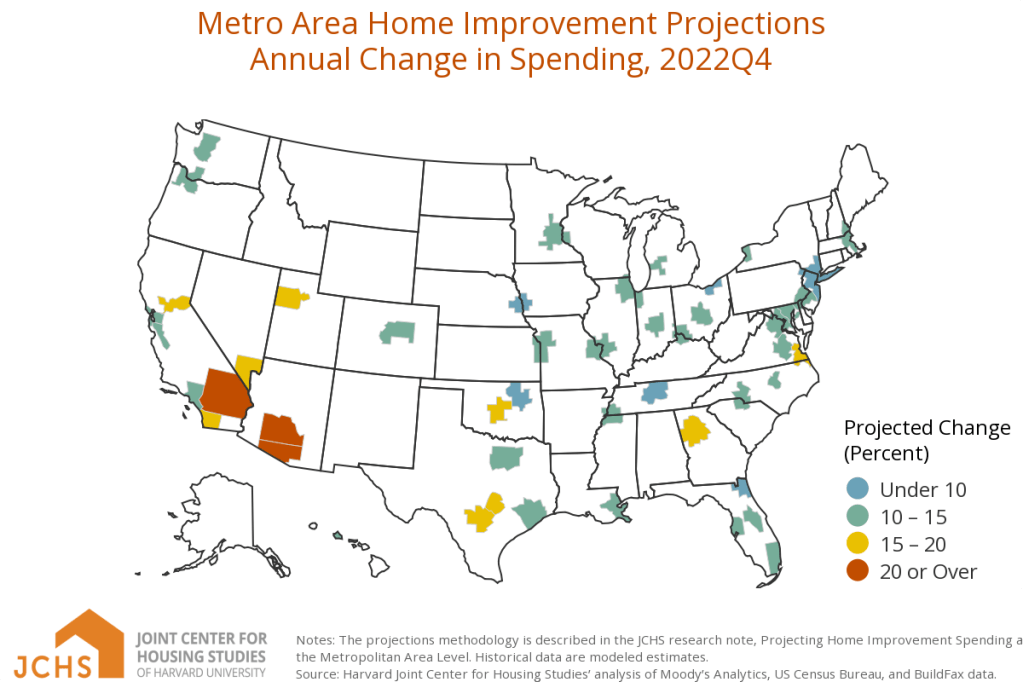

Expenditures for improvements to the owner-occupied housing stock are expected to increase at a faster pace in most of the nation’s largest metropolitan areas in 2022, according to the Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University (JCHS).

The JCHS projects annual growth in home improvement spending of 13.8% across the 48 major metropolitan areas tracked in 2022, with owner expenditures expected to grow between 7.6% and 23.0%. Of the 48 analyzed metros, 20 are expected to see above average growth of 14% or greater, with six metros—Tuscon, Ariz. (23.0%); Riverside, Calif. (21.9%); Phoenix, Ariz. (20.3%); Austin, Texas (19.2%); San Antonio, Texas (19.1%); and Las Vegas (17.5%)—expected to surpass the projection for national remodeling spending of 17% growth this year. All but one of the metros tracked show higher growth projected for 2022 compared with 2021 estimates.

“Record-breaking home price appreciation, solid home sales, and high incomes are all contributing to stronger remodeling activity in our nation’s major metros, especially in the south and west,” Sophia Wedeen, a research assistant in the Remodeling Futures Program at the JCHS, said in a prepared statement.

Carlos Martin, project director of the Remodeling Futures Program, said ongoing shortages and rising costs of labor and building materials may dampen some of the projected remodeling acceleration in 2022.

“There will be shifts in local supply chains and the remodeling workforce as regional economies pull out of the pandemic, and as homeowner needs and activities change,” Martin said.

Due to data discontinuation, the 2022 metro projections substituted total existing home sales for existing single-family home sales as a model input. The Metro Area Home Improvement Projections are released annually to provide a short-term outlook of home improvement spending to owner-occupied homes. The indicator, developed with biennial estimates from the American Housing Survey, is designed to project the annual rate of change in spending for the current quarter and subsequent three quarters in approximately 50 of the largest metro areas, and is intended to help identify future turning points in the local business cycles of the home improvement industry.