Let’s begin this month by reviewing some basic financial concepts and benchmarks. Out of your total sales revenue you subtract the costs of goods sold (COGS), also known as your “direct construction costs” – the labor, materials, and subcontracts required to complete the project. What’s left “above the line” after subtracting those direct costs is your gross profit.

It would be great if you could just pocket your gross profit, but unfortunately you still have five major expense categories to pay for:

• Sales and marketing (advertising, sales commissions, marketing efforts)

• Warranty and customer service liability

• Financing (lines of credit and construction loans)

• Construction indirect costs (supervision, job trailers, dumpsters)

• General and administrative (office expenses, office salaries, utilities, business owner’s compensation)

All of those categories come out “below the line,” meaning they are subtracted from your gross profit, leaving you with your “net profit” – the number I hope you’re now budgeting for. Your cost structure is going to vary greatly depending on the type of work you do, which is why we’ve been separating jobs into five basic categories: remodeling, repair, new homes, commercial work, and “other” (a catch-all for things like project management and design-only work). Don’t confuse net profit and your wages or salary. You should be able to pay yourself the going rate for selling projects, managing projects, working in the field (if that’s what you want to do), and managing your business and still earn a reasonable net profit, which is really the return on your investment.

So what is a reasonable net profit? Ten percent is a good target. The best-performing businesses in our industry earn 12 percent to 15 percent net profit while the vast majority fall well short of 10 percent. Production home builders and commercial GCs can earn 10 percent on a gross profit margin of 18 percent to 25 percent, whereas a pro handyman might have to work on a 100 percent markup for a gross profit of 50 percent in order to earn that magic 10 percent net. Why? Because attracting those kinds of jobs requires more advertising and marketing, and completing them successfully requires more supervision. After they’re done, they involve higher warranty costs.

But don’t get stuck in generalizations – really, there are no shortcuts. The only way to accurately determine your cost structure is to work out your fixed overhead and then create your sales-starts-revenue budgets (“Use Excel to Budget Next Year’s Project Mix,” 12/10, and “Budgeting for Your Marketing, Sales, and Project Starts,” 1/11).

The Power of Gross Profit

Look around at your competition. There are bound to be one or two companies that always seem to land the best jobs, have the nicest offices, and employ the best people. There’s a reason they’re not struggling: Instead of always doing more jobs at lower margins, they concentrate on doing fewer jobs at higher margins.

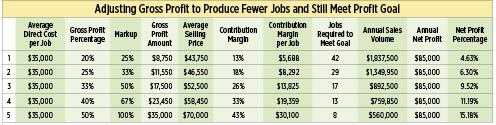

Let’s say your financial target for the year is to earn a clean $85,000 net profit – after you’ve paid yourself a reasonable salary and covered your overhead obligations (we’ll assume $150,000 for the year). Let’s also pretend your average project is a remodeling job that sells for around $50,000, and it’s up to you to apply the appropriate markup and sell the jobs for whatever you can.

The table in Figure 1 shows that if your average job’s direct costs are $35,000 and you mark those costs up 25 percent for a selling price of $43,750, you would need to complete 42 projects to meet your financial goal for the year. Note that for the purpose of illustration the table assumes a contribution margin 7 percent lower than your gross profit – representing in this case a 5 percent sales commission plus 2 percent average sales concession. These numbers would come from your actual historical records. (For a refresher on contribution margin, see “Strategic Budgeting and Your Break-Even Volume,” 8/10.)

But look at what happens if you raise your markup to 50 percent, for a gross profit margin of 33 percent: Now you have to complete only 17 projects to meet your financial goals for the year – less than half the original sales volume. True, you’ve increased your selling price by $8,750 – from $43,750 to $52,500 – but a good sales presentation coupled with stronger customer referrals should make it fairly easy to overcome price objections. Remember, you’ll no longer need 42 buyers. Now you’ll need only 17, which means you can target a more willing, more ready, more able prospect. You’ll need fewer leads and fewer sales calls, and you’ll have more time and resources to devote to the projects you do sell. Better still, if a prospect doesn’t feel right or there are any red flags early in the sales process, you can excuse yourself and look for a better fit, because you no longer have to start anywhere near as many jobs. In short, raising your gross profit margin changes almost every aspect of your business in your favor.

Net profit percentage. Something else happens when you raise your gross profit margin – your net profit as a percentage of sales also goes up dramatically.

Lowering Direct Costs

There’s another way to increase your gross profit margin: Instead of raising prices, target and reduce your direct costs. This ties together everything I’ve discussed so far in this column with the idea of being a “lean” contractor (“Putting Lean Principles to Work,” 2/11). Remember that “lean” is about the relentless identification and elimination of waste.

What if you could reduce your cost of production by 10 percent, saving $3,500 in direct costs on every project? Let’s look at three different ways this could play out.

First, lowering your direct costs by 10 percent would further reduce sales pressure. If times are slow, you could hold your average selling price at $52,500, complete only 14 projects, and still meet your original financial goals.

Or you might choose to use your original sales budget of 17 projects. Assuming everything goes as planned, that approach will increase your net profit from $85,000 to $103,000 – an extra $18,000 for the year.

Finally, if pricing pressure in a tough market proves too much to overcome, finding 10 percent in your direct costs might provide a small cushion by which you could lower your selling price yet still maintain a reduced sales volume and protect your profit.

Tighten Up

We’ll take a closer look at direct-cost- saving ideas in future columns, but for now here are a few things that you can do right away.

Build “virtually” first. After you sell a project, take time in the beginning to work out every last detail of how you’ll approach it, from staging materials on the site to fully developing any construction details that might be lacking in the plans. Every hour spent planning can save valuable time on site.

Provide complete scopes-of-work and drawings to everyone who needs them. If you don’t spell out in detail what you want from your lead carpenters and subcontractors, things are going to get done their way – which will probably require more materials (and labor) than you were planning on. It’s worth taking the time to draw the details you want so that you’re sure the people doing the work know exactly what you expect from them.

Do your own materials takeoffs. While it’s true that many lumberyards have very good estimators, their takeoffs are going to represent how they want to sell materials, not how you want to build a project. If you’re looking to lower your direct costs, there’s no substitute for knowing every last piece and part that’s required to build something. (CAD software that can generate a materials list – even an incomplete one – can save you hours of time.)

Tighten your estimates with field counts. A plan takeoff is one thing, but if you really want to figure out how to tighten up your materials requirements, you have to keep track of what was actually used and continually roll that information back into future estimates.

Review your framing practices. The average JLC reader is probably way out ahead on this count, but it’s still amazing to me how much wood is wasted in an average frame. Unneeded trimmers and special studs, headers in nonbearing walls, and wasted temporary bracing materials all add cost to the typical project.

Avoid trade cost creep. If you use subs, figure out who – you, or them – will stage the materials, provide the temporary utilities and heat, do the daily cleanup, and provide warranty service items on the work. Get it in writing and make enforcement part of your job supervision. If your crew is providing items the sub normally would be responsible for, negotiate better pricing.

Develop a strong change-order policy – and stick to it. Probably the No. 1 cause of cost creep happens under the heading of “taking care of your customer” – doing all those little things they ask for and never recovering a dime. Grocery stores don’t give you extra groceries out of the goodness of their heart, so don’t give away materials and labor to your buyers. It takes only a few percentage points in lost gross profit before you’ll need to sell and complete entire additional projects to meet your financial goals.

JLC contributing editor Joe Stoddard moderates the Business Technology forum at jlconline.com.