An Xactimate estimating screen includes categories for thousands…

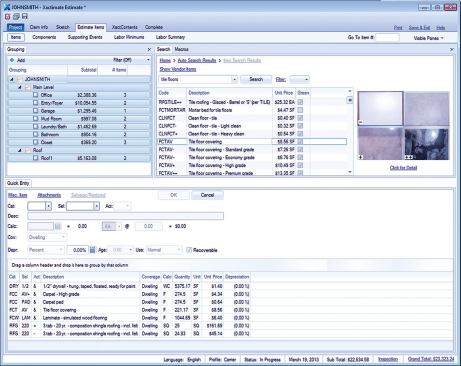

An Xactimate estimating screen includes categories for thousands of types and grades of materials, with examples and unit costs (upper right), along with a data entry screen (lower half). Dimensions are calculated and imported automatically from a drawing created in the attached Sketch program. The program also maintains a running room-by-room total (upper left).

Paul Bianchina

One of the most common insurance

restoration scenarios is dryi…

One of the most common insurance

restoration scenarios is drying out wet carpeting, pads, and subfloors.

Paul Bianchina

While a major fire can be a devastating loss for a family, it al…

While a major fire can be a devastating loss for a family, it also presents a rewarding opportunity for an insurance restoration contractor, who should be prepared to do both structural repair work and specialized deodorization.

Paul Bianchina

Storm damage — from hail, wind, lightning, and other weather e…

Storm damage — from hail, wind, lightning, and other weather events — is the second largest category of insurance restoration work (after water damage). The side of this house was pocked and dented by hail.

Paul Bianchina

These salvageable materials from a water job have been dried and…

These salvageable materials from a water job have been dried and labeled and are awaiting transport back to the author’s warehouse for final cleaning and storage.

Paul Bianchina

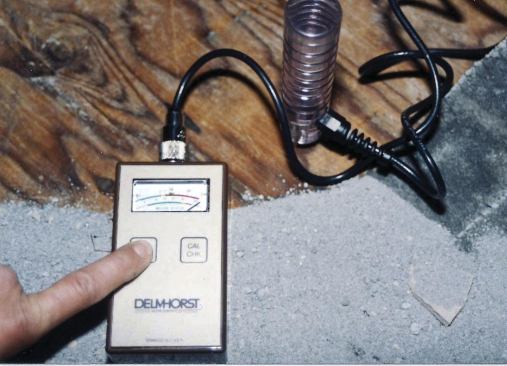

The equipment needed for structural drying — including air mov…

The equipment needed for structural drying — including air movers (top and bottom, left) and water testing meters (below) — typically represents a contractor’s biggest capital expenditure when entering the restoration field.

Paul Bianchina

Paul Bianchina

With all the destruction caused by Hurricane Sandy and other recent natural disasters, you may be considering a move into insurance restoration. As a retired general contractor who specialized in insurance restoration for over 20 years and co-owned one of the largest restoration companies in Oregon, I can tell you that this work is easily one of the most fascinating and potentially lucrative fields within the construction industry. Do it right and you’ll find an abundance of challenging, year-round work — plus you’ll be helping people and communities in ways you might not have thought possible.

But it can be a tough industry to break into. Restoration companies need good cash flow, as well as owners and employees who are willing to put in long hours and stormy nights away from home. Your clients experience a lot of stress, anger, and grief, which can be emotionally taxing. And if you don’t like paperwork, you might want to think twice before making the plunge.

Insurance Restoration vs. Remodeling

I was a remodeler long before I started doing insurance restoration work, and quickly learned that while there are some similarities between the two fields, there are a lot of differences too. When you’re remodeling, your clients have waited months for their new kitchen or addition. They’ve planned for it and can’t wait to get started. But with insurance restoration, it’s just the opposite. Your clients’ lives and homes have been thrown into sudden turmoil by unexpected damage, and even though you’re there to help, you’re also an intruder whom they’d just as soon have gone as quickly as possible.

Another big difference is that remodeling is a two-party relationship — just you and your client. In insurance restoration, there’s a somewhat ominous third party that can act as both your advocate and your nemesis: the insurance company.

Understanding the Insurance World

When a loss occurs, the property owner’s insurance agent initiates a claim. Then the insurance adjuster (also called a claims representative) enters the picture to represent the insurance company’s interests. The adjuster has three basic jobs: determine if the loss is covered under the terms of the policy; establish a dollar value for the loss; and coordinate all the paperwork while seeing the project through to completion.

For a loss to be covered, it must be “sudden and accidental.” For instance, if an ice-maker line breaks and ruins a kitchen floor, that’s a sudden and accidental occurrence. But if that line has been dripping for six months — regardless of whether the homeowner knew about it — the repairs most likely won’t be covered.

If the loss is covered, the adjuster, restoration contractor, and property owner meet and determine the “scope of loss” (in other words, what’s damaged and what needs to be repaired or replaced). This is a key element of insurance restoration: You can only bid what’s been damaged.

For example, say there is a room with a water-damaged wall, and the rest of the walls also sorely need painting. In a normal remodeling job, you would bid to paint the entire room. In restoration work, the adjuster will only pay to have the water-damaged wall painted, so that’s all you can bid. You can bid the other three walls later as a separate estimate. This means more paperwork, but adjusters don’t want any overlap.

Preparing the estimate. Typically, you’ll need to prepare your estimates in a format that’s approved by your client’s insurance company. This gives the company more control over costs and makes it easier for the adjuster to compare estimates.

Insurance companies don’t like per-hour or per-day rates, because they’re simply too vague. Instead, restoration estimating is done by unit costs — so much per square foot, per linear foot, and so on. Lots of books and software programs are available for unit-cost estimating, but the most widely accepted program in the insurance industry is Xactimate (see “Xactimate Estimating Software” sidebar).

After you’ve submitted the completed estimate to both the adjuster and the property owner, the adjuster reviews it to make sure it’s in line with the previously agreed scope and to verify that your pricing is in line with industry standards. Adjusters will also compare estimates against those of other contractors bidding the same loss, and possibly against estimates they’ve written themselves for comparison. Once the adjuster has an accurate value for the loss, work can begin.

Documentation. Each insurance company has different paperwork requirements, and the parameters are constantly changing. Be ready to document and track everything from the moment you walk onto the site. Our company prepared a separate binder for each job. We also took digital photos — lots of them — to document everything we did. For liability reasons, we also documented everything the homeowner had already done, plus any pre-existing damage or other unusual conditions. Once tear-out began, we used storage bins to keep small samples of building materials — trim, tile, flooring, paint samples, and the like — both to help with matching and to establish comparable values if revisions to the estimate were required. To maintain accurate records, we communicated by email with our clients and the insurance company whenever possible. When we spoke by phone or in person, we documented these communications with client file notes. Specific changes were executed on signed change-order forms.

Everything we accumulated on a job was labeled with the client’s name or job number, then stored for the duration of the job plus one year. After a year, it’s probably okay to discard bulky samples, though paperwork should go into long-term storage for at least seven years, or whatever your attorney recommends.

Who’s Your Client?

If the adjuster has approved your estimate and the insurance company is paying for the repairs, the insurance company must be your client, right? Wrong! Don’t ever forget that the property owner is still your client. The insurance company is the funding source, just like a bank is the funding source for a major remodeling project.

That means that you’ll still need to have a valid contract in place with the property owner, along with signed change orders for any additional work. You also need to comply with any state requirements for preliminary lien notices or other paperwork.

Protect yourself. Insurance companies issue payments directly to the property owner, and I’ve had clients spend that money on car repairs and vacations instead of using it to pay me. One client took the money, then filed for bankruptcy, leaving us at the end of a long line of creditors. Just because an insurance company is involved doesn’t mean that your money is guaranteed.

One way to protect yourself is to ask the insurance company to have your company placed on the draft, a common procedure particularly on larger losses. This prevents the homeowner from cashing the draft unless you sign off on it as well.

Deductible. This is a portion of the loss paid by the property owner, and may be a set dollar amount or a percentage of the building’s insured value. In either case, it falls to the contractor to collect the deductible, and you don’t want to wait until the end of the job to do it. Instead, collect it before work begins by writing it into your contract: “Deductible amount of $__ to be paid prior to commencement of work.” If you don’t want to use the word “deductible,” call it a “down payment.”

Some states and insurance companies impose restrictions on how deductibles and down payments can be collected, so you’ll need to rely on your attorney for the specific wording.

Restorative Drying

Emergency calls are common, and typically chaotic — such as the time we arrived at the house of a woman who had put some clothes in a sink, got distracted by her kids, and left for work with the sink stopped up and the faucet still running. In fact, the calls my company received most often were for structural drying after a building became wet. This process is known as “restorative drying” in the industry, because insurance companies increasingly expect to see building materials salvaged, not just torn out.

Proper drying requires the right equipment, plus specialized training such as the IICRC’s three-day Water Damage Restoration Technician course (see “Training and Certification,” page 58). The class covers the basics of how water affects a structure and what equipment and techniques are needed for drying various materials.

Equipment. A typical emergency water job begins with testing to find the extent of the water’s movement. Our testing equipment included a thermo-hygrometer to measure temperature and humidity levels ($100 to $500) and various types of moisture meters to determine how wet different materials are ($450 to $600).

We also owned a number of air movers ($150 to $550), which are used to evaporate the moisture and get it airborne. A small wet job will require three or four air movers, while larger jobs can require 10 or more for the initial drying. Large restoration companies will often own 25 to 30 air movers or more.

Dehumidifiers ($1,300 to $3,600) are used to remove the moisture from the building. A minimum of one dehumidifier is required per job, more on larger jobs. A contractor getting started in insurance restoration should expect an initial investment of at least $10,000 in equipment and training, in addition to any franchise fees.

Water and Storm Damage

Water damage — from frozen pipes, broken appliance lines, overflowing plumbing fixtures, wind-driven rain, and other sources — accounts for most insurance restoration work. Storm damage from hail, wind, lightning, and other related natural occurrences is a close second.

Water and storm losses vary tremendously in size. One of the single largest residential losses our company handled was a vacant home up for sale. A frozen third-floor pipe broke and ran for three days before a real-estate agent discovered it, causing almost $200,000 worth of damage.

Flooding. It’s important to realize that not all water damage is covered after a massive storm like Sandy or Katrina. “Ground water” — in a broad sense, water that came in contact with the ground before entering the house, including floods and tidal actions — is typically not covered unless the property owner has flood insurance. But if wind blew off the roofing and rain poured inside, both the shingle damage and the resulting water damage are typically covered.

Snow. Damage that results from the weight of snow and ice is typically covered, but damage caused by melted snow and ice (ground water) is not.

Mold. When water sits in contact with building materials, mold often grows — but mold is no longer a covered loss. So even though insurance will cover the cost of repairing water-damaged drywall, it won’t cover the added costs of dealing with the mold spores that may be released into the air while handling that wet drywall.

In this situation, a contractor would typically give the homeowners a separate estimate for mold remediation. Depending on the severity of the mold, the homeowners then have the option of paying the contractor separately to do the remediation, hiring out the remediation on their own, or doing the remediation themselves. Lots of gray areas here, and lots of legal liability. We’ve walked away from jobs where the homeowner wasn’t willing to have heavy mold infestations properly remediated, due to the liability.

Fire Damage

From an emotional standpoint, no other type of loss — no matter how extensive — had the same effect on our clients as a fire. A burnt home can be virtually unrecognizable — a black, twisted, foul-smelling heap.

Fire-related insurance work can be broken down into two categories: repairing structural damage, and deodorization. The science and technology behind fire repair has made significant strides in recent years. As a result, adjusters have become increasingly used to working with skilled restoration contractors, and they don’t want to pay to replace any items that can be cleaned and deodorized.

At a minimum, contractors working on fire restoration should receive the IICRC’s Fire & Smoke Restoration Technician certification (or the equivalent). This training is also helpful for understanding the deodorizing chemicals and equipment used in fire restoration.

Smoke deodorization can be very tricky. One of our most difficult “fire” jobs resulted from a neglected pot roast that slowly burned to a crisp on a stove. While there were no actual flames or sooty smoke, the home’s interior was coated with a sticky yellow film and permeated with the nauseating odor of burnt meat. We were able to remove the film and odor from all the home’s nooks and crannies, but it took a tremendous amount of effort.

Impact Damage

Insurance policies cover just about any type of damage caused by something hitting a building, from trees to drunk drivers. To me these are the most interesting and challenging types of losses, because they often involve structural issues that require the assistance of a structural engineer. For example, we once were involved in the repair of a house that had been partly knocked off its foundation after a runaway construction crane rolled into it.

Contents Cleaning and Storage

In virtually every job, there are wet or smoky contents that need to moved, cleaned, or stored. This is an aspect of restoration that a lot of contractors don’t give much thought to, but it can be very lucrative if you have the proper training, equipment, and warehouse space. You’ll also need proper insurance — including coverage for handling, transporting, and storing materials (usually treated as three separate activities by insurance companies) — and strong organizational skills. Since you’ll be dealing with your clients’ personal belongings, you’ll also need patience.

At first, our company handled just structural repairs and drying and subcontracted the contents handling to a specialized company. That allowed us to be a full-service contractor while avoiding some of the initial startup and liability costs of owning our own facility. Eventually, however, we built a dedicated warehouse and content processing facility, and brought everything in-house.

Paul Bianchina was a co-owner of Spectrum Building & Restoration in Bend, Ore., and is the author of Insurance Restoration Contracting: Startup to Success.