In previous articles, we differentiated between production costs (classified in accounting as Cost of Goods Sold and often abbreviated COGS), considered profit as just another expense, and learned how to calculate gross margin and gross profit based on actual historical numbers. In this article, we’ll put it all together and we’ll see how you can apply simple formulas to give you “what if” scenarios for projections.

Let’s look again at a simplified profit and loss and the formulas for gross margin and markup. We’ll keep our gross profit fixed. You will always know what that is, because you’ve isolated your overhead and named your profit. Gross profit is the sum of these. But this time, we’re going to learn the formulas required in order to perform a series of “what if’” scenarios.

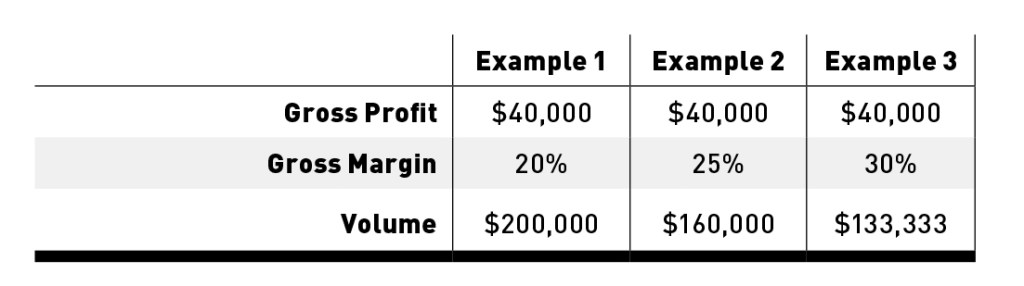

Different Margins Yield Different Volumes

If you know your gross profit and you experiment with various margins, you can see the theoretical sales volume required to meet your overhead and target profit.

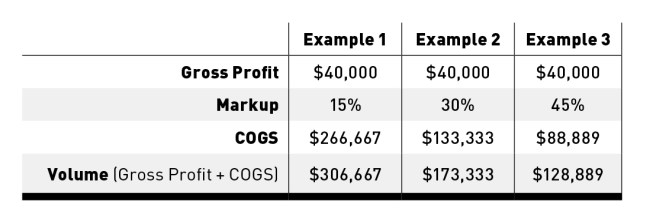

Different Markups Yield Different Volumes

If you know your gross profit and you experiment with various markups, you can see the theoretical sales volume required to meet your overhead and target profit.

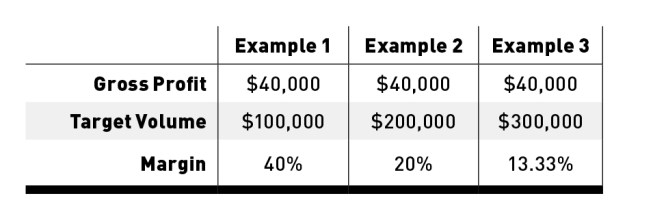

What Margin Do You Need to Meet Realistic Volumes?

Now let’s rein in the sales volume to get some realistic numbers for, in this example, a small volume remodeler. (You may be comfortable with a larger volume, but we’re going to start off conservatively. You can grow from here.) If you know your gross profit and you experiment with various possible realistic sales-volume amounts, you’ll see what margin would need to be achieved at each sales volume in order to meet your overhead and target profit figures.

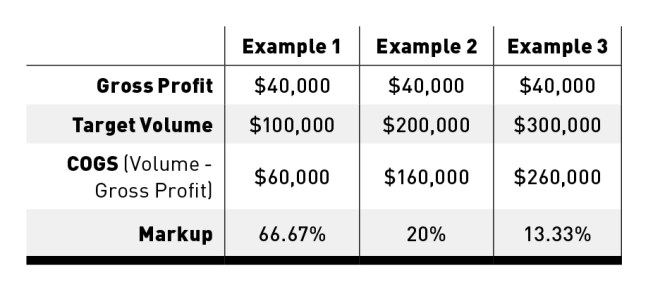

What MarkUp is Needed to Meet Realistic Volumes?

Taking these same realistic volume figures, you can calculate the markup you need to apply. Then, using the markups, you can price your jobs accordingly, secure in knowing that you will actually make a sustainable profit, provided you hit your sales volume target.