Target Your Profit

While you can attempt to predict your sales, the actual incoming and outgoing dollars associated with production are going to be, at best, a rough estimate.

But profit is a number you should know. In fact, you need to establish it—to build in profit as a target to shoot for, treating it, in essence, as a cost. It may seem counterintuitive to consider profit to be a cost, but unless it’s planned for, far too many contractors end up discovering profit as a happy accident, possibly only found at the end of the year when their accountant tells them how they did.

If you start with the mindset that net profit is as justifiable a cost as, say, your office rent, then you can begin to plan on how to make sure that you sell your work with enough added dollars to be able to pay for that profit “cost.”

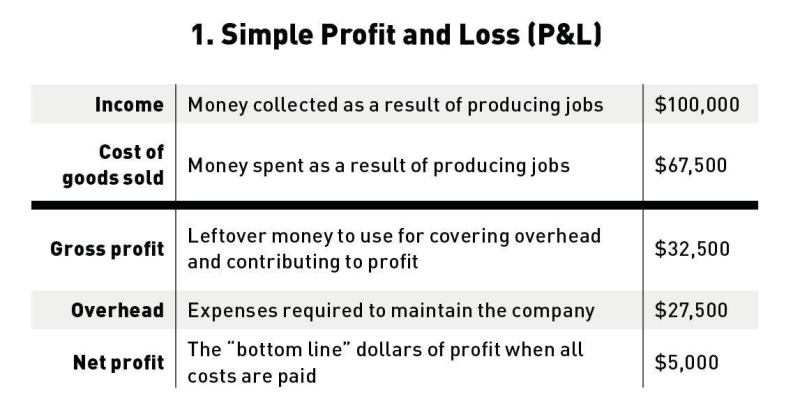

The chart above shows a simplified profit and loss statement (P&L), which includes income, production costs (COGS), overhead, and profit. In this model, the net profit ends up being a leftover. But what happens if we run it backward instead?

Step 1: Start with the most reliable, predictable number you can access: your overhead. Look at what you spent on overhead last year, or over the past 12 months. Write it down. Then put down what you think you will spend on a similar period, going forward. Consider whether you’re planning on hiring new office staff, increasing your marketing budget, paying more in rent, and so on.

Step 2: Write down the profit you earned last year. Are you happy with it? Do you want more? Put down the dollars of profit you want this year. Don’t be shy!

Step 3: Add the numbers together. This is the number of dollars you’ll need to have as your gross profit.

Gross Profit = Production Income – Production Costs

The significance of gross margin

While gross profit is an essential line item to account for, gross margin actually serves as a better tool for determining how profitable a given job may be. To see how this works, let’s review where we’re at.

In Part 1 we looked at a simplified profit and loss statement so we could better understand the terms involved. Here in Part 2, we began by running the profit and loss “backward,” starting with the overhead we were confident we would need to cover, and then adding the target profit amount we’d like to achieve. The total of these two amounts ($40,000 in our example) represents the dollars you’ll need to have left over after you finish producing your work.

It’s simple math: If you need to spend $40,000 on covering overhead and meeting your target profit, then the “leftover” dollars from producing work must be $40,000.

Now the questions you need to ask become: What do you need to mark up your costs by? And how much work must you sell in order to make your overhead and profit?

The answer is not as obvious as it might first seem because you can get to that magic $40,000 in many ways. A bigger job does not necessarily mean a bigger profit.

The underlying question is: Would you prefer to sell $1,000,000 or only half of that or one-quarter, or even one-tenth, of that in order to earn the same $40,000?

Gross Margin is a Better Comparison

In order to understand what’s practical for your company, you need to have more information about key numbers associated with your completed jobs. Namely, you need to know: What was your average achieved gross margin over the past 12 months?

Gross margin is related to gross profit but is expressed as a percentage rather than in dollars. You get gross margin by dividing the gross profit in dollars by income in dollars.

Gross margin is really the percentage of your income that’s due to gross profit. The higher the gross margin, the more profitable the job.

Using percentages makes it easier to compare dissimilar jobs. For example, the chart at bottom above shows two jobs of different sizes. Which one was more profitable? Is it easier to answer that question based on dollars of profit or on gross margin?

What’s next?

Once you know what gross margin your company can realistically achieve (assuming no major changes in your production process), you can estimate the sales volume and markup required in order to meet your objectives. We’ll look at those two— markup and margin—in next month’s installment.

Melanie Hodgdon is owner of Business Systems Management.

melaniehodgdon.com