Over my decades in the construction industry, I’ve heard many discussions about profit. The relentless focus on the bottom line shunts aside another important issue, the need to manage cash as it flows through a company. That’s understandable. Maintaining profitability in a construction business is hard. But profit and cash are not the same thing.

Profit vs. Cash

The profit numbers reported by your accounting system can fool you. It may produce what financial professionals term “mismatches” between income and expense flows. That’s especially a hazard in construction where we learn to “bill early and bill often” in order to avoid having completed a lot of work that a customer is then unwilling or unable to pay for.

Billing early, though prudent, can cause a problem. We take the payments and record them in our accounting system. But expenses associated with the payments may not yet be incurred, much less recorded. That is, we’ve got a mismatch.

For example, we’ve largely framed the walls for a project. We’ve received and recorded payment for all wall framing. But we have not yet recorded all costs for the associated labor and material—say, for blocking or other pickup work yet to be done or workers’ comp premiums that will be coming due. As a result, profitability through the framing phase of a project looks better than it actually is. Cash is not so illusory. It’s either in a financial account or it’s not. You can think of profit as the bird in your sights. Cash is the bird in the freezer. —D.G.

Cash management is what the legendary grandmother does for her farming family. Prices at market for the farm’s apples are good. Much cash is coming home. Grandmother sets up a series of envelopes in her steel box with the hasp and lock. One is for the money to pay upcoming bills. Another is for charity, a third for holidays. A fourth is labeled “rainy day fund.” It’s for emergencies and hard times. A final envelope stores cash for purchase of a new tractor.

Grandmother takes each week’s income and divides it among the envelopes. She’s taken control of her farm’s cash. She’s managing it.

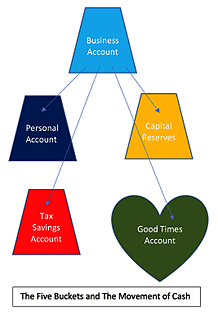

These days, when financial pros talk about business cash management, they use a “bucket” metaphor to describe a practice parallel to grandmother’s use of envelopes. As cash is generated by a business, it is divided into a series of “buckets,” just as grandmother divided her family’s cash into envelopes. These buckets are in actuality accounts at financial institutions.

When starting out in the construction business, we may have only one bucket, a checking account at a bank. We deposit income from our projects into that account and pay our business and personal expenses from it. That’s a practice that goes hand in hand with a financial mishap that often bedevils construction contractors. It encourages confusion of pay with profit. We see money piling up in our one account and take that as a sign that we are running a profitable business. But almost all of what we are perceiving as “profit” may, in fact, be the compensation that we will take for our work in the field and our office and use for personal expenses.

Our pay as a company owner is not profit. It is an expense to the company. Pay to anyone, including ourselves, who does work for the company is a company expense. Therefore, our pay must be deducted from company income to produce a valid number for profit.

To prevent the mistake of miscategorizing pay as profit, we take an initial step toward cash management. Keeping the first bucket as a personal account, we set up a second bucket for business income and expenses. Going forward, when we take pay for our work in our company, we transfer it from the business to the personal account and record the pay as a company expense.

With one bucket in place for our personal pay and expenses and another for business operations, we have made a good start at cash management. To match grandmother’s performance, we need more buckets. Next up, a bucket for tax payments. We’ll regularly transfer funds into it from our business bucket. Failure to set aside money for taxes can result in unpleasant consequences. Suddenly, it’s tax time. We don’t have money to pay our taxes in either our business or personal accounts. So we don’t pay them. Big fines can result—about $150,000 in the case of a flooring contractor I once worked with.

As our business matures, we need a fourth bucket. That’s the capital-reserves bucket. It’s the construction pro’s equivalent of grandmother’s hard-times envelope. Hard times do come in construction, hitting in the form of what I call “profit costs” like those described in the sidebar “Profit Costs and Capital Reserve,” (below).

With your capital reserves and other buckets topped up, you can establish a fifth bucket. It’s my favorite. Let’s call it the “good-times bucket.” It’s your storehouse of free cash—money not claimed by ongoing personal expenses or business needs. Some folks will spend it on a boat, travel, a grander home, or a vacation cabin. Others will opt to invest their free cash to secure financial freedom. That is my preference. Financial freedom is to me the best of all good times. Nothing beats being able to greet the day knowing you can go about your business from choice, not out of economic necessity.

Profit Costs and Capital Reserves

In construction, we have three kinds of costs: the direct costs of construction at our jobsites, the off-site costs of running our companies, and what I like to call “profit costs”—those strikes out of the blue that can take a big chunk out of our profits.

Profit costs range from abrupt inflation in material prices during a job to lawsuits long after a project has been completed. The appendix of my new book, Building Freedom, contains a list of 35 profit costs.

With skilled management and luck, we might escape most of them. But we won’t escape all. Prudence requires that we be ready for them—with a topped-up capital-reserves bucket.

Judith Miller, a veteran financial advisor in the remodeling industry, underscores the point: Many construction contractors, she says, “fall prey to the arrogance of profitability.” Business is booming. They are on a roll. They fritter away their cash on speculative ventures and big boys’ toys. “They do that without realizing they are failing to develop a sufficient war chest of money for protection during bad times.” Over the course of her career, Miller has watched many builders suffer due to lack of the capital reserves needed to cover profit costs. —D.G.

By now you may be wondering, “where should I keep my cash and how much cash should I keep in each bucket?” Answers vary depending on the legal form and needs of your business. But generally, you want your cash in accounts at reliable financial institutions.

The initial all-in-one bucket that will become your personal account can be set up at a full-service local bank. Bucket #2, the business account, could be at the same bank. But that may foster errors like using the business account for personal expenses. Placing the business account in a separate bank can safeguard against that error.

Bucket #3, the tax account, can be housed at the same bank as either the personal or the business account. Rather than a checking account, it can be a savings account. As you determine the amount you need to set aside for taxes, you transfer funds from the business to the savings account and keep them there until tax payments are due.

For capital reserves, you may, for convenience sake, set up an account at the bank you use for your business account. Alternatively, especially as your capital reserves grow, you might prefer a financial institution where you can more readily place part of the reserves in “investment vehicles” such as CDs (or even, to a prudent extent, stock or bond funds). Thereby, you could capture earning power beyond what’s likely to be available from an account at a bank.

Bucket #5, your good-times account, should almost certainly be at a financial institution that serves investors. From there, you can deploy your money into whatever pleasures or investments suit you. One caution: You do not want to indefinitely leave your good-times money stored in the form of cash. Ray Dalio, the legendary investor and philanthropist, warns us that in the long run, “cash is trash.” Well, maybe not quite. But the purchasing power of cash does get eaten away by inflation. The dollars that today buy you a hamburger will eventually get you just the bun and the pickles.

That brings us to a last question: How much cash should you place in each of your five buckets? Answering it requires judgment calls.

The business account must retain enough to cover all ongoing costs for construction and for overhead. To calculate the amount, you must accurately project the income and outflow that your business will experience over coming months. Given the frequency and severity of profit costs that hit construction companies, you’d be wise to keep your projections on the safe side. Under-project income. Over-project expenses. Maintain a margin of safety.

You need to transfer enough money to the personal bucket to cover your ongoing costs of living. If you require a high-end lifestyle, the personal bucket will need to be fed a great deal of cash. If your priority is financial freedom, you will want to restrain the amount of cash going into the personal bucket and deploy more for investments.

The tax bucket needs to be fed enough cash to cover upcoming federal and state estimated tax payments. Determine what percentage of your profits you will be required to pay in taxes. As you complete a job—or on large projects, a phase of a job—calculate profitability. Set aside the determined percentage of the profits for taxes.

As for capital reserves, construction business advisors advocate varying amounts. Victoria Downing, president of Remodelers Advantage, urges having enough cash in reserve to cover half a year’s worth of overhead expenses, including owner’s pay.

I have long urged an even more conservative guideline, namely 10% of annual revenue as capital reserves. That’s $100,000 at $1 million revenue and $1 million at $10 million revenue. A builder I have interviewed for my books owns a company that was enjoying some $10 million annually in revenue when a brutal recession hit. Over the next couple of years, he burned through about $700,000 of his reserves to keep his company going. He was glad he had gone with 10%. His business survived and prospered again, refilling the buckets for capital reserves and pouring free cash into his good-times bucket.

For your good-times bucket, my answer to the “how much” question is, “as much as possible without compromising the strength of your company and the work it produces.” In a coming article, I will discuss the features of a strong and sustainable construction company.

With five buckets, each being fed an appropriate amount of cash, you have effectively assumed management of your cash. You want to do that. You do not want to stop at just recording and accounting for the money that flows through your business.

Accounting is about observation. Cash management is about command and control. You want to direct the flow of your cash. You worked steadily to acquire it, so be sure you take charge of it.