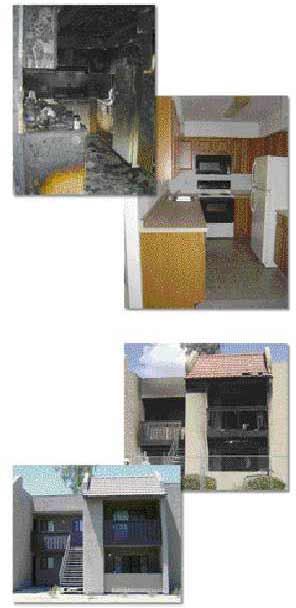

To the uninitiated, insurance companies seem to have bottomless pockets and limitless work for willing contractors. The reality is a bit different. While insurance restoration can be a lucrative source of steady income, it’s competitive and tough to break into, and the builder or remodeler who jumps into it blind can get into trouble fast. If you’re interested in this business, you need remodeling and estimating skills, along with the resources to handle messy cleanups and respond to calls on short notice. You also need the temperament to stay calm in a crisis, and to deal tactfully with homeowners who are often anything but calm.

JLC wanted to get some advice for contractors thinking of branching out into insurance work, so we spoke with Kevin Dietmeyer, partner at Minute Men Construction, a Phoenix firm that does about $200,000 per month in insurance work, most of it residential fire, smoke, and water damage. Before joining Minute Men, Dietmeyer spent three years as an insurance adjuster, so he’s seen the business from both sides.

JLC: How does a builder or remodeler go about getting insurance restoration work?

Dietmeyer: The homeowners submit a claim to the insurance company, which sends an adjuster out to inspect the damage. The adjuster will give the homeowners the option of calling their own contractor, but since most people don’t know contractors, the adjuster will often recommend two or three companies. You want to get on the adjuster’s list of recommended companies, which can be tough at the beginning. As an adjuster, I used to get a lot of brochures and literature from contractors looking for insurance work, but I rarely read them.

One way to break into the business is through plumbers. When there’s a claim for water damage, the plumber is usually the first trade to get called. Plumbers will sometimes recommend a restoration contractor, but in the Phoenix area, where I work, referrals are so sought after, plumbers often charge contractors for them.

If you do get a referral, the insurance company will want you to complete an application documenting your years in business (most companies have a minimum, which varies by company), liability insurance, and credit. You may also be asked for a performance bond, which covers things above and beyond personal liability, such as workmanship or timely completion of a job.

JLC: When bidding for work, has your experience as an adjuster given you an advantage over builders who don’t have such a background?

Dietmeyer: No. I went to work for an established company that was already getting steady referrals without an adjustment background. I do know former adjusters whose background helped them get their first jobs, but as an adjuster I worked with plenty of contractors who had no adjustment experience. Ultimately, it was the quality of their work and the way they did business that determined whether I would recommend them again.

Having said that, my experience does help me deal with adjusters, because I’m able to see things from their perspective and give them a heads-up if something happens on the job that might cause a problem for them.

JLC: How much competition is there for insurance work as compared with standard restoration, and how profitable is it?

Dietmeyer: The fee per job might be less than you are used to. When I was an adjuster, the estimates I got from experienced restoration companies were typically 30 to 50 percent lower than the estimates I got from remodelers trying to break into insurance work.

Despite these lower fees, the competition for this type of work is fierce. Restoration contractors make money on volume and efficiency. Most do the same type of work over and over — 90 percent of what we do is repairing water damage — so they make a good profit by learning to get in and out of a job quickly. And a good contractor can look forward to enough referrals to keep busy all the time.

JLC: What special tools and technical skills does a contractor need for this type of work?

Dietmeyer: You need special skills and tools to properly dry out and clean a water-damaged building. I have a $600 probe that I can run across the surface of a wall to see how much water is in the drywall. I have other probes that insert into the wall to measure water in the framing.

Once you know where the moisture is, it’s a matter of removing the water-damaged materials and properly using the appropriate drying equipment. My company dries out buildings, but a lot of contractors sub that work out to a company that specializes in that part of the business, like ServiceMaster.

The Institute of Inspection, Cleaning, and Restoration Certification [www.iicrc.org] offers continuing education classes in most areas throughout the year. Topics range from carpet cleaning to the art of drying.

After the building is cleaned and dried out, the work is pretty much standard remodeling.

JLC: Are insurance adjusters hesitant to deal with small or single-person operations?

Dietmeyer: There should be no problem as long as the small company has the proper licenses and insurance. The problem with small companies is that they tend to get overextended. It’s better to say that you are too busy to take a job than to take it and have an angry customer calling the adjuster asking why you haven’t painted the living room. If that happens, you say goodbye to any future referrals.

JLC: How does estimating insurance work differ from estimating a standard remodel?

Dietmeyer: Aside from drying out, there’s no real difference. You might charge a per-square-foot fee for replacing drywall or refinishing a floor, a linear-foot charge for installing trim, and so on.

A good estimating program helps. Room dimensions are entered by line item or through a sketch option. Once that is done, you select the scope of work and items for each room to arrive at a line-item bid that provides concise material and labor costs.

JLC: What estimating software do you use?

Dietmeyer: Three popular packages are Xactimate [Xactware, 800/424-9228, www.xactware.com.], IntegriClaim Estimator [Marshall & Swift/Boeckh, 888/337-9665, www.msbinfo.com], and Simsol for Contractors [Simsol, 800/447-4676, www.simsol.com]. Find out what program the adjusters are using in your area.

Most of our local carriers work with Xactimate, so that’s what we use. My company paid less than $1,000 for the program several years ago, plus several hundred dollars to attend a basic three-day training class. The number of users determines the monthly cost to use the program, which in our case is about $200.

JLC: How hard was it to learn the software?

Dietmeyer: No harder than any other estimating software. Once you learn the basics, you can create complete, detailed estimates very quickly. However, it takes a good 50 estimates to become really fast and to learn all the program’s shortcuts.

JLC: How do you know the software’s cost estimates are accurate for your local area?

Dietmeyer: These programs rely on regional cost data, which gets updated several times a year to follow price trends, but you can also adjust the costs yourself. We had to manually update the price of plywood when they started rebuilding in Iraq and costs suddenly went higher than Xactimate’s database indicated. When we did the next regular download of new prices, they were right on.

JLC: Is there any way a contractor can check his numbers to see if they are in line with what the adjuster is willing to pay?

Dietmeyer:: The best thing to do is to submit your estimate, then call the adjuster to talk about it. Once you’ve done a few jobs with the same company, you learn what they expect to pay for various line items.

Some adjusters will actually provide you with a printout of their line-item prices to use as a guide. When I was an adjuster, for example, I usually settled a claim by writing my own estimate and having the contractors on my list work directly from it. If market conditions force you to charge a higher price than the adjuster is used to paying, you need to discuss the higher price up-front, and provide a specific, valid reason.

“Homeowners tend to forget that the purpose of insurance is to put things back as they were, not to add that kitchen island they’ve always wanted.” |

JLC: Do all claims require multiple bids?

Dietmeyer: Not always. If a contractor is fair and provides accurate estimates to the adjuster, more than one estimate is not needed on most claims. Most adjusters keep a list of trusted flooring and cabinet companies, roofers, plumbers, and others who they not only refer business to, but trust to answer questions when a lesser-known company is on the job. When the relationship between contractor and adjuster is based on trustworthy information, guess who benefits?

JLC: When creating a bid, how do you decide whether to repair or to replace a particular item?

Dietmeyer: Repair or replace options apply to things like flooring, cabinets, and wall coverings.

Say you have four feet of water-damaged lower kitchen cabinets. If it will cost less to rebuild the boxes with the original faces than to replace the cabinets, then that is what needs to be done. If, on the other hand, it would cost more to rebuild the boxes than to buy new cabinets, you should put that on your bid, but you should provide the adjuster with documentation for your decision.

JLC: What if you run into unforeseen damages after starting work?

Dietmeyer: That’s one reason why it’s a good idea to include a detailed scope of work with your bid. If you run into damage outside that scope, you need to estimate the costs for repairing it, then get these costs to the adjuster. In some cases, small supplements are approved over the telephone.

JLC: What if you forget to put something on the estimate?

Dietmeyer: In most cases, if you notify the adjuster, there shouldn’t be a problem, especially if you have a good relationship with your adjuster and have built a reputation as an honest company.

However, in some cases you may be told that the agreed price is the agreed price, so be careful with your estimates.

JLC: Do adjusters try to pay as little as possible for a claim, or are they generally fair?

Dietmeyer: It varies, not just by company, but by the particular manager in charge of the local office.

The insurance company I worked for was willing to pay whatever the policy owed, but some companies are tighter. There is one insurer that we won’t do business with because they lowball estimates.

Also, inexperienced adjusters will become afraid or skeptical when they see bigger numbers and might try to pay less than the job is worth.

When I got into the restoration business, it was a real eye-opener to see that a job I thought should take eight hours really required 20.

JLC: It obviously costs a contractor more in overhead to do small jobs. Do adjusters take this into account?

Dietmeyer: My former company often paid a minimum for small jobs that was higher than what it would cost if priced out by the square foot. We did this to compensate for the higher overhead costs and added hassle for the contractor.

Insurance work requires a good piece of estimating software. Dietmeyer’s company uses Xactimate because it’s what most of his local adjusters use. The software relies on a database of labor and materials prices, which gets updated several times a year. Dietmeyer is able to print out a detailed scope of work and pricing for each item, which he asks the homeowner and adjuster to sign before he begins work.

JLC: What is the typical payment schedule?

Dietmeyer: The first payment is usually the actual cash value of the job, which is replacement cost less a depreciation figure.

You may be asked to start work before getting the first payment. If this happens, be sure you have an agreed scope and pricing with the adjuster and homeowner before starting work.

JLC: Does the insurance company pay the contractor directly?

Dietmeyer: Some companies will pay you directly with authorization from the insured homeowner if you’re on their vendor list. Most companies send the check to the insured, often with only their name on it. The insured is supposed to pay you, but you might guess what sometimes happens — a vacation, a car, or some other toy. With experience, you learn to anticipate this type of thing.

My advice is to listen carefully when homeowners talk about finances. If they keep talking about how they’re behind on their house payments, that’s a red flag.

JLC: Are homeowners generally hard to deal with?

Dietmeyer: Not always, but some can be. Homeowners tend to have a difficult time understanding that you will be paid only for work directly related to the covered loss. They also tend to forget that the purpose of insurance is to put things back as they were, not to add that kitchen island they’ve always wanted.

To make sure they understand this, it’s always best to take the time to meet with the homeowners and go through the approved estimate room by room, or even line item by line item. If the insured wants you to inflate the claim, refer them back to the adjuster. If they tell you someone else will agree with them, walk away.

Even a homeowner who seems to understand this can cause problems after work starts. Your crew may be asked to paint an extra room, move a doorway, build a pantry, or whatever else is on the insured’s wish list. Or the insured may expect you to give them a marble countertop to replace their smoke-damaged laminate.

JLC: How hard will a homeowner push for these kinds of extras?

Dietmeyer: The average person will take one shot and stop when it doesn’t work. Then there’s the occasional nightmare customer.

For instance, we were recently referred to a job where the old kitchen cabinets had gotten wet when the upstairs bath leaked. There was no damage, so we moved them out of the way and mopped up water. They dried out. The problem was that the homeowners desperately wanted new kitchen cabinets. They called us several times to tell us that they had spoken with the adjuster, and that the adjuster had authorized replacement cabinets. We called the adjuster and were told that wasn’t true. If we had discarded the old cabinets, then found out the insurance company hadn’t authorized it, we would have been liable.

We’ve actually had cases in which customers refused to pay us the final amount owed to us unless we did some extra work for them. Some will get real threatening and say there’s mold in cabinets and threaten to sue you. My advice in these situations is not to take the bait. The customer who holds the last payment hostage will usually hold back payment no matter how much free work you do.

JLC: How do you protect yourself against this?

Dietmeyer: All you can do is communicate. Talk to the adjuster before you do any work. And make sure to keep the homeowner in the loop. Be very clear about what the estimate does and does not include, and have the homeowners sign off on it.

In our contract, for example, the homeowners have to agree to endorse any insurance check to our company, and to authorize us to sign any insurance checks made out to them.

The most important thing you can do to protect yourself is be fair and honest with everyone. An adjuster who has confidence in your integrity based on past experience will be much more willing to consider any special situations or needed supplements, and will be more willing to back you up when there’s a dispute with the homeowner.

Finally, realize that sometimes the best thing you can do is walk away from a job before it starts. Don’t be so anxious to be busy that you’re willing to take anything.