A few years ago, I wrote a column in which I tried to clear up some of the confusion surrounding the terms “mark up” and “margin” (Business Forum, 2/95). In that article, I explained that many contractors who use a multiplier to “mark up” their estimated costs actually underprice their jobs by 5% or more. I suggested throwing out the term “mark up” in favor of “gross profit margin,” and I provided a method for arriving at the proper selling price that uses a divisor.

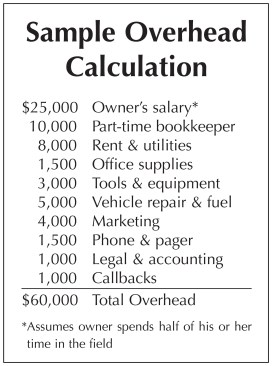

Figure 1. To find your overhead, add together all of the costs your company would incur for the year whether or not you took on any work. If you’re not sure of some amounts for the current year, make your best guess based on expenses for past years.

Since then, however, I’ve talked with many builders and remodelers who are still confused, not only about how to calculate gross profit but also about how the resulting percentage relates to estimated costs and selling price. So in this article, I’m going to make another run at it, this time using simple fractions — and, yes, some visual aids — to explain the critical relationships between estimated costs, gross profit, and selling price.

Calculating Gross Profit

Nobody who wants to stay in business for long can price a job at cost. In addition to the cost of materials, labor, and subcontractors for each project — called direct costs — a construction company has non-job-related expenses — called indirect costs or overhead — that must be included in the price of every job (see Figure 1). The selling price should also include profit, which every business needs both to compensate for risks and to provide capital for growth. Together, overhead and profit comprise gross profit, which is typically expressed as a percentage of total revenue.

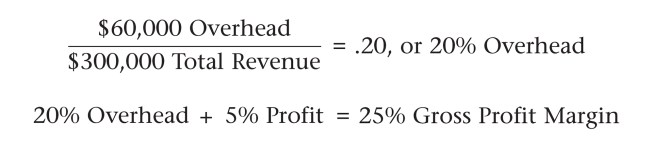

The simplest way to find the overhead percentage is to first calculate the total dollar amount of overhead, then divide by the total revenue. (If you can’t accurately estimate total revenue for the current year, make your best guess or use last year’s dollar volume.) To find gross profit, add a profit percentage to the overhead percentage. Using the overhead dollar amount from Figure 1 and a target profit of, say, 5%, the math looks like this if annual revenue is $300,000:

Finding the Selling Price

Once you know what your gross profit margin is, you can use it to increase direct costs and arrive at the selling price. Unfortunately, however, it’s easy to use the right gross profit margin to come up with the wrong selling price. It seems obvious, for instance, that adding 25% to your direct costs would give you a selling price that would cover the 25%gross profit in the above example. But the fact is, simply adding 25% results in a selling price that’s too low. To cover a 25% gross profit, you have to increase estimated costs by 33%.

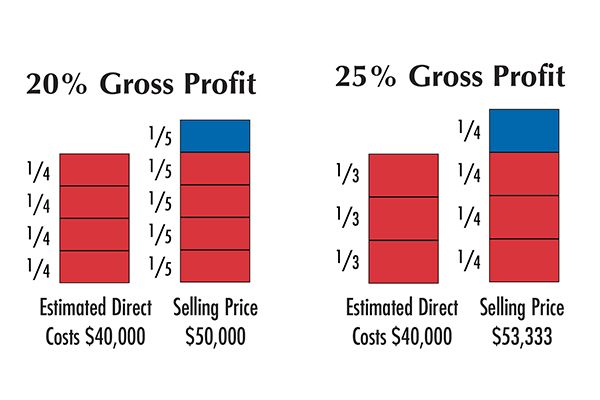

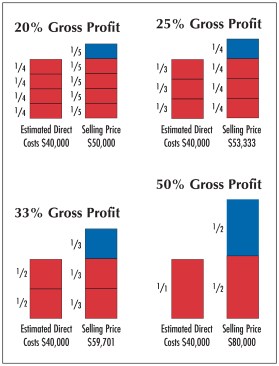

To understand why this is true, look at the four pairs of columns in Figure 2. In each pair, the left-hand column represents estimated direct costs (materials, labor, and subs) of $40,000, so every left-hand column is the same height. The right-hand column in each pair, however, changes depending on what gross profit percentage is being used to figure the selling price.

Figure 2. The left-hand column in each pair of columns is the same, and represents estimated direct costs of $40,000. The right-hand columns, which represent the selling price, vary depending on what gross profit percentage (blue boxes) is used. Taken together, each pair of columns shows how the fraction of estimated costs that must be added to arrive at the correct selling price is always higher than the fraction of the selling price that represents gross profit.

To follow through on our example, look at the pair of columns labeled “25% Gross Profit.” The blue box represents 25%, or 1/4, of the total revenue for the job. But this is 33%, or 1/3, of the estimated direct costs. In other words, when you’re done estimating direct costs, you have to add 1/3 of those costs to arrive at a selling price that will cover a gross profit of 1/4.

With a smaller gross profit of 20% or 1/5, you need to add 1/4 of estimated costs. For a larger gross profit — 33% or 1/3, for example — you need to add 1/2 of estimated costs. Finally, to earn a gross profit of 50% or 1/2, you have to sell the job at exactly twice your cost.

The Magic Formula

These examples use nice round numbers that I hope will help you visualize the relationship between estimated costs, gross profit, and selling price. When it comes to actually crunching the numbers, however, there’s a foolproof formula for calculating a selling price that covers both overhead and profit: Simply take the decimal value of your gross profit, subtract it from 1, and divide it into your estimated costs. Returning to our example of $40,000 in estimated direct costs, the calculation would look like this:

Gross Profit = 25%, or .25

1 – .25 = .75

$40,000 ÷ .75 = $53,333 Selling Price

The formula works, not just for the gross profit percentages shown in Figure 2, but for any gross profit percentage. For example, if your gross profit is an odd number like 17.3%, the formula would work like this:

Gross Profit = 17.3%, or .173

1 – .173 = .827

$40,000 ÷ .827 = $48,368 Selling Price

Next time you have to quote a price, don’t simply add 15% to your estimate like everybody else. Instead, figure out what your gross profit percentage should be, then use a divisor to figure the selling price. You may not win every bid, but for those jobs you do get, you’ll cover your costs and earn a profit as well.