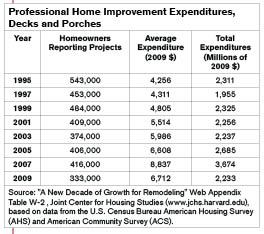

Boom. In the years leading up to housing’s peak in 2005, home prices appreciated at a formidable rate. Owners of existing homes therefore saw their equity increasing. With interest rates relatively low, lots of equity to borrow against, and no end in sight to the appreciation, homeowners had a strong financial incentive to invest in home improvements, which led to a cumulative increase in remodeling spending of almost 80 percent between 2000 and 2007.

A large percentage of that run-up, JCHS found, was accounted for by higher spending on upper-end discretionary projects, like kitchen and bath remodels and additions. Repair and maintenance spending, however, remained fairly consistent, as it tends to be less affected by broader economic conditions. Another finding was that the percentage of households engaged in remodeling over that period changed very little, though the actual number grew as the overall homeownership rate increased through 2005.

Bust. Then, after housing prices plummeted, remodeling’s bubble burst too. Between 2007 and 2009, homeowner (as opposed to rental-owner) remodeling spending declined by more than 20 percent – small beans next to some of the losses in home values, but still the industry’s largest decrease in the last quarter century. Just as JCHS attributes much of the boom to an increase in spending on upper-end discretionary projects, it also attributes much of the bust to reduced spending on those same types of projects, rather than to any reduction in the percentage of homeowners engaged in remodeling. Some of the share of spending shifted to exterior replacement projects and system upgrades, perhaps because of new tax credits for improvements like insulation and energy-efficient doors and windows.

Why was remodeling affected? For one, as home prices tanked (and they continue to fall in some areas), financial incentives for remodeling investment shrank. Some homeowners watched their equity disappear, leaving nothing to borrow against; worse, others found themselves “underwater” on their mortgages or facing foreclosure. Those homeowners, as well as banks who took over ownership of the foreclosed properties, spent at most what was required to maintain the property. Then the greater economy worsened, and unemployment became a significant factor, not just for those who lost their jobs. Others, fearing job loss, tightened spending for discretionary projects, and also postponed maintenance and repair.

Homeownership rates have been declining as well. According to the U.S. Census Bureau, 69 percent of households owned their residence at the end of 2005 (68.2 percent in 2007) versus 66.5 percent at the end of 2010. Therefore, though the percentage of homeowners that remodel hasn’t changed much, the pool of homeowners has shrunk. That’s important because homeowners spend, on average, almost twice as much on improvements each year as owners of rental units, according to JCHS.

Finally, household mobility has declined. Historically, most remodeling spending happens when sellers prepare their homes for sale and buyers customize their recent purchases. With home sales depressed, that remodeling activity is not occurring. This may be offset somewhat as the economy improves, though, as homeowners who refinanced their mortgages at historically low interest rates choose to remodel rather than move and take on a new mortgage at a higher rate.

Growth. According to JCHS, growth in remodeling spending has historically correlated to overall economic growth. With the economy and incomes expected to improve, albeit slowly, JCHS projects that remodeling spending (adjusted for inflation) will increase about 3.5 percent a year from 2010 through 2015. It estimates that the number of homeowners will increase by 4.5 million, which will account for about one-third of the increase in spending. Per household spending is estimated to provide the remaining two-thirds of the increase.

Other factors contributing to the expected growth include an aging population, pent-up demand for repair and maintenance, and aging housing stock. Older baby boomers are projected to be a significant market as they begin retrofitting their homes for a retirement lifestyle and for aging in place.

Repair and maintenance activity is also expected to increase, especially on foreclosed properties, which are going to continue to enter the market at historically high rates. These have often been neglected; the JCHS report cites a 2010 survey by the Home Improvement Research Institute that showed that buyers of those properties spend 15 percent more on remodeling and repair projects than purchasers of nondistressed properties do. Also, homeowners who put off repair projects during the recession may now be willing and able to spend money on them.

Finally, the housing stock is getting older. JCHS notes that from 2000 to 2009, homeowners in metropolitan areas where the housing is newest spent 17 percent less than the 35-metro average for remodeling. A large number of those homes, built in the 1980s and ‘90s, will soon be 20 to 30 years old and prime remodeling age.

Location. Two key predictors of remodeling spending are income and home prices, says JCHS, and both are often highest in large metro areas. Areas that were not hit as hard by falling home prices and high rates of loan delinquencies and foreclosures will do best in the coming five years, JCHS projects, suggesting the remodeling market will be strongest in metro areas of the Northeast and Midwest (which also have older housing stock) and weaker in Sunbelt states like Arizona and Florida. Specific metro areas that will continue to struggle include Chicago, Detroit, Seattle, and Tampa. – Laurie Elden

Decking Demand to Rise

In January, the market-research company Freedonia Group (freedonia group.com) released its latest report on decking, “Wood & Competitive Decking to 2014.” The report costs $5,100, which is beyond this column’s budget, but in a press release Freedonia shared some of the highlights.

There’s good news for deck builders. Not only is overall decking demand forecast to increase 2.7 percent annually through 2014, but the residential market – for both new and existing housing – is projected to grow at a higher rate than other markets. In addition, Freedonia’s research shows that homeowners will want larger decks.

Composites and plastics should continue to grab market share from wood, says the report, with double-digit gains in sales. Though wood’s sales are projected to grow less than 1 percent annually, wood will continue to dominate the decking market. Freedonia notes that “consumer interest in tropical hardwoods, such as ipe, will provide growth opportunities.” – L.E.