In my previous series on retirement, I discussed the need for construction business owners to save for retirement. I identified various retirement savings accounts you can establish, and I emphasized starting early, being motivated, making sacrifices, and taking advantage of tax-free saving. I did not discuss Social Security as a part of overall retirement planning, so let’s dive into that now.

A History of Social Security

Social Security was signed into law in 1935 with the passage of the Social Security Act, a response to the devastation inflicted on the average American family by the Great Depression. As part of President Roosevelt’s goals to provide protection from poverty in old age and from job loss, two of the benefits established under the act were retirement and unemployment insurances. Social Security benefits were meant to be combined with family savings to prepare for retirement. That is true today as well; Social Security should be combined with personal savings and tax savings retirement accounts to prepare a family for its future. In addition to retirement and unemployment benefits, the act provided assistance for work disabilities, assistance for children of retired, disabled, or deceased workers, and benefits for survivors of deceased workers. Other benefits have been added since the passage of the law.

Social Security is not an entitlement; it’s insurance that you pay for. Money is deducted from your paycheck each month as a payroll tax known as FICA (Federal Insurance Contribution Act). Every year, you pay 6.2% of earnings up to $142,800; that contribution is then matched by your employer for a total of 12.4%. An additional 1.45% is deducted from your earnings for Medicare, which is also matched by your employer for a total contribution of 2.9%. If you’re self-employed, you contribute the entire amount—12.4% for Social Security and 2.9% for Medicare.

There is a tremendous amount to know about the many Social Security benefits—disability benefits are especially significant for those of us in the construction trades—but for this article, I am going to focus on retirement benefits. Social Security’s retirement plan is perfect for our industry. Participation is required, and you can’t skip the contribution to pay a supplier, a liability insurance premium, or a truck loan. You can only complain that your paycheck looks a bit light. On the bright side, if you’re an employee, your contribution is matched, and for both employees and employers, there’s a good chance you or your family will get more money back from Social Security than you put in. With participation required, there is only one decision you will need to make once you qualify for drawing Social Security: at what age to start collecting.

Qualifying for Social Security

To qualify for Social Security, you have to accumulate 40 credits. A credit is awarded for every $1,410 earned up to four credits a year. If you make $5,640 a year or more for 10 years and pay FICA taxes on those earnings, you qualify for benefits. The amount of your benefit, however, is based on your lifetime earnings (available for review at ssa.gov/myaccount). Your benefit is based on your 35 highest earning years, adjusted for inflation, in which you paid FICA taxes. If you work fewer than 35 years, a zero is added for each year you’re short. Once you have 40 credits and 35 years of earnings, you have the choice to begin collecting Social Security benefits sometime between 62 and 70 years of age.

Before we continue, let’s get the 1,000-pound gorilla out of the room. Will Social Security go bankrupt before I can collect? The Social Security Administration is projected to run out of surplus funds around 2033, but it will still collect payroll taxes and have enough funding to pay 78% of benefits. So, if Congress does nothing, Social Security recipients will take a 22% cut in 2034. However, that’s not likely. Keep in mind, 76% of folks 65 to 74 vote, which is the highest percentage for any cohort. For that reason, Congress may be responsive to retirees’ needs and pass legislation to maintain benefits; some possibilities include raising taxes, raising the $142,800 wage cap for paying FICA taxes, reducing benefits for the wealthy, and raising the full retirement age. What Congress does or doesn’t do may mean thousands of retirement dollars for you, so keep an eye on Social Security news—and don’t wait until you’re 65 to vote. To maximize your benefits in case of a 22% reduction, work 35 years and delay collecting until you are 70.

When to Begin Collecting Social Security

When to begin collecting benefits is a personal decision. Your decision likely will depend on factors such as family savings, retirement savings, sources of income, marital status, your health, family longevity, and future financial needs. And, let’s not forget, do you like what you’re doing? What’s Sunday night like: Are you looking forward to Monday morning and getting back to the job, or are you anxious about returning to work? There is a lot to sort out.

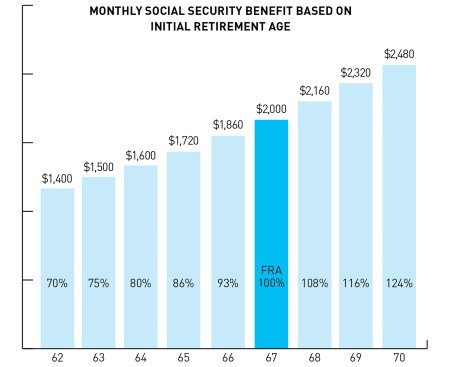

The bottom line is, the longer you wait to collect, the higher your monthly benefit will be. You can start collecting retirement benefits any time between the ages of 62 and 70, though there is something called a “full retirement age” (FRA), which is based on the year you were born. For those born in 1960 or later, the FRA is 67. (If you were born earlier, visit ssa.gov to find out your FRA.) If you start collecting benefits before you reach 67, your monthly benefit will be reduced by about 0.5% for each month you’re shy of 67; if you start collecting at 62, this reduction amounts to 30%. On the other hand, by waiting until after you reach 67 to collect benefits, you receive an 8% increase each year (8% on your FRA benefit, not on the compounded sum each year after). If you wait until you’re 70 to collect, your monthly benefit will be 77% higher than had you started at age 62. Boiling it down, if your monthly payment starting at age 67 would be $2,000, then your monthly benefit starting at 62 would be $1,400 and at 70, $2,480 (see chart, below).

For individuals born in 1960 or later, “full retirement age” (FRA) is 67—the age at which you are eligible for 100% of your benefit. The amount of your monthly benefit at FRA is based on the 35 highest earning years, adjusted for inflation, in which you paid FICA taxes. Individuals are eligible to start collecting benefits at age 62, but the monthly amount will be lower; waiting until age 70 results in a higher amount, as shown here for a $2,000 monthly FRA benefit.

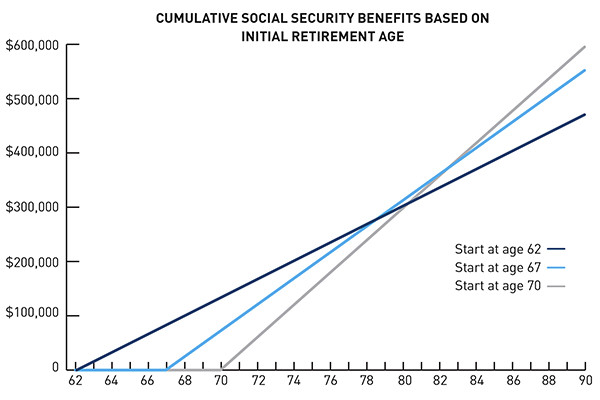

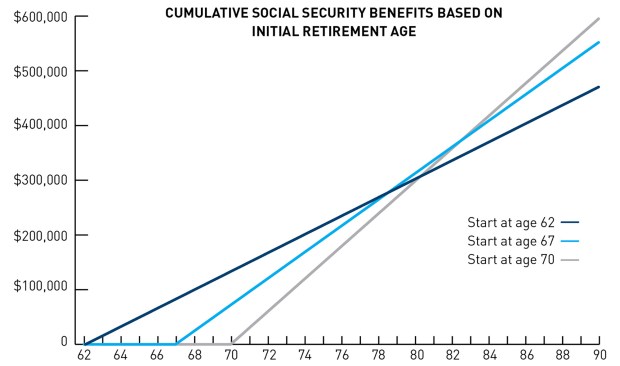

Break-Even Age

Waiting to collect benefits means you collect more per month, but you collect this higher amount for fewer years. So, how do you figure out whether it pays long term to wait? Break-even math helps you calculate how old you’ll be when the sum of a greater number of lower payments will be the same as the sum of fewer higher payments (see chart, below). That’s the age at which you will start to realize a higher lifetime benefit from waiting. Knowing this age may help you decide when to start collecting, especially if you have a particularly short or long life expectancy based on your health and family history.

Let’s use the example above and find the break-even point of starting benefits at 62 versus waiting until your FRA of 67. Starting at 62 means you will collect 60 monthly (five years) $1,400 payments, or $84,000, by the time you reach 67. If instead you start at 67 and collect $2,000 a month, it will take 11.7 years to break even—$84,000 divided by $600 (the difference in monthly benefits) divided by 12 months. That means at age 78.7, you break even and head toward the finish line with a higher monthly benefit.

What is the break-even point if you wait until 70 to collect benefits? If you start at 62, you will collect 96 $1,400 payments, or $134,400, by age 70. If you wait until you’re 70, when your monthly benefit will be $2,480 ($1,080 more per month than at 62), it will take you 10.4 years to break even—$134,400 divided by $1,080 divided by 12 months. So you are walking tall at age 80.4 with maximum benefits.

If you start benefits at your FRA of 67, you will collect 36 $2,000 payments, or $72,000, by age 70. Waiting until 70 and collecting $2,480 a month ($480 more a month than at 67) will take you 12.5 years, until the age of 82.5, to be in the green—$72,000 divided by $480 divided by 12 months. Do you feel lucky?

The longer you wait to claim Social Security benefits, the more you stand to gain over the long term, provided you live past the break-even age. Above, that would be 82.5, if you are comparing starting at 67 versus 70 (based on a $2,000 monthly payment at a full retirement age of 67).

Other Considerations

Be aware that if you want to collect Social Security at 62 and continue to work, there is an earnings limit. If you continue to work after starting to collect at 62, you are allowed to make $19,560 (beginning in 2022) before the SSA withholds $1 for every $2 earned. The withholdings are not lost, however. At full retirement, monthly benefits are increased to reflect withholdings, and the higher monthly benefits will continue even after withholdings are paid back in full (about 12 years). Once you reach your FRA, there is no earnings limit or withholdings, and you can work and collect with no earnings penalty.

Inflation. A wonderful feature of Social Security’s retirement benefit that should be considered in your decision-making process is the cost-of-living (COLA) adjustment (not guaranteed each year). You have to look long and hard to find other investments with such an inflation hedge. This year’s COLA is 5.9% effective January 2022. Cost of living adjustments apply if you start at 62, but if you can wait until you’re 70, you get not only the 8% a year delayed retirement credit each year after FRA but also a cost-of-living adjustment on a larger base, which has a compounding effect. This may be significant if inflation is persistent during your retirement or you or your spouse live to a ripe old age.

Life expectancy. Here are a few life expectancy estimates from the SSA: A typical 65-year-old today will live to 83, one in four 65-year-olds will live to 90, and one in 10 65-year-olds will live to 95. People are living longer, and generally, women live longer than men.

Spousal benefits. A surviving spouse with a lower benefit can collect their partner’s higher benefit upon the partner’s death. If at the time of your spouse’s death, they are collecting $2,000 a month and you are collecting $800 and are at your FRA, you now qualify for their $2,000 a month benefit instead. So, collecting early at 62 rather than at your FRA or 70 may mean your surviving spouse will receive less money in monthly benefits and have a lower COLA base for the rest of their life. (Unfortunately, in the example above, the household income drops from $2,800 to $2,000.) The longer a spouse lives, the less likely family savings will last and the more likely they will need a larger Social Security benefit that adjusts for inflation. So, the proper age to start benefits may not be about how much you may collect in your lifetime, but about how much your family may collect.

There is a second spousal benefit, for a couple rather than a widow or widower, that may bring additional retirement benefits into your household. Using the $2,000/$800 example above and assuming both spouses have reached their FRA, the lower earner can collect 50% of the higher earner’s benefit. So, the $800 spouse can apply to receive $1,000—while the higher wage earner continues to collect their $2,000. Collecting a spousal benefit before FRA will reduce the 50% benefit. Additional, special spousal benefits for Social Security recipients are available for retired couples with a disabled child or a child under 16.

Collect Early or Delay?

Reasons to collect early and receive a smaller monthly payment include the following: You dislike work, you need the money, inflation is not a concern, your health or life expectancy is an issue, you don’t trust the Social Security system, and you have no family to consider. Reasons to delay, increasing your monthly benefit, are: You want to continue working, you don’t need the money, you want to maximize your spouse’s benefit and COLA, you don’t want to run out of money, and your health and life expectancy are good.

So, when do you start to collect Social Security benefits? It’s an individual’s task to figure out the best scenario. Don’t hesitate to seek assistance. Start with the local Social Security office. Many communities offer free retirement planning assistance with volunteer professionals. Check into AARP (American Association of Retired Persons). Pick up a book or magazine or search retirement planning online. Talk to family and friends. Do your homework and see a paid professional, if need be. And, be thankful that the voters 87 years ago, in 1935, thought it important to make your future a bit more secure. What can we do now to make the future 87 years from now—in 2109—a better place? Cue up Zager and Evans: “In the year 2525, if man is still alive, if women can survive …”